How Much SIP You Need to Reach 1 crore?

This article helps you calculate how much you will need to invest every month to reach the first significant portfolio milestone of ₹ 1 crore by investing in mutual funds.

This article helps you calculate how much you will need to invest every month to reach the first significant portfolio milestone of ₹ 1 crore by investing in mutual funds.

₹1 crore is the first wealth milestone, after the previous ones of ₹1 lakh and ₹10 lakhs, where the power of compounding starts to be felt.

For example, if you have ₹1 crore today, just a ₹27,237/month SIP will get you to ₹2 crore in 5 years at 12%. Out of that ₹2 crores, around ₹26.40 lakhs would have come from the SIP, while the remaining ₹1.74 crore would have come from the starting ₹1 crore.

In this article, we will cover how to reach your first ₹1 crore by investing in Mutual Funds by SIP.

To understand how to find the SIP amount, we will take the example of driving from Kashmir to Kanyakumari. Using Google Maps data,

| Metric | Car Travel | Investment Goal |

|---|---|---|

| Target | 3,600 Km | ₹ 1 crore |

| Time | 8 days with 9hr/day driving |

8 years with 12% return/year |

| Effort | 50 Km/hr average speed |

₹63,674/month |

For the investment, we need:

In the cases below, we will assume 12% return from investment and 10% annual step-up in the SIP amount.

| Years | Monthly SIP Amount |

Total investment (lakhs) |

|---|---|---|

| 5 | ₹1,03,000 | ₹75.59 |

| 6 | ₹77,438 | ₹71.70 |

| 7 | ₹59,836 | ₹68.12 |

| 8 | ₹47,143 | ₹64.70 |

| 9 | ₹37,723 | ₹61.47 |

| 10 | ₹30,594 | ₹58.51 |

| 11 | ₹25,015 | ₹55.63 |

| 12 | ₹20,642 | ₹52.97 |

| 13 | ₹17,176 | ₹50.54 |

| 14 | ₹14,351 | ₹48.17 |

| 15 | ₹12,105 | ₹46.15 |

If you are investing to reach ₹1 crore via safe investments like Recurring Deposits (RD), then you need ₹60,940/month (vs. ₹30,594/month via SIP) to reach ₹1 crore in 10 years assuming 5%/year post-tax returns in RD.

To see how this works with your portfolio, you can use the Arthgyaan SIP Calculator for Target Amount

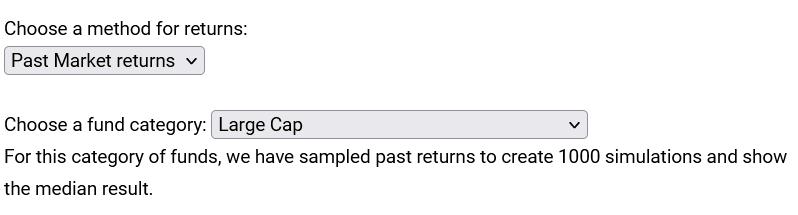

Our How Much SIP You Need to Reach 1 crore? calculator allows you to know how much you should invest via SIP to reach a specific target corpus amount say ₹1 crore. For example:

Required Monthly SIP (₹):

Total Investment (₹):

Target Value (₹):

Inflation-Adjusted Value (₹):

If you found this useful, check out the Arthgyaan step-up SIP calculator.You need to enter just these numbers to get started with the Arthgyaan SIP Calculator for Target Amount calculator:

These inputs are optional and can be left as-is

The output of the Arthgyaan SIP Calculator for Target Amount has two easy to understand parts:

These are the numbers that have the result of the Arthgyaan SIP Calculator for Target Amount:

To understand more about Uncertainty-Adjusted Range, please refer to our detailed article that will help you adjust your expectations from investing in the stock market:

The Arthgyaan SIP Calculator for Target Amount allows you to choose which type of mutual funds:

Here is the compiled result for a 10 year, 10% step-up SIP:

| Mutual Fund Category |

Monthly SIP Amount |

Total investment (lakhs) |

Risk |

|---|---|---|---|

| Small Cap | ₹37,575 | ₹51.56 | Very High |

| Mid Cap | ₹38,624 | ₹53.00 | Very High |

| Large Mid Cap | ₹42,311 | ₹58.06 | Very High |

| Large Cap | ₹42,884 | ₹58.84 | Very High |

| Aggressive Hybrid | ₹43,392 | ₹59.54 | High |

| Multi Asset Allocation | ₹44,918 | ₹61.64 | High |

| Gold | ₹49,750 | ₹68.27 | High |

| Conservative Hybrid | ₹51,785 | ₹71.06 | Medium |

| Equity Savings | ₹51,912 | ₹71.23 | Medium |

| Gilt With 10 Year Constant Duration | ₹54,200 | ₹74.37 | Medium |

| Gilt | ₹55,154 | ₹75.68 | Medium |

| Money Market | ₹56,012 | ₹76.86 | Low |

| Liquid | ₹56,362 | ₹77.34 | Low |

| Arbitrage | ₹56,426 | ₹77.43 | Very Low |

| Overnight | ₹57,634 | ₹79.08 | Very Low |

Investors should balance the risk of various fund categories vs. the amount they need to invest. Here risk comes from the fact that mutual fund returns fluctuate due to market movements and are not guaranteed. In general, for the same amount of time allocated to reach the target of ₹1 crore:

Here is the latest data regarding mutual fund returns that will give you an estimate of what to expect based on past returns.

| Category | Any 1Y SIP | Any 2Y SIP | Any 3Y SIP | Any 5Y SIP | Any 7Y SIP | Any 10Y SIP |

|---|---|---|---|---|---|---|

| Equity: Large Mid Cap | 14.81% | 11.6% | 17.7% | 17.47% | 18.34% | 16.65% |

| Equity: Sectoral or Thematic | 13.04% | 11.97% | 17.18% | 16.43% | 17.4% | 16.13% |

| Equity: Flexi Cap | 13.48% | 11.1% | 15.48% | 15.89% | 16.49% | 15.83% |

| Equity: ELSS | 14.07% | 10.68% | 16.2% | 16.16% | 17.04% | 16.06% |

| Equity: Large Cap | 14.06% | 11.33% | 14.41% | 14.11% | 14.7% | 14.21% |

| Equity: Value | 14.04% | 12.16% | 17.66% | 16.48% | 17.03% | 15.93% |

| Equity: Mid Cap | 17.26% | 13.2% | 20.0% | 19.87% | 21.86% | 19.11% |

| Equity: Multi Cap | 14.4% | 12.36% | 17.82% | 17.98% | 18.35% | 16.38% |

| Equity: Contra | 16.81% | 12.53% | 18.3% | 18.62% | 20.73% | 18.98% |

| Equity: Dividend Yield | 13.11% | 10.25% | 15.29% | 16.36% | 17.69% | 16.03% |

| Equity: Focused | 14.18% | 11.24% | 15.87% | 15.34% | 15.88% | 15.28% |

| Equity: Index | 11.97% | 9.41% | 15.71% | 14.85% | 15.01% | 13.86% |

| Category | Any 1Y SIP | Any 2Y 目↑ SIP | Any 3Y 目↑ SIP | Any 5Y 目↑ SIP | Any 7Y 目↑ SIP | Any 10Y 目↑ SIP |

|---|---|---|---|---|---|---|

| Equity: Large Mid Cap | 14.81% | 10.81% | 16.73% | 17.56% | 19.23% | 17.44% |

| Equity: Sectoral or Thematic | 13.04% | 11.06% | 16.39% | 17.33% | 19.11% | 17.18% |

| Equity: Flexi Cap | 13.48% | 9.99% | 14.92% | 15.74% | 17.33% | 16.41% |

| Equity: ELSS | 14.07% | 10.54% | 15.73% | 16.12% | 17.87% | 16.59% |

| Equity: Large Cap | 14.06% | 10.31% | 14.51% | 14.71% | 16.02% | 15.13% |

| Equity: Value | 14.04% | 9.69% | 16.41% | 17.66% | 19.35% | 17.11% |

| Equity: Mid Cap | 17.26% | 12.01% | 18.67% | 19.74% | 22.28% | 19.59% |

| Equity: Multi Cap | 14.4% | 10.7% | 16.15% | 17.23% | 20.14% | 18.12% |

| Equity: Contra | 16.81% | 11.05% | 17.84% | 19.64% | 21.73% | 19.68% |

| Equity: Dividend Yield | 13.11% | 9.48% | 15.74% | 18.63% | 20.52% | 18.06% |

| Equity: Focused | 14.18% | 10.29% | 15.29% | 15.94% | 17.61% | 16.28% |

| Equity: Index | 11.97% | 9.43% | 14.92% | 14.4% | 14.98% | 14.19% |

| Category | Any 1Y | Any 2Y | Any 3Y | Any 5Y | Any 7Y | Any 10Y |

|---|---|---|---|---|---|---|

| Equity: Large Mid Cap | 10.87% | 17.2% | 18.83% | 18.36% | 17.43% | 15.87% |

| Equity: Sectoral or Thematic | 9.6% | 17.53% | 17.98% | 16.77% | 16.29% | 15.2% |

| Equity: Flexi Cap | 11.18% | 15.72% | 16.3% | 15.67% | 15.8% | 15.2% |

| Equity: ELSS | 11.55% | 15.9% | 16.75% | 16.66% | 16.23% | 15.53% |

| Equity: Large Cap | 10.63% | 14.99% | 14.42% | 14.32% | 14.02% | 14.18% |

| Equity: Value | 10.52% | 16.46% | 17.93% | 16.1% | 15.52% | 15.29% |

| Equity: Mid Cap | 14.62% | 19.94% | 21.91% | 20.71% | 20.12% | 17.84% |

| Equity: Multi Cap | 11.34% | 18.41% | 18.8% | 18.01% | 16.73% | 16.21% |

| Equity: Contra | 14.31% | 17.93% | 18.75% | 19.94% | 19.48% | 18.2% |

| Equity: Dividend Yield | 10.29% | 16.66% | 17.3% | 18.39% | 15.79% | 15.11% |

| Equity: Focused | 11.12% | 15.49% | 17.15% | 16.74% | 15.28% | 15.34% |

| Equity: Index | 6.76% | 16.19% | 16.88% | 15.76% | 13.93% | 13.51% |

| Category | Any 1Y SIP | Any 2Y SIP | Any 3Y SIP | Any 5Y SIP | Any 7Y SIP | Any 10Y SIP |

|---|---|---|---|---|---|---|

| Debt: Medium To Long Duration | 6.93% | 6.58% | 7.47% | 6.96% | 6.77% | 6.92% |

| Debt: Liquid | 6.53% | 6.51% | 6.48% | 6.09% | 5.88% | 5.97% |

| Debt: Gilt | 7.39% | 6.6% | 7.64% | 7.3% | 7.03% | 7.18% |

| Debt: Medium Duration | 8.16% | 7.99% | 7.86% | 6.69% | 6.45% | 7.27% |

| Debt: Money Market | 7.22% | 7.24% | 7.19% | 6.94% | 6.55% | 6.55% |

| Debt: Long Duration | 7.1% | 7.61% | 7.6% | 7.68% | 7.56% | 7.41% |

| Debt: Dynamic Bond | 7.23% | 7.16% | 7.62% | 7.24% | 6.95% | 7.23% |

| Debt: Low Duration | 7.68% | 7.96% | 7.75% | 7.12% | 6.94% | 6.81% |

| Debt: Corporate Bond | 7.57% | 7.84% | 7.55% | 7.24% | 7.32% | 7.36% |

| Debt: Ultra Short Duration | 6.79% | 6.6% | 6.71% | 6.64% | 6.46% | 6.28% |

| Debt: Banking And PSU | 7.57% | 7.78% | 7.77% | 7.12% | 7.13% | 7.16% |

| Debt: Overnight | 5.36% | 5.76% | 5.93% | 5.91% | 5.45% | 5.39% |

| Debt: Gilt Fund With 10 Year Constant Duration | 8.54% | 8.29% | 8.22% | 8.8% | 7.9% | 7.59% |

| Debt: Floater | 7.02% | 7.64% | 7.93% | 7.39% | 7.35% | 7.39% |

| Debt: Short Duration | 7.81% | 7.86% | 7.72% | 7.29% | 6.91% | 7.19% |

| Debt: Credit Risk | 8.65% | 9.52% | 8.85% | 8.04% | 7.76% | 7.53% |

| Debt: Index | 8.19% | 8.4% | 7.9% | 0% | 0% | 0% |

| Category | Any 1Y SIP | Any 2Y 目↑ SIP | Any 3Y 目↑ SIP | Any 5Y 目↑ SIP | Any 7Y 目↑ SIP | Any 10Y 目↑ SIP |

|---|---|---|---|---|---|---|

| Debt: Medium To Long Duration | 6.93% | 6.28% | 6.92% | 6.94% | 6.93% | 6.94% |

| Debt: Liquid | 6.53% | 6.57% | 6.69% | 6.48% | 6.08% | 6.03% |

| Debt: Gilt | 7.39% | 5.65% | 6.38% | 6.5% | 6.53% | 6.89% |

| Debt: Medium Duration | 8.16% | 8.61% | 8.37% | 7.75% | 7.42% | 7.43% |

| Debt: Money Market | 7.22% | 7.38% | 7.48% | 7.02% | 6.66% | 6.63% |

| Debt: Long Duration | 7.1% | 7.13% | 6.98% | 6.75% | 6.68% | 6.9% |

| Debt: Dynamic Bond | 7.23% | 6.92% | 7.3% | 7.08% | 7.0% | 7.17% |

| Debt: Low Duration | 7.68% | 8.12% | 8.0% | 7.35% | 7.06% | 6.87% |

| Debt: Corporate Bond | 7.57% | 8.27% | 8.19% | 7.41% | 7.24% | 7.39% |

| Debt: Ultra Short Duration | 6.79% | 7.33% | 7.35% | 6.94% | 6.68% | 6.43% |

| Debt: Banking And PSU | 7.57% | 7.97% | 7.9% | 7.27% | 7.12% | 7.2% |

| Debt: Overnight | 5.36% | 6.01% | 6.17% | 5.96% | 5.51% | 5.42% |

| Debt: Gilt Fund With 10 Year Constant Duration | 8.54% | 7.67% | 8.02% | 7.21% | 7.0% | 7.39% |

| Debt: Floater | 7.02% | 8.23% | 8.26% | 7.61% | 7.39% | 7.47% |

| Debt: Short Duration | 7.81% | 8.14% | 8.02% | 7.49% | 7.29% | 7.31% |

| Debt: Credit Risk | 8.65% | 10.44% | 10.16% | 9.05% | 8.49% | 8.04% |

| Debt: Index | 8.19% | 8.41% | 7.88% | 0% | 0% | 0% |

| Category | Any 1Y | Any 2Y | Any 3Y | Any 5Y | Any 7Y | Any 10Y |

|---|---|---|---|---|---|---|

| Debt: Medium To Long Duration | 7.49% | 7.79% | 7.39% | 6.53% | 7.15% | 7.19% |

| Debt: Liquid | 6.66% | 6.7% | 6.42% | 5.77% | 5.8% | 6.29% |

| Debt: Gilt | 7.57% | 7.84% | 7.88% | 7.51% | 7.85% | 7.86% |

| Debt: Medium Duration | 8.04% | 8.16% | 7.83% | 6.7% | 6.98% | 7.52% |

| Debt: Money Market | 7.35% | 7.4% | 7.18% | 6.46% | 6.71% | 6.9% |

| Debt: Long Duration | 7.79% | 8.83% | 8.23% | 7.43% | 8.44% | 7.96% |

| Debt: Dynamic Bond | 7.39% | 8.09% | 7.85% | 7.05% | 7.45% | 7.69% |

| Debt: Low Duration | 7.78% | 8.1% | 7.6% | 6.81% | 6.88% | 7.1% |

| Debt: Corporate Bond | 7.88% | 8.17% | 7.7% | 7.27% | 7.69% | 7.81% |

| Debt: Ultra Short Duration | 6.88% | 6.64% | 6.66% | 6.31% | 6.51% | 6.67% |

| Debt: Banking And PSU | 7.76% | 7.98% | 7.73% | 6.94% | 7.58% | 7.54% |

| Debt: Overnight | 5.48% | 5.87% | 5.73% | 5.26% | 5.17% | 5.61% |

| Debt: Gilt Fund With 10 Year Constant Duration | 8.72% | 8.99% | 9.01% | 8.99% | 8.65% | 8.38% |

| Debt: Floater | 7.09% | 7.59% | 7.8% | 6.9% | 7.46% | 7.58% |

| Debt: Short Duration | 7.93% | 7.92% | 7.76% | 7.11% | 7.34% | 7.57% |

| Debt: Credit Risk | 8.71% | 9.4% | 8.71% | 8.0% | 7.22% | 7.63% |

| Debt: Index | 8.24% | 8.57% | 7.84% | 0% | 0% | 0% |

| Category | Any 1Y SIP | Any 2Y SIP | Any 3Y SIP | Any 5Y SIP | Any 7Y SIP | Any 10Y SIP |

|---|---|---|---|---|---|---|

| Hybrid: Aggressive | 12.3% | 10.52% | 14.47% | 14.51% | 15.08% | 14.16% |

| Hybrid: Conservative | 8.78% | 8.23% | 9.21% | 8.7% | 8.95% | 8.63% |

| Hybrid: Equity Savings | 9.87% | 9.03% | 10.18% | 9.9% | 9.97% | 9.47% |

| Hybrid: Arbitrage | 6.47% | 6.72% | 6.55% | 6.32% | 6.19% | 6.29% |

| Hybrid: Balanced | 8.81% | 11.05% | 0% | 0% | 0% | 0% |

| Category | Any 1Y SIP | Any 2Y 目↑ SIP | Any 3Y 目↑ SIP | Any 5Y 目↑ SIP | Any 7Y 目↑ SIP | Any 10Y 目↑ SIP |

|---|---|---|---|---|---|---|

| Hybrid: Aggressive | 12.3% | 10.08% | 13.88% | 14.42% | 15.59% | 14.66% |

| Hybrid: Conservative | 8.78% | 7.85% | 9.15% | 8.98% | 9.21% | 8.82% |

| Hybrid: Equity Savings | 9.87% | 8.87% | 10.33% | 9.97% | 10.18% | 9.57% |

| Hybrid: Arbitrage | 6.47% | 7.07% | 7.32% | 6.97% | 6.59% | 6.48% |

| Hybrid: Balanced | 8.81% | 11.06% | 0% | 0% | 0% | 0% |

| Category | Any 1Y | Any 2Y | Any 3Y | Any 5Y | Any 7Y | Any 10Y |

|---|---|---|---|---|---|---|

| Hybrid: Aggressive | 10.18% | 14.3% | 14.53% | 14.46% | 14.08% | 13.74% |

| Hybrid: Conservative | 8.22% | 9.74% | 9.47% | 8.71% | 8.75% | 8.64% |

| Hybrid: Equity Savings | 8.77% | 10.54% | 10.33% | 9.95% | 9.53% | 9.16% |

| Hybrid: Arbitrage | 6.53% | 7.01% | 6.43% | 6.01% | 6.08% | 6.41% |

| Hybrid: Balanced | 10.01% | 15.11% | 0% | 0% | 0% | 0% |

Your choice of funds will therefore depend on the return expectations. We have included the lump sum returns as well since it will impact the lump sum investment amount that you already have at the beginning of the investment.

In this table, we show how much the SIP amount changes based on the return expectations of the chosen fund for a 10% step-up SIP for reaching ₹1 crore in 10 years

| Return | Monthly SIP Amount |

Total investment (lakhs) |

Return (lakhs) |

|---|---|---|---|

| 5% | ₹42,038 | ₹80.40 | ₹ 19.60 |

| 6% | ₹40,207 | ₹76.90 | ₹ 23.10 |

| 7% | ₹38,478 | ₹73.59 | ₹ 26.41 |

| 8% | ₹36,748 | ₹70.28 | ₹ 29.72 |

| 9% | ₹35,121 | ₹67.17 | ₹ 32.83 |

| 10% | ₹33,544 | ₹64.15 | ₹ 35.85 |

| 11% | ₹32,018 | ₹61.23 | ₹ 38.77 |

| 12% | ₹30,594 | ₹58.51 | ₹ 41.49 |

| 13% | ₹29,221 | ₹55.88 | ₹ 44.12 |

| 14% | ₹27,847 | ₹53.26 | ₹ 46.74 |

| 15% | ₹26,576 | ₹50.83 | ₹ 49.17 |

It is very important to note how much less investment is required if the return expectation increases. Of course, the higher return you expect, the higher is the expected fluctuations due to market movements.

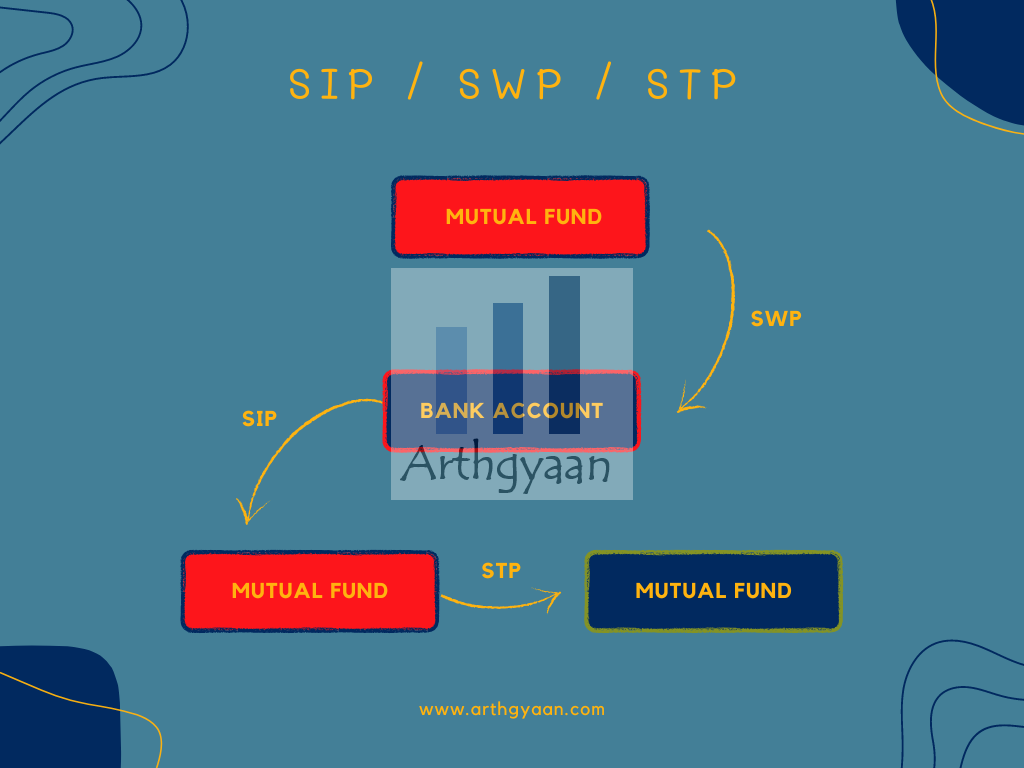

All of these are standing instructions that get executed as per a schedule you specify:

A SIP is an instruction to a mutual fund to deduct from your bank account, typically every month, to invest in a mutual fund. The amount invested stays the same every month.

A step-up SIP is one where the monthly amount invested increases, say by 5% or 10%, after a year every year until you stop the SIP.

You can see how the monthly amounts in a SIP and step-up SIP change like this:

| Year | SIP | 10% Step-up SIP |

|---|---|---|

| 1 | 1,000 | 1,000 |

| 2 | 1,000 | 1,100 |

| 3 | 1,000 | 1,210 |

| 4 | 1,000 | 1,331 |

| 5 | 1,000 | 1,464 |

We have covered the basics of a step-up SIP in detail in the link below:

| Return | Fixed SIP Amount |

Step-Up SIP Amount |

Lower investment in step-up SIP |

|---|---|---|---|

| 5% | ₹64,519 | ₹42,038 | -34.84% |

| 6% | ₹61,264 | ₹40,207 | -34.37% |

| 7% | ₹58,111 | ₹38,478 | -33.79% |

| 8% | ₹55,161 | ₹36,748 | -33.38% |

| 9% | ₹52,312 | ₹35,121 | -32.86% |

| 10% | ₹49,616 | ₹33,544 | -32.39% |

| 11% | ₹47,073 | ₹32,018 | -31.98% |

| 12% | ₹44,632 | ₹30,594 | -31.45% |

| 13% | ₹42,292 | ₹29,221 | -30.91% |

| 14% | ₹40,105 | ₹27,847 | -30.56% |

| 15% | ₹38,020 | ₹26,576 | -30.10% |

The table above shows the effects of a step-up vs. fixed SIP for reaching ₹1 crore in 10 years at 12% average returns. Since a step-up SIP moves the bulk of the investment amount into the future, when income is expected to be higher, the starting SIP amount is much lower vs. a fixed SIP.

The short answer is that both are important. If you have a chunk of money already invested, that is the lump sum that enters the calculation. If you have not yet invested that lump sum into mutual funds, you can do so either at one go, or if it makes you feel better, split that into 6-12 equal parts and invest into the chosen funds.

| Fund | Any 5Y | Any 7Y | Any 10Y |

|---|---|---|---|

| Quant ELSS Tax Saver Fund | 26.34% | 24.66% | 21.61% |

| Nippon India Small Cap Fund | 24.67% | 24.03% | 21.1% |

| Aditya Birla Sun Life Digital India Fund | 20.75% | 20.07% | 20.98% |

| SBI Midcap Fund | 14.26% | 15.98% | 20.72% |

| Invesco India Midcap Fund | 26.31% | 23.48% | 20.27% |

| Franklin Build India Fund | 14.54% | 16.29% | 20.23% |

| Quant Infrastructure Fund | 30.22% | 26.22% | 20.14% |

| Quant Small Cap Fund | 31.82% | 27.01% | 20.07% |

| Quant Flexi Cap Fund | 24.5% | 23.04% | 20.01% |

| Axis Midcap Fund | 18.51% | 18.09% | 19.8% |

The above table shows the top funds with the highest lump sum returns right now.

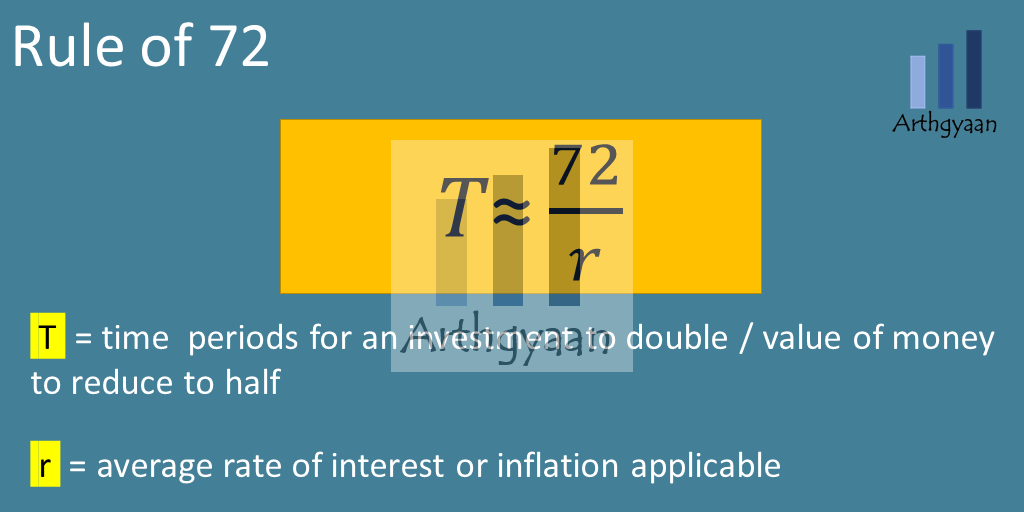

Inflation is essential to goal planning in an economy where prices are rising overall. We can use the rule of 72 as a convenient mental shortcut to understanding the impact of inflation.

The rule says: Rate of doubling * Time in years = 72

Rule of 72 lets us quickly calculate the impact of inflation over time. For example, using the rule, we can see that the purchasing power of money halves every ten years at 7% inflation. For example, one crore worth today will be worth around 50 lakhs in 10 years and 25 lakhs in 20 years.

| Years needed to reach 1 cr |

Value of 1cr at 7% inflation (lakhs) |

Value of 1cr at 8% inflation (lakhs) |

Value of 1cr at 9% inflation (lakhs) |

|---|---|---|---|

| 5 | ₹ 71.30 | ₹ 68.06 | ₹ 64.99 |

| 6 | ₹ 66.63 | ₹ 63.02 | ₹ 59.63 |

| 7 | ₹ 62.27 | ₹ 58.35 | ₹ 54.70 |

| 8 | ₹ 58.20 | ₹ 54.03 | ₹ 50.19 |

| 9 | ₹ 54.39 | ₹ 50.02 | ₹ 46.04 |

| 10 | ₹ 50.83 | ₹ 46.32 | ₹ 42.24 |

| 11 | ₹ 47.51 | ₹ 42.89 | ₹ 38.75 |

| 12 | ₹ 44.40 | ₹ 39.71 | ₹ 35.55 |

| 13 | ₹ 41.50 | ₹ 36.77 | ₹ 32.62 |

| 14 | ₹ 38.78 | ₹ 34.05 | ₹ 29.92 |

| 15 | ₹ 36.24 | ₹ 31.52 | ₹ 27.45 |

Therefore investing too conservatively, if the target is to reach the first crore, will make the real value of that ₹1 crore too low to be of much use once finally reached.

We will approach this problem step-by-step:

Yes, but only with a long investment horizon spanning decades. Even at 12% annual returns, ₹5,000 per month (with 10% annual step-up) grows to approximately ₹1 crore in about 30 years.

At 12% returns and 10% annual step-up, the required SIP is roughly ₹30,594 per month. At 14% returns, it drops to around ₹27,847 per month.

Over long periods, diversified equity funds in India have historically delivered returns in the 10-15% range, making 12% a common planning assumption. Short-term returns can vary widely and should not be considered for planning.

Yes. A step-up SIP strategy, where you increase your SIP by 5-10% annually, significantly reduces the starting SIP required to reach ₹1 crore. It also makes reaching the target of ₹1 crore faster. For example, if you can invest ₹50,000/month at 12% returns then a fixed-SIP can get you to ₹ 1 crore in 14 years, while a 10% step-up will get you there in 11 years for the same starting amount.

For long time horizons, diversified funds like multi-asset can be used as the core fund of the portfolio with multiple satellite funds for tactical bets. For short time horizons, debt or some hybrid funds offer less volatility at the cost of taking longer to reach the target.

A lump sum can reach the goal faster if invested early. However, SIPs reduce timing risk and are easier for most investors to sustain monthly since investors have salary income.

With official inflation at 5-6%, the purchasing power of ₹1 crore will fall over time. The Rule of 72 shows that the value of ₹1 crore will be ₹50 lakhs in 10 years and ₹25 lakhs in 20 years at just 7% inflation.

Yes. Most mutual fund platforms allow pausing SIPs without penalty. However, pausing reduces corpus growth and may require a higher SIP later.

Yes. The total monthly investment across funds is what matters. Multiple smaller SIPs diversify the portfolio without affecting the total target corpus. Too many funds however, create clutter that reduces returns and makes it difficult to manage.

Annual reviews are typical. Adjustments may be needed based on income changes, performance deviations, or changes in your target duration. Use the Arthgyaan SIP Calculator for Target Amount to find out how much you need to still invest based on where you are on your investment journey.

Published: 18 December 2025

8 MIN READ

1. Email me with any questions.

2. Use our goal-based investing template to prepare a financial plan for yourself.Don't forget to share this article on WhatsApp or Twitter or post this to Facebook.

Discuss this post with us via Facebook or get regular bite-sized updates on Twitter.

More posts...Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled How Much SIP You Need to Reach 1 crore? first appeared on 29 Nov 2025 at https://arthgyaan.com