We review the new LIC Amritbaal insurance cum investment plan so that parents are aware that the plan is not good for most people. We will also show what to do instead for your kid’s goals.

We review the new LIC Amritbaal insurance cum investment plan so that parents are aware that the plan is not good for most people. We will also show what to do instead for your kid’s goals.

This article is a part of our detailed article series on avoidable investment plans for your children. Ensure you have read the other parts here:

This article discusses the corpus projections shared officially when launching the NPS Vatsalya scheme and how parents should be aware of the danger of ignoring inflation.

This article discusses the NPS Vatsalya scheme that does not make any sense as a product for anyone even if you plan to invest for your children’s retirement.

We will discuss this point in detail in this article.

It facilitates accumulation of corpus through Guaranteed Addition

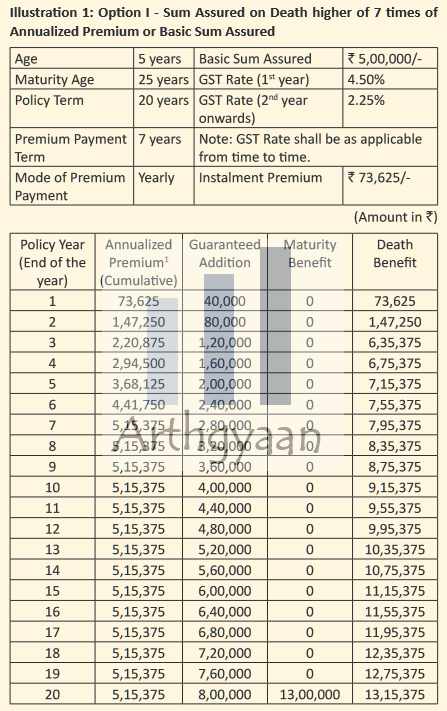

This is the hook that brings in parents. The brochure says “Guaranteed Addition ₹80 per thousand Basic Sum Assured throughout the Policy Term” and many people interpret this as an 8% return. We will explain how this calculation works and how the return, though guaranteed, is not 8%.

This policy ignores the risk of the earning parents dying and not leaving behind enough money for the child. Instead of insuring the more likely risk of the premature death of the parent,

this policy pays out money if the child dies.

This is absurd. The insurance is taken on the life of a kid who is not yet 13 at the time of buying the policy. This will be harsh but it should be obvious that the target market for this plan is people who plan to financially benefit from their own child’s death.

Most people should give up on considering this plan and jump to the alternatives section by clicking the link below:

Entry age (of the child): The policy is bought for a child from birth up to age 13

Maturity age (of the child): From 18 to 25

Premium payment can be one-time or for the first few years (limited time)

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

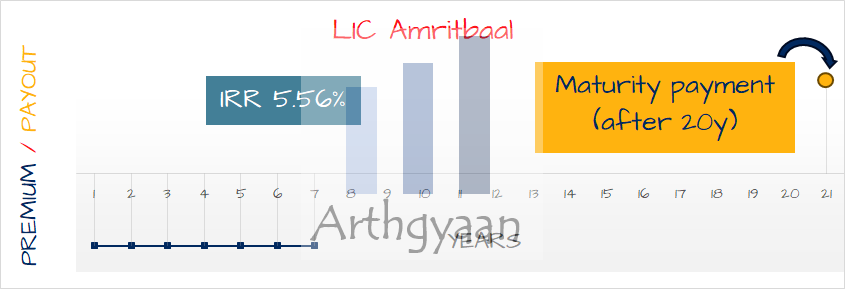

Returns offered (IRR) of the plan

No, it is not 8%. That would be remarkable and it is very clearly not so. The plan offers ₹80 per 1000 of the sum assured (8%) as a guaranteed addition. But this amount is paid at the end. It is not paid every year and therefore does not compound.

a return component which is handily beaten, without any risk and with a full government guarantee, by PPF (7.10% tax-free) or Sukanya Samriddhi Yojana (for girl children, currently offering 8.20%, also tax-free)

Of course, investors willing to take a bit more risk, which they should to beat educational inflation (7-10%), have the option of investing in equity and debt markets via mutual funds.

Start Building Wealth with Expertly Curated Mutual Fund Packages

The whole family, i.e. child and parents should also have sufficient health insurance. This step prevents loss of income or a setback to investment goals due to illness.

Step 3: Make an investment plan to cover your child

Children’s education and other goals do not exist in isolation. They are a part of the comprehensive goal-based planning that parents need to do for their own retirement and everything else. The process is explained best with these examples:

To implement all of the above steps in one easy-to-follow bundle, we have Arthgyaan Child Education goal packages. Choose the year closest to your desired college admission year to get started:

Frequently Asked Questions (FAQs)

What is the IRR of LIC Amritbaal policy?

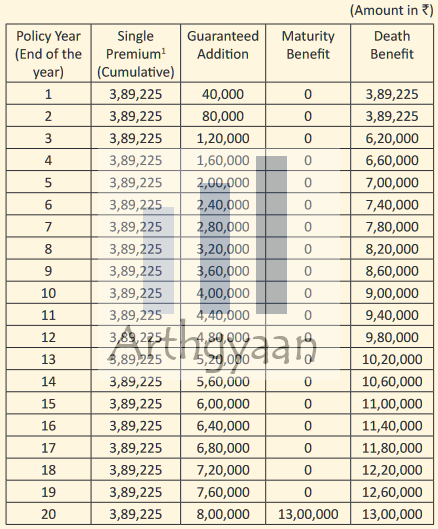

The IRR of LIC Amritbaal policy is 5.56% for a 20-year term with 7 years of premium payment. For the single premium 20-year plan, the IRR is 6.22%

Is the LIC Amritbaal policy a good plan for children?

The LIC Amritbaal policy is not a good plan. This plan insures the life of the child which is not needed and the return offered is a poor 5.56%-6.22%. PPF, Sukanya Samridhhi, and mutual funds offer better returns. Instead of the child, parents should insure themselves via a term plan

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Why LIC Amritbaal policy is a complete wastage of money: how to invest for your child in the right way first appeared on 22 Feb 2024 at https://arthgyaan.com