This article describes the tax benefits announced in Budget 2025 for the NPS Vatsalya Scheme to understand if these benefits make NPS Vatsalya a good scheme for children’s future.

This article describes the tax benefits announced in Budget 2025 for the NPS Vatsalya Scheme to understand if these benefits make NPS Vatsalya a good scheme for children’s future.

This article is a part of our detailed article series on Union Budget 2025. Ensure you have read the other parts here:

This article gives a high-level overview of the most important points which affect your portfolio and taxation in Union Budget 2025 for both residents and NRIs.

This article describes the tax benefits announced in Budget 2025 that can be used by NRIs planning to retire in India to create a tax-free and inflation-indexed passive income stream.

This article describes how to use the Arthgyaan goal-based investing tool as a calculator to determine if switching to the New Tax Regime makes sense from 1st April 2025.

This article explores using the NPS Vatsalya scheme for grandparents to transfer wealth to their grandchildren by gifting them a large corpus to be used to create a pension income stream.

This article discusses the corpus projections shared officially when launching the NPS Vatsalya scheme and how parents should be aware of the danger of ignoring inflation.

This article discusses the NPS Vatsalya scheme that does not make any sense as a product for anyone even if you plan to invest for your children’s retirement.

Is NPS Vatsalya Scheme a good scheme at all for your children?

Before coming to the tax-deduction introduced in Union Budget 2025 let us first recap the features of the NPS Vatsalya Scheme:

this is an NPS account for children and parents will contribute to it before the child turns 18

once the child turns 18, it becomes their normal NPS account

NPS Vatsalya Scheme account can be opened with ₹1,000 and subsequent contributions have to be at least ₹1,000/year. There is no maximum cap on contributions

up to 25% of the invested amount (not the corpus value) can be withdrawn three years after opening the account for education, illness and disability for up to three times

We still fail to see what is the benefit of this particular scheme. We have argued against the NPS Vatsalya Scheme using various points:

Does your child really need a pension plan?

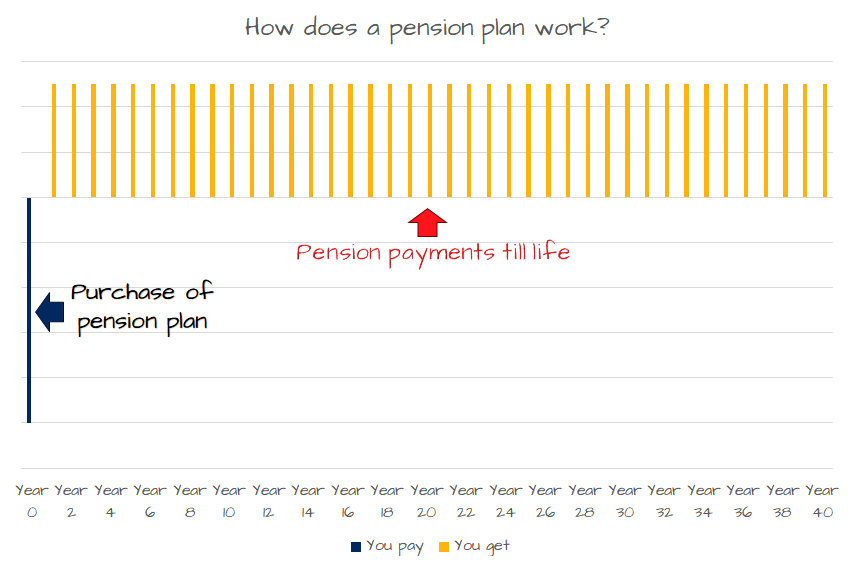

A pension plan gives you money every year until life. Pension is a fantastic product that made a lot of sense in the socialist world of the 1960s-2000s India but is meaningless today. Here are the reasons why we say so:

Pension plans offer fixed payouts which do not grow with inflation

40-60 years later, when these pensions start, India will be more developed and just like Western developed nations, pension yields will be much lower than today

Is the NPS Vatsalya Scheme the only way for your child to get a pension after retirement?

No, of course not.

A pension plan, very simply, is a deal between an insurance company and you to get regular sums of money until death in exchange for a large lump-sum payment today.

If you invest in NPS, the government makes it a rule to invest at least 40% of the corpus reached at the age of 60 into a pension plan while the rest is given to you tax-free. You can, of course, invest more than 40% also in the pension plan.

Here are two important points regarding the pension plan:

you don’t need NPS to buy a pension plan. You can go to any insurance company and buy a pension plan today

the pension you get depends on the investments you make over time to reach the corpus at the age of 60

As a parent do you really need the NPS Vatsalya Scheme as an investment product today?

We will ask the parent, looking at the NPS Vatsalya Scheme for their child, these three questions:

Highest priority: Are you investing enough for your own retirement?

Medium priority: Are you investing enough for your child’s education?

Lower priority: Are you investing enough for your child’s first house?

If the answer to any of the above questions is a “No” or “Maybe” then NPS Vatsalya Scheme is not for you.

The only use case of NPS Vatsalya Scheme that we can reasonably justify is generational wealth transfer from grandparents to grandchildren cognisant of the lock-in until the child turns 60: Can NPS Vatsalya be used to create wealth across generations?

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Start Building Wealth with Expertly Curated Mutual Fund Packages

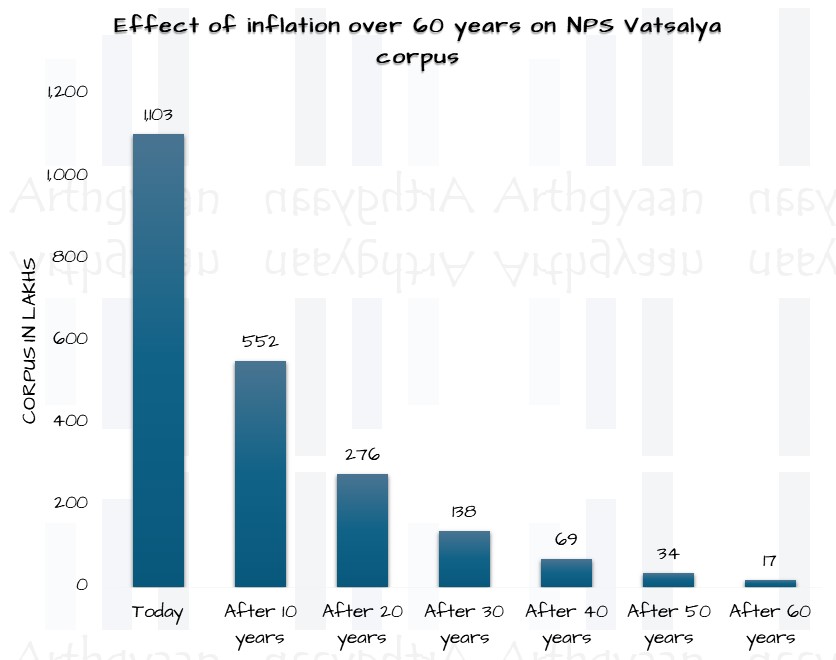

Also, ₹50,000/year will not create any meaningful corpus after 60 years due to six decades of inflation where the value of money halves every 10 years like this:

If the NPS Vatsalya Scheme corpus reaches ₹11 crores as per this projection shared by Press Information Bureau in 2024 at the time of announcement of NPS Vatsalya Scheme, then we need to adjust that for inflation

A quick mental maths shortcut to calculate this is:

All in all, there is no justification to start a NPS Vatsalya Scheme just for the tax deduction. There are many alternatives that will be suitable for most people.

What are the alternatives to investing in NPS Vatsalya Scheme?

We are not saying that NPS Vatsalya Scheme is bad. We are saying that better alternatives with full flexibility and more options exist once you follow the process described below step-by-step:

Step 1: Identify your child’s goals

Your child’s school and other regular expenses will come from monthly income. But you need to plan for bigger expenses in advance:

The whole family, i.e. child and parents should also have sufficient health insurance. This step prevents loss of income or a setback to investment goals due to illness.

Step 3: Make an investment plan to cover your child

Children’s education and other goals do not exist in isolation. They are a part of the comprehensive goal-based planning that parents need to do for their own retirement and everything else. The process is explained best with these examples:

To implement all of the above steps in one easy-to-follow bundle, we have Arthgyaan Child Education goal packages. Choose the year closest to your desired college admission year to get started:

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Budget 2025: what income tax benefits are there for NPS Vatsalya? Is it good for children? first appeared on 01 Feb 2025 at https://arthgyaan.com