This article discusses the NPS Vatsalya scheme that does not make any sense as a product for anyone even if you plan to invest for your children’s retirement.

This article discusses the NPS Vatsalya scheme that does not make any sense as a product for anyone even if you plan to invest for your children’s retirement.

This article is a part of our detailed article series on avoidable investment plans for your children. Ensure you have read the other parts here:

This article discusses the corpus projections shared officially when launching the NPS Vatsalya scheme and how parents should be aware of the danger of ignoring inflation.

We review the new LIC Amritbaal insurance cum investment plan so that parents are aware that the plan is not good for most people. We will also show what to do instead for your kid’s goals.

Union Budget 2024 introduced the concept of the NPS Vatsalya Scheme. This scheme allows parents to open an NPS account for their child and contribute to it. Once the child becomes an adult at 18, this NPS Vatsalya Scheme account will become the child’s own NPS account for their retirement at the age of 60. There are no tax deductions available to the parent if they invest in the NPS Vatsalya Scheme.

This article is a part of our detailed article series on the NPS Vatsalya scheme. Ensure you have read the other parts here:

This article describes the tax benefits announced in Budget 2025 for the NPS Vatsalya Scheme to understand if these benefits make NPS Vatsalya a good scheme for children’s future.

This article explores using the NPS Vatsalya scheme for grandparents to transfer wealth to their grandchildren by gifting them a large corpus to be used to create a pension income stream.

This article discusses the corpus projections shared officially when launching the NPS Vatsalya scheme and how parents should be aware of the danger of ignoring inflation.

Why is the NPS Vatsalya Scheme an unnecessary gimmick?

We need to understand which problem the NPS Vatsalya Scheme is supposed to solve. Let us ask these questions and answer them:

What is the parent supposed to invest for by opening this NPS Vatsalya Scheme account?

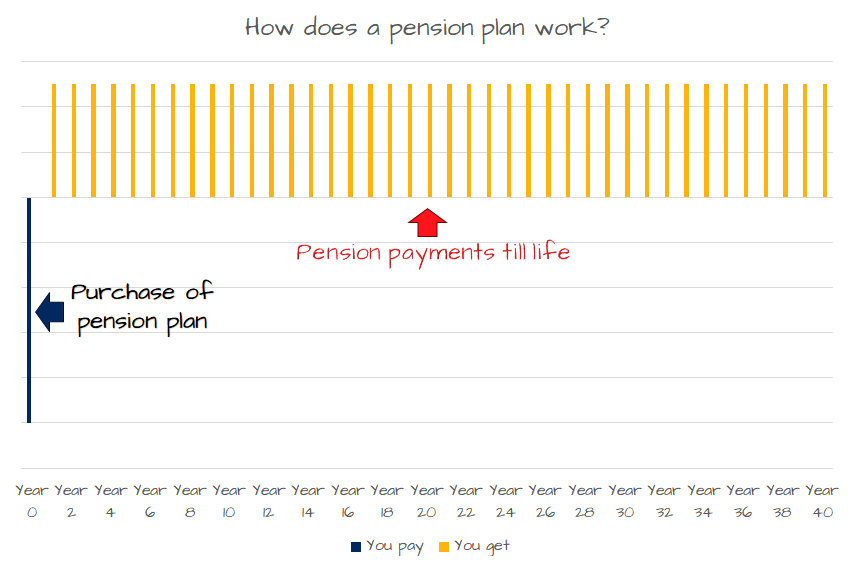

The NPS Vatsalya Scheme account is for the “retirement” of the child and not that of the parent.

When will the NPS Vatsalya Scheme account mature?

For a minor child, the account will mature at least 42 years later when the child turns 60 as per the current NPS rules. In fact, the age of the child and the NPS Vatsalya Scheme account maturity period look like this:

Age of child

Years until maturity

1

59

2

58

3

57

4

56

5

55

6

54

7

53

8

52

9

51

10

50

11

49

12

48

13

47

14

46

15

45

16

44

17

43

Does opening the NPS Vatsalya Scheme account mean that the child enjoys 4 or more decades of compounding?

That is true since the maturity of the NPS Vatsalya Scheme is more than 40+ years as per the table above. So there is immense potential for growth.

But then, why is this an avoidable gimmick?

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Do you really need the NPS Vatsalya Scheme as an investment product today?

We will ask the parent, looking at the NPS Vatsalya Scheme for their child, these three questions:

Highest priority: Are you investing enough for your own retirement?

Medium priority: Are you investing enough for your child’s education?

Lower priority: Are you investing enough for your child’s first house?

If the answer to any of the above questions is a “No” or “Maybe” then NPS Vatsalya Scheme is not for you. You have more important and urgent goals to take care of:

One day you will retire. This is an unavoidable fact of life. Where will the money come from to spend in retirement?

Your child may not get admission to a subsidised government college like AIIMS that costs a few thousand a year. Even the cheapest IIT degree costs 10+ lakhs. Where will that money come from? Your own funds or educational loans?

We are in a boom in real estate as the country matures and the same price appreciation happens in real estate across the rest of India as seen abroad (New York, San Francisco, London etc.) and closer to home in Mumbai. How much of your child’s first salary will go into rent?

Start Building Wealth with Expertly Curated Mutual Fund Packages

Why is the NPS Vatsalya Scheme an avoidable gimmick?

If after all of these considerations, you are still interested in NPS Vatsalya Scheme then we have more questions for you:

Can you not get the same results via, say, mutual funds? After all, mutual funds also invest in stocks and bonds and do not force you to keep the money locked for 40-60 years.

Are you afraid that you are not disciplined in investing and will pull out the money invested for the child’s use if not locked in? Retirement is a multi-decade and multi-crore corpus creation journey. If you are not disciplined to be on this journey then your own retirement will be at risk. Pulling out some amount from the child’s mutual funds will not make too much of a difference in this case unless you have a medical or similar emergency.

What about funds needed in dire emergencies? NPS allows only 20% corpus withdrawal if withdrawn before age 60. The rest must be used to buy a pension plan (or annuity). If there is a substantial amount in NPS that you need for an emergency, then you cannot get to it.

What if your child decides to retire early before age 60? NPS locks up your money up to 60. How will your child use the corpus if they want to leave their job at 40 and decide to start a business?

In the end, there is one more point that we need to mention here. Every investment has multiple criteria for checking suitability:

We have so far addressed the Liquidity aspect here since the investment is locked until maturity. Now we will address the second L i.e. Legal / regulatory (L):

What if in a future budget the tax-free withdrawal of 60% of the NPS corpus rule is removed making NPS taxable?

What if returns on the pension plan that you are forced to purchase with 40% of your NPS corpus have very poor interest rates?

What if the proportion of corpus needed to compulsorily purchase an annuity gets increased to more than 40%?

Since NPS is essentially a mutual fund with extra rules around liquidity and regulatory aspects, there is very little justification to open up another NPS account just for your child.

What are the alternatives to investing in NPS Vatsalya Scheme?

We are not saying that NPS Vatsalya Scheme is bad. We are saying that better alternatives with full flexibility and more options exist once you follow the process described below step-by-step:

Step 1: Identify your child’s goals

Your child’s school and other regular expenses will come from monthly income. But you need to plan for bigger expenses in advance:

The whole family, i.e. child and parents should also have sufficient health insurance. This step prevents loss of income or a setback to investment goals due to illness.

Step 3: Make an investment plan to cover your child

Children’s education and other goals do not exist in isolation. They are a part of the comprehensive goal-based planning that parents need to do for their own retirement and everything else. The process is explained best with these examples:

To implement all of the above steps in one easy-to-follow bundle, we have Arthgyaan Child Education goal packages. Choose the year closest to your desired college admission year to get started:

Here are some FAQs on NPS Vatsalya Scheme for those who wish to learn more about it

Please use the Find feature of your browser to look for specific items of interest.

What is the NPS Vatsalya Scheme?

The NPS Vatsalya Scheme, introduced in Budget 2024, is a National Pension Scheme (NPS) designed specifically for minors. Parents and guardians can open an NPS account for their children and make contributions until the child turns 18. Upon reaching adulthood, the account can be converted into a regular NPS account.

Who is eligible to open an NPS Vatsalya account?

All parents and guardians, including Indian citizens, NRIs, and OCIs, are eligible to open an NPS Vatsalya account for their minor children.

What are the benefits of the NPS Vatsalya Scheme?

The benefits include promoting early savings habits, providing a substantial retirement corpus, ensuring portability of the account, and teaching children responsible financial management. The account can be converted to a standard NPS account upon the child reaching adulthood.

How does the NPS Vatsalya Scheme promote savings habits in children?

By opening an NPS Vatsalya account for minors, parents can teach children to save and invest from an early age. Once the child turns 18, they can manage and contribute to the account independently.

What happens to the NPS Vatsalya account when the child turns 18?

The NPS Vatsalya account is converted into a regular NPS account, which the child can manage and contribute to independently.

Can parents contribute to the NPS Vatsalya account on behalf of their children?

Yes, parents and guardians can make regular contributions to the NPS Vatsalya account on behalf of their children until they turn 18.

Frequently Asked Questions (FAQs)

What is the NPS Vatsalya Scheme?

The NPS Vatsalya Scheme, introduced in Budget 2024, is a National Pension Scheme (NPS) designed specifically for minors. Parents and guardians can open an NPS account for their children and make contributions until the child turns 18. Upon reaching adulthood, the account can be converted into a regular NPS account.

Who is eligible to open an NPS Vatsalya account?

All parents and guardians, including Indian citizens, NRIs, and OCIs, are eligible to open an NPS Vatsalya account for their minor children.

What are the benefits of the NPS Vatsalya Scheme?

The benefits include promoting early savings habits, providing a substantial retirement corpus, ensuring portability of the account, and teaching children responsible financial management. The account can be converted to a standard NPS account upon the child reaching adulthood.

How does the NPS Vatsalya Scheme promote savings habits in children?

By opening an NPS Vatsalya account for minors, parents can teach children to save and invest from an early age. Once the child turns 18, they can manage and contribute to the account independently.

What happens to the NPS Vatsalya account when the child turns 18?

The NPS Vatsalya account is converted into a regular NPS account, which the child can manage and contribute to independently.

Can parents contribute to the NPS Vatsalya account on behalf of their children?

Yes, parents and guardians can make regular contributions to the NPS Vatsalya account on behalf of their children until they turn 18.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled NPS Vatsalya: A Gimmicky Product That Should Be Avoided If You Are Serious About Investing For Your Children first appeared on 26 Jul 2024 at https://arthgyaan.com