What is the concept of the bucket portfolio for retirees?

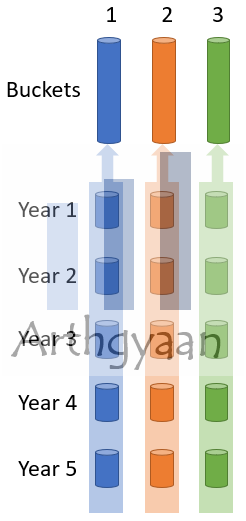

The concept of the 3-bucket retirement portfolio creates three risk-based asset pools or buckets within the retirement portfolio:

Bucket 1: Cash for short-term expenses (3-5 years) and emergency fund (12 months of expenses)

Bucket 2: Debt assets for portfolio stability and income

Bucket 3: Inflation-beating assets like equity mutual funds and direct equity stocks

In this article, we will discuss how retirees can distribute different investments, measured by sources of risk, across the various portfolio buckets to achieve the right mix of risk and returns.

What are the various sources of risk that contribute to a retiree’s portfolio?

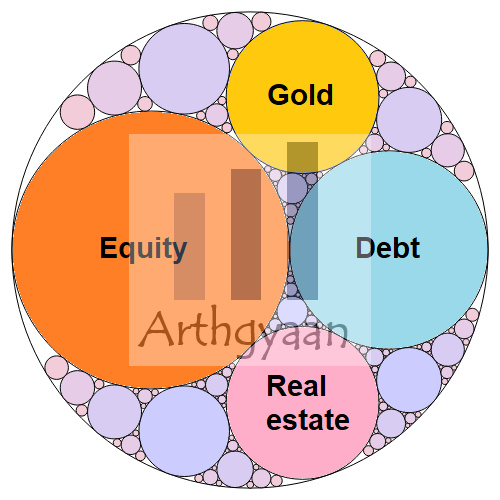

We can use a diagram like this to visualise the universe of investable asset classes, which you can use to create a portfolio. Typically, these include:

Equity via direct investment in stocks or through mutual funds.

Debt via bonds or mutual funds.

Real estate via residential and commercial property or REITs.

Gold via jewellery, SGB, or gold mutual funds.

Alternatives like precious metals (e.g., silver funds, which are now available in India), art, private equity, etc.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

What are the different risk profiles applicable to retirees?

We will categorise the retiree population into three risk-based categories:

Low-risk profile

Medium-risk profile

High-risk profile

A high-risk profile investor typically meets multiple of these criteria:

A large portfolio relative to projected first-year expenses

Access to unbiased investment advice

The ability and willingness to manage the retirement portfolio themselves or with the help of a capable family member

Excellent physical and mental health for both spouses

One or more passive income streams (dividends, royalties, pension, etc.)

Children with stable careers and incomes

Family members who are informed and involved in the portfolio’s structuring and maintenance

Sufficient health insurance coverage

The risk profile moves from high to medium to low as more of the points above become false or inapplicable for the retiree. Ultimately, the investor’s risk profile is the less risky option based on their ability to take risks (measured by the points above) and their willingness to do so.

Start Building Wealth with Expertly Curated Mutual Fund Packages

What are the risk factors that may be suitable for a low-risk retiree portfolio?

Bucket 1: Cash for short-term expenses (7-10 years) held in major nationalised or SIFI banks in savings accounts, sweep fixed deposits (FDs), and regular FDs.

Bucket 2: Debt assets for portfolio stability and income, held in government schemes like PPF, Post Office Monthly Income Scheme, Senior Citizens Savings Scheme (SCSS), and similar plans. Government bonds purchased from RBI Retail Direct can also be a part of this bucket. Interest (from the government schemes) and coupon (from the bonds) payments can fund the cash in Bucket 1.

Bucket 3: Inflation-beating assets like large-cap equity mutual funds can be an optional part of this bucket.

What are the risk factors that may be suitable for a medium-risk retiree portfolio?

In this risk profile, we focus on tax optimisation and take on a slightly higher level of risk. We increase the allocation to mutual funds to take advantage of professional management and tax deferral.

Bucket 1: Cash for short-term expenses (5-7 years) held in banks (as above) or in arbitrage or liquid/money market mutual funds, which are more tax-efficient.

Bucket 2: In addition to government schemes, you can make an additional allocation to debt mutual funds with zero to minimal credit risk and minimal interest rate risk. Debt funds that invest in short-dated (maturing within five years) government bonds (beyond 364-day Treasury Bills) can be an option here.

Bucket 3: Equity mutual funds investing in mid-cap (or even small-cap) stocks can be an additional investment option.

What are the risk factors that may be suitable for a high-risk retiree portfolio?

In this risk profile, we focus adding different sources of risk for portfolio diversification which will require professional management going forward.

Bucket 1: Cash for short-term expenses (3-5 years) held in sweep FDs in banks (for only the emergency fund), with the rest in arbitrage or money market mutual funds.

Bucket 2: In addition to short-dated gilt funds, you can also invest in long-term gilt funds, noting that these funds can fluctuate significantly with interest rate movements.

Bucket 3: Equity mutual funds investing in international stocks (to reduce single-country/single-currency risk) and a small allocation to alternative investments like gold/silver and REITs can be added to this mix. Direct stocks can also be in this bucket, with any dividend payments contributing to the cash in Bucket 1.

Ready-made goal-linked mutual fund packages related to this article

You can look at Arthgyaan Packages for making your retirement planning simpler. Each Arthgyaan Package is a structured investment plan for retirement, ensuring financial security in later years through systematic wealth accumulation tagged to a particular retirement year. A package encapsulates the portfolio creation assumptions (equity / debt / cash asset returns, inflation, longevity and rebalancing plan) and creates a mutual fund (and EPF, PPF and NPS if applicable) portfolio.

Choose the year closest to your desired retirement year to get started:

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Retirement Portfolio Strategy: How to Allocate Equity, Debt, and Cash Buckets for Maximum Security and Growth first appeared on 14 Aug 2024 at https://arthgyaan.com