This article brings together the interrelationship between the size of the retirement corpus, inflation, asset returns, longevity and the amount you wish to spend in retirement.

This article brings together the interrelationship between the size of the retirement corpus, inflation, asset returns, longevity and the amount you wish to spend in retirement.

The article investigates if you can retire in India with only 25x your expenses saved as retirement corpus.

Challenges in Retirement Planning: Longevity, Inflation, and Portfolio Returns

“nastiest, hardest problem in finance.” - William Sharpe, Nobel Prize winner, regarding the withdrawal stage of retirement

This article tries to bring the competing factors in play when deciding on a retirement corpus, early i.e. FIRE or normal or abrupt (when you are phased out of your current role). There are a few things that we need to keep in mind:

Longevity which is a euphemism of saying how long you plan to stay alive since the longer you live, the more money you need

Asset returns and in turn asset allocation since you need to invest in the right mix of low risk (e.g. cash), medium risk (FD, debt mutual funds, coupon paying bonds and rental income etc.) and high risk (like shares and equity mutual funds)

Inflation of both your basics (like food, clothing) and lifestyle (entertainment, travel whether domestic or foreign) and also unexpected costs of chronic or one-time healthcare issues

Starting expenses which is the money you will spend in the first year of retirement which will then increase with inflation

For simplicity, we will exclude any generational wealth you plan to pass on since those must be handled outside the retirement portfolio.

What returns do you need to get based on your corpus size and longevity?

We use the simple IRR function in Excel to estimate the returns. Using the IRR function in Excel or Google Sheets like this for the 5 crore, 12 lakhs, 7% inflation example:

Required real return = Nominal return - Inflation (approximately)

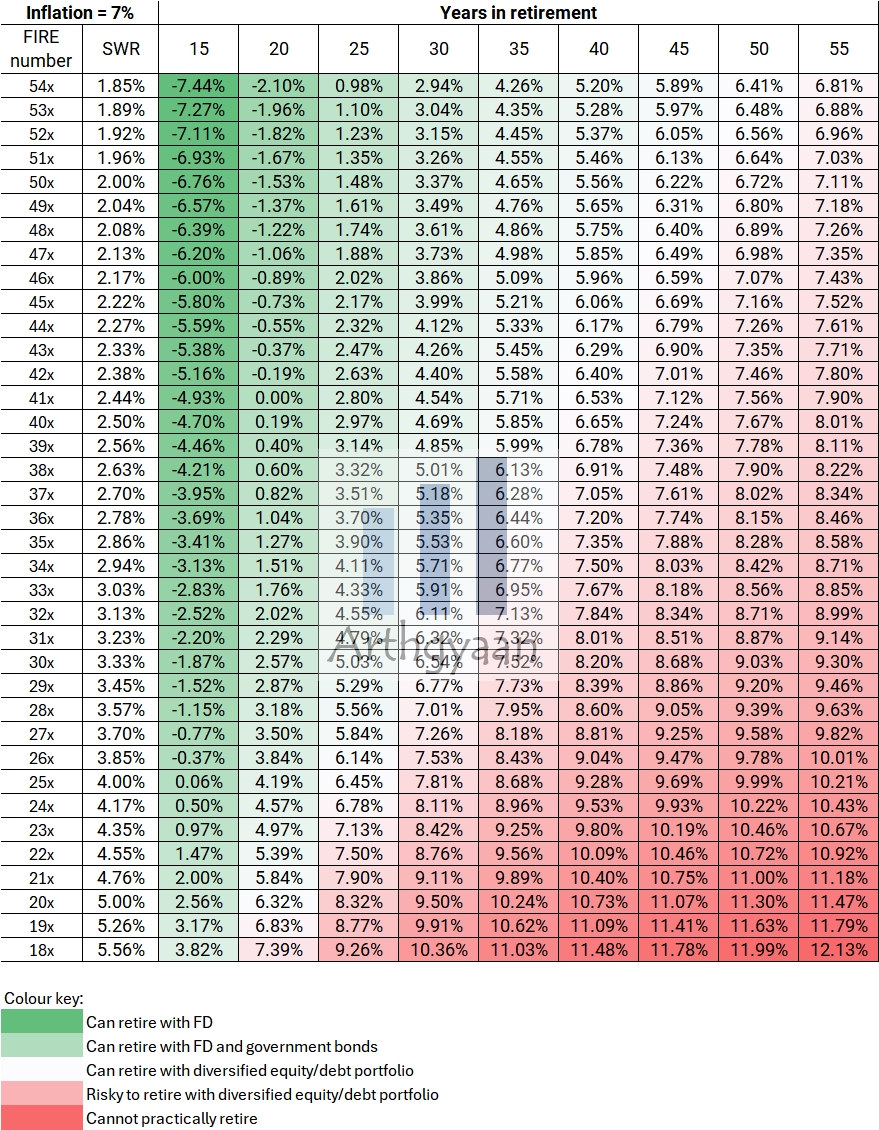

Since it is very common to estimate your retirement expenses and see if you can fit that into your corpus, we will now show a couple of tables of corpus size vs. longevity and see the target return.

Here the basic premise is that if, simplistically speaking, you have ₹10 crores and you spend ₹1 lakh/year, then even an SBI savings account will last you a lifetime. We have covered some of those calculations here: How much returns should you expect from your retirement portfolio?.

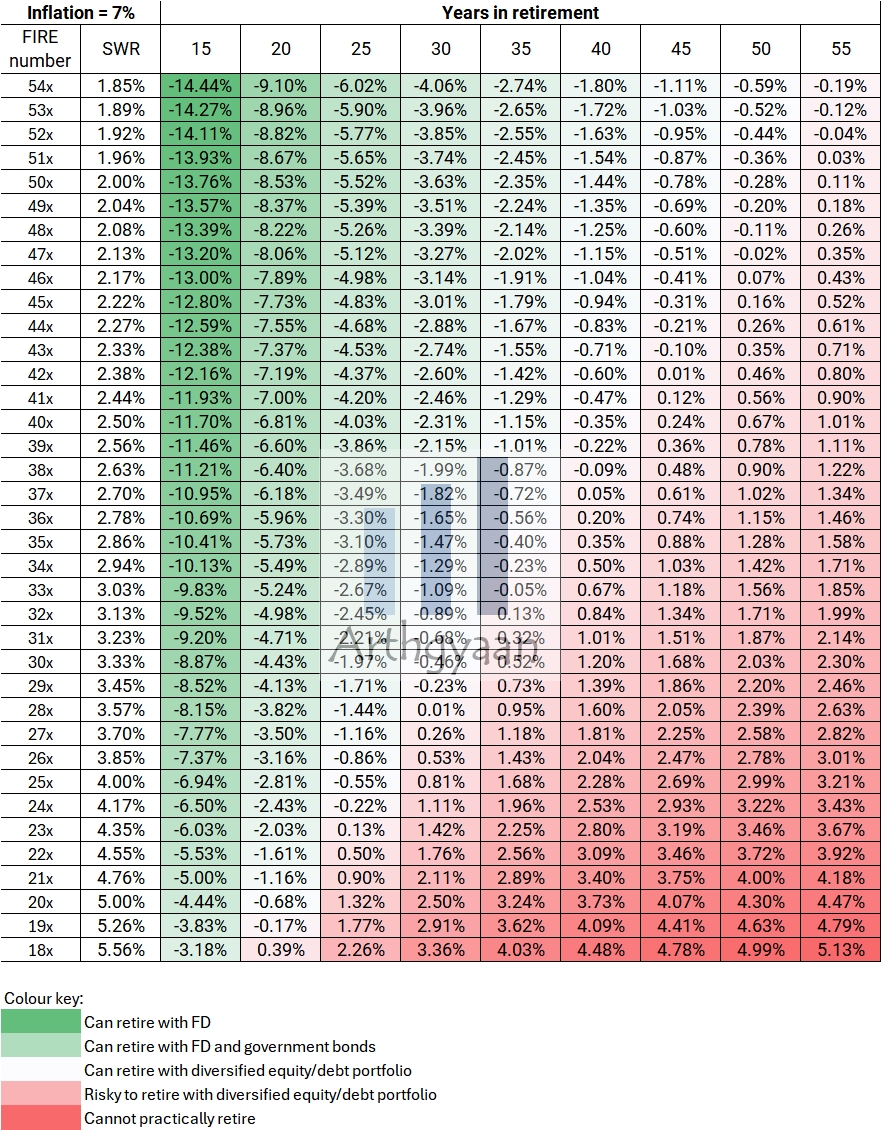

In the charts below, we have used 7% inflation. Real-life inflation due to aspirational items (like foreign travel) and healthcare costs will make this number much higher for most people.

This chart shows that if you think you will live for another 40 years, which is not difficult thanks to modern medicines that will keep you alive longer than you think, and you have 40x corpus already available, then you need just 6.65% lifetime returns from the portfolio. This is not a bad return considering it comes below the 7% inflation.

However, if the corpus available drops to just 35x, the required return jumps to 7.35% which is above inflation and therefore difficult to achieve.

The chart below this shows the same data but with real returns (nominal returns minus inflation).

Once you know the returns you are targeting, you can use this step-up SWP calculator to see how much you can withdraw from your portfolio over the retirement period:

₹

1 Cr

₹

25,000

10%

For this category of funds, we have sampled past returns to create 1000 simulations and show the median result.

Dark green: Huge corpus, low expenses, even FD will work

Lighter green: Good corpus, moderate expenses, FD plus other debt investments will work

Almost white: Decent corpus and matching expenses, 3-bucket portfolio needed

Pink to red: Corpus smaller relative to expenses, risky with a 3-bucket portfolio

Red: Insufficient corpus, will likely run out of money at some point before the desired end of retirement

These charts can be used to answer the following questions:

Can I FIRE now if I have a corpus of 2 crores?

You can divide the corpus by your expenses and then look up the figures as per your age which will give you the number of years in retirement. Once you have the required return figure, see in which zone it falls: red, white or green and get the answer from there. In some cases, you might wish to defer your FIRE plan.

Can I FIRE when I reach the age of 50?

The planning aspect will depend on the amounts already invested and the desired life-style expenses. A worked out case study is presented below:

Can I retire with FD if I don’t want to invest in the stock market?

If your corpus and expenses are mostly in the green zone, then you will be mostly fine with just FD. Flooring the retirement income via an annuity (i.e. pension plan), so that your income never falls below the pension amount.

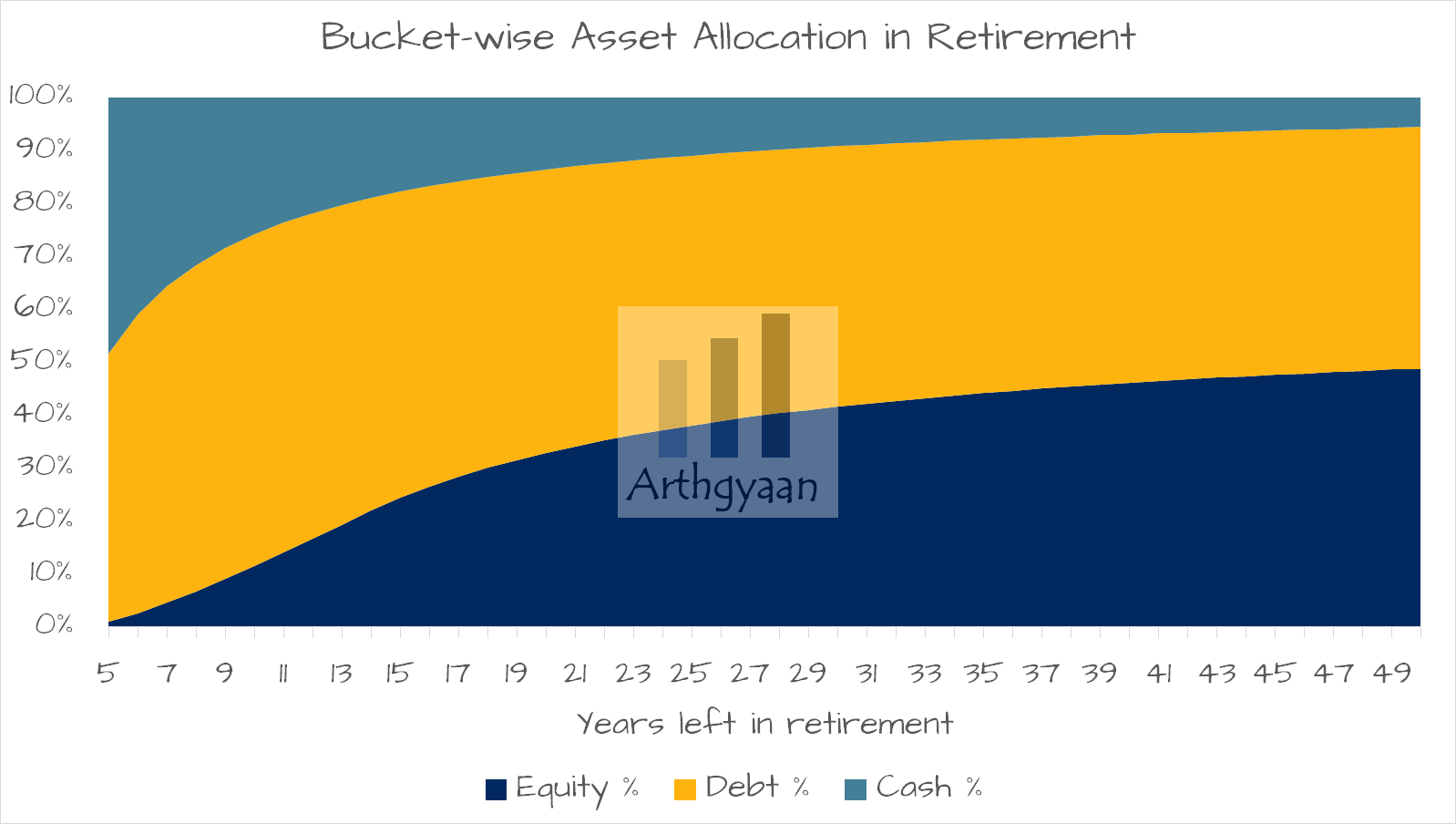

How much should I put in the stock market when I am retired?

Ready-made goal-linked mutual fund packages related to this article

If you are planning your FIRE journey, then Arthgyaan packages can help you create and manage your FIRE portfolio effortlessly. Choose the year closest to your desired FIRE year to get started:

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Safe Withdrawal Rates and Required Portfolio Returns For Retirement Planning first appeared on 06 Jan 2025 at https://arthgyaan.com