This article explores the math behind matching your EMI to your rent, highlights the role of rental yield and loan tenure, and helps you understand why leveraging your house purchase is a good decision.

This article explores the math behind matching your EMI to your rent, highlights the role of rental yield and loan tenure, and helps you understand why leveraging your house purchase is a good decision.

What are the Rules for Calculating Rent vs. EMI When Buying a House?

If you buy a house on a home loan, here are a few rules you need to be aware of:

The bank caps the loan to no more than 75% of the house price

You need to provide a down payment of at least 25%

Closing costs like registration/stamp duty, TDS (which is very large if you are buying from an NRI), interiors, brokerage and shifting charges are not included as the loan

Your EMI depends on the interest rate and loan tenure. Since we plan to pay no more than the rent of the same house as the EMI, we will take the longest period loan possible and pay it off earlier via salary hikes.

The bank will not generally grant a loan beyond your official retirement age (58-60 years usually). So depending on your current age, and how you structure the loan, your EMI can be lower by stretching out the loan.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Doesn’t paying off a home loan for many years mean that you are paying a lot of interest?

Yes. That is a good thing actually assuming you take the benefit of leverage.

Leverage means using a loan to acquire assets that appreciate over time

A house is the only asset you can finance on loan apart from a college degree. No bank will give a loan for investing in its own share let alone the stock market. Car loans don’t count as well since cars are depreciating assets.

Now we will explain why prepaying a home loan is not a good idea if the only goal is to save interest.

Firstly, some basics:

EMI payment is compulsory

Prepayment is paying some amount over and above the EMI and is optional

If you have the extra money to pay over and above the EMI, you should first ask yourself:

Is this money really extra money?

Can it not be invested for long-term goals like retirement?

Can this not be used to say pay for my kid’s college education?

Given that stock markets give higher returns over the long term, isn’t it better to invest in the stock market instead via mutual funds?

Therefore, if your job is stable, you can pay off the loan as long as you need to without rushing to prepay. Of course, psychologically you will mostly feel better about getting rid of the debt. In such cases, you can prepay using a step-up EMI in line with salary hikes.

Start Building Wealth with Expertly Curated Mutual Fund Packages

To reduce the EMI to ₹25,000/month, the loan will be therefore be ₹25 lakhs since EMI will be:

1% of 25 lakhs = ₹25,000 per month

The table below shows the downpayment vs. the loan term and the rental yield like this for the same ₹1 crore house.

Rental yield

Yearly Rent (lakhs)

EMI

15y loan

20y loan

25y loan

30y loan

2.00%

2.00

16,667

83

81

80

79

2.50%

2.50

20,833

79

76

75

74

3.00%

3.00

25,000

75

72

70

68

3.50%

3.50

29,167

71

67

65

63

4.00%

4.00

33,333

67

62

59

58

4.50%

4.50

37,500

62

58

54

52

5.00%

5.00

41,667

58

53

49

47

5.50%

5.50

45,833

54

48

44

42

6.00%

6.00

50,000

50

43

39

36

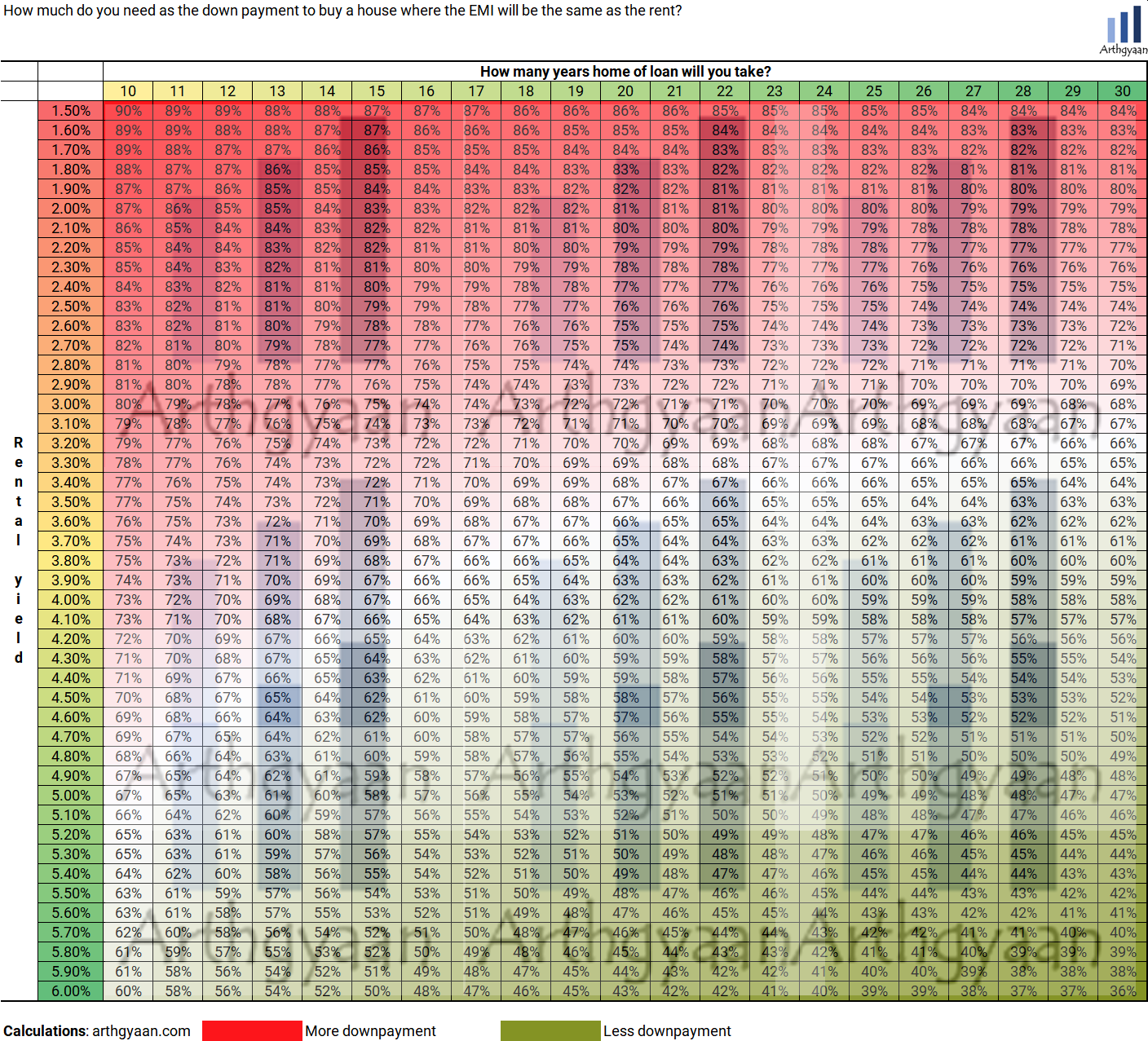

How much do you need as the down payment to buy a house where the EMI will be the same as the rent?

Use the table below effectively with these steps:

Subtract your age from your retirement age to get your maximum loan eligibility (or talk to your bank) - this will give you the column to look for

calculate the rental yield by dividing the annual rent by the price of the house - this will give you the row to look for

Once you have the row and the column, you will get the amount of downpayment as a percentage of the cost of the house.

This calculation is done using an 8.75% average home loan interest rate. Small changes in the interest rate (say 8.4-8.9%) will not materially change the result.

Who should go with this plan of buying a house whose rent and EMI are the same?

Four kinds of individuals and families can look to purchase a house with EMI equal to the rent:

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Can You Buy a House with EMI Equal to Rent? Here's How first appeared on 09 Jan 2025 at https://arthgyaan.com