Section 54F of the Income Tax Act offers a legal way to avoid capital gains tax-if you meet certain conditions. This guide explains how to qualify, maximize your tax exemption, and avoid common mistakes.

Section 54F of the Income Tax Act offers a legal way to avoid capital gains tax-if you meet certain conditions. This guide explains how to qualify, maximize your tax exemption, and avoid common mistakes.

If you ever decide that you will sell your mutual funds to buy a house you will be in for a pleasant surprise. Section 54F of the Income Tax Act says that long-term capital gains, on selling mutual funds, for example, are tax-free if you use that money to buy a house.

This article is a part of our detailed article series on the concept of tax savings using Section 54F. Ensure you have read the other parts here:

Section 54F of the Income Tax Act lets you claim tax exemption if you reinvest in property - potentially saving lakhs. This guide helps you calculate how the exemption works, with eligibility criteria, and key timelines.

If you sell mutual funds, stocks, or gold and use the proceeds to buy or construct a house within the required timeline, you can claim up to 100% capital gains tax exemption under Section 54F - provided you don't own more than one other house at the time of sale. However, if the new house is sold within three years or if you purchase another house within a year, the exemption is reversed, and you must pay tax.

Introduced in 1983, Section 54F of the Income Tax act, as sourced from the Income Tax website, allows us to save capital gains tax if we sell mutual funds to buy a house.

Insertion of new section 54F. 12. In the Income-tax Act, after section 54E, the following section shall be inserted with effect from the 1st day of April, 1983, namely: -

'54F. Capital gain on transfer of certain. capital assets not to be charged in case of investment in residential house.

The basic premise of this tax exemption is very simple:

you wish to buy a house in India as an individual or HUF

you sell Mutual funds, shares, gold etc, to buy the house

on the date of the MF sale, you do not already own more than one house

you don’t have to pay capital gains taxes (only if it is long term gains) on the MF/shares/gold you sold

There is an upper limit of Rs. 10 crores on the exemption amount under Section 54F as per Budget 2023.

We will now break down and analyse each subsection of 54F to understand the terms and conditions implied.

First sub-section: basic terms, timelines and eligibility

The first sub-section as per the act

(explanation follows below)

(1) Where, in the case of an assessee being an individual, the capital gain arises from the transfer of any long-term capital asset, not being a residential house (hereafter in this section referred to as the original asset), and the assessee has, within a period of one year before or after the date on which the transfer took place purchased, or has within a period of three years after that date constructed, a residential house (hereafter in this section referred to as the new asset), the capital gain shall be dealt with in accordance with the following provisions of this section, that is to say,-

(a) if the cost of the new asset is not less than the net consideration in respect of the original asset, the whole of such capital gain shall not be charged under section 45;

(b) if the cost of the new asset is less than the net consideration in respect of the original asset, so much of the capital gain as bears to the whole of the capital gain the same proportion as the cost of the new asset bears to the net consideration, shall not be charged under section 45:

Provided that nothing contained in this sub-section shall apply where the assessee owns on the date of the transfer of the original asset, or purchases, within the period of one year after such date, or constructs, within the period of three years after such date, any residential house, the income from which is chargeable under the head 'Income from house property', other than the new asset.

Explanation.-For the purposes of this section,-

(i) 'long-term capital asset' means a capital asset which is not a short-term capital asset;

(ii) 'net consideration', in relation to the transfer of a capital asset, means the full value of the consideration received or accruing as a result of the transfer of the capital asset as reduced by any expenditure incurred wholly and exclusively in connection with such transfer.

Understanding the first sub-section

Objection: I already own a house, so I can't benefit from Section 54F.

Response: You can still claim this exemption if you own only one house at the time of selling your assets.

Original asset: this is the asset sold to buy the house. This can be Mutual funds, shares, gold, residential land etc. This cannot be another house which comes under Section 54E

Date of sale (DOS): date on which the original asset was sold

New asset: the new house that is constructed / purchased. It must be in India

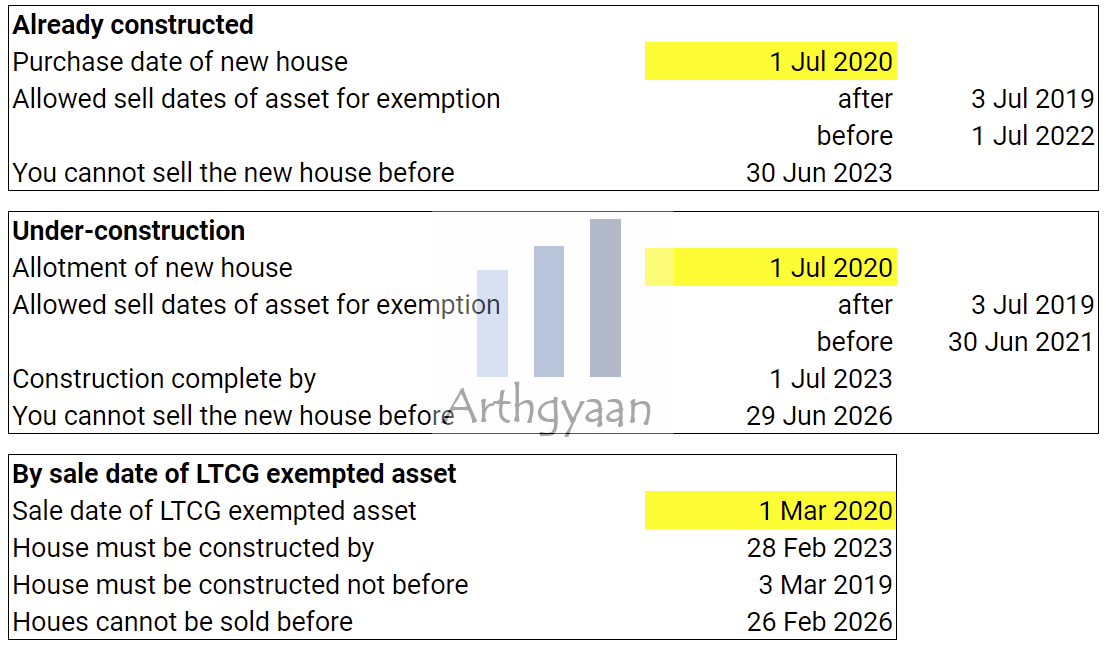

What are the timelines: DOS must be within a year of purchase of the new asset. In case the new asset is being constructed, the construction must finish within three years of DOS

the tax exemption is available only if you already own not more than one house. This rule is thus beneficial if you are buying your first or second house only. It also means that if you have taken the exemption once for your first house, you can take it again for your second house as well

the capital gains must be long term

If your new house costs more than the mutual funds you sold, you can save lakhs in capital gains tax

If the cost of the new asset is X and the sale proceeds from original asset sales is Y, then

if X ≥ Y, i.e. the new house is at least as expensive compared to the sale, then entire capital gains on original assets sale is tax-free

if X < Y, then the capital gains exemption applies proportionally based on the cost of the new asset relative to the sale amount. For example, you sold 20 lakhs of assets and have a capital gains tax of 4 lakhs. The house costs 15 lakhs. The capital gains exempt from tax will be 15/20 * 4 = 3 lakhs. The other 1 lakh of capital gains will be taxable.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Second section: a second house reverses the benefit

The second sub-section as per the act

(explanation follows below)

(2) Where the assessee purchases, within the period of one year after the date of the transfer of the original asset, or constructs, within the period of three years after such date, any residential house, the income from which is chargeable under the head 'Income from house property', other than the new asset, the amount of capital gain arising from the transfer of the original asset not changed under section 45 on the basis of the cost of such new asset as provided in clause (a), or, as the case may be, clause (b), of sub-section (1), shall be deemed to be income chargeable under the head 'Capital gains' relating to long-term capital assets of the previous year in which such residential house is purchased or constructed.

Understanding the sub-second section

Objection: What if I sell my new house later?

Response: If you sell within 3 years, the tax benefit is reversed. So you need to time the sale as per this condition.

If another house is constructed/purchases within the same period (1 year for purchase / 3 year for construction) which is eligible for ‘income from house property’ i.e. given on rent, then the tax benefit received on the new asset construction is reversed and has to be paid in the previous financial year. This rule effectively means that:

you sell 50 lakhs of mutual funds to buy a house (H1). The capital gains tax saved is ₹5 lakhs

within 3 years of the sale of the MF, you buy/construct another house (H2)

then the ₹5 lakh tax becomes payable in the financial year preceding the purchase of H2. This is of course not a problem if you don’t buy H2

Start Building Wealth with Expertly Curated Mutual Fund Packages

(3) Where the new asset is transferred within a period of three years from the date of its purchase or, as the case may be, its construction, the amount of capital gain arising from the transfer of the original asset not charged under section 45 on the basis of the cost of such new asset as provided in clause, (a) or, as the case may be, clause (b), of sub-section (I) shall be deemed to be income chargeable under the head 'Capital gains' relating to long-term capital assets of the previous year in which such new asset is transferred.'.

Understanding the third sub-section

If the new house is sold within three years of purchase / construction, the capital gains tax becomes payable in the financial year preceding the purchase of the house.

We have an easy-to-use calculator for Section 54F exemption calculation

Section 54F Tax Exemption Calculator

How to use the Section 54F Exemption Calculator?

The calculator requires you to enter three numbers, one choice of house type, the number of houses you own today and one date:

Cost of the New House you are planning to purchase

Sale Proceeds of Original Asset, eligible for long-term capital gains, which can be Mutual Funds, Shares, Gold etc. (anything except another property)

Long-term Capital Gains from this sale

The number of houses you own today since you cannot get Section 54F exemption if you own more than one house already

The type of you house you are purchasing: ready-to-move or under-construction

Now you need to enter one of these dates:

purchase date of house in case you know this date either in the past or future

sale date of LTCG exempted asset if you have already sold or plan to sell

Now click the Calculate Exemption button to get the result.

₹

1.00 Cr

₹

50.00 Lakh

₹

30.00 Lakh

A. By purchase date of house

B. By sale date of LTCG exempted asset

If you want to use a Google Sheets / Excel version, please see below:

We will use Google sheets to create a simple calculator for this calculation. There is a link to download a pre-filled copy of the Google sheet via the button below.

Important: You must be logged into your Google Account on a laptop/desktop (and not on a phone) to access the sheet.

Here are some tutorials on using the tool (click the image below)

Please refer to the Sec54F tab of the sheet once you open it. You can export this Sheet to Excel using the File > Download Menu option.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Sec 54F: a hack that can save lakhs in taxes when you buy a house first appeared on 10 Jul 2022 at https://arthgyaan.com