Section 54F of the Income Tax Act lets you claim tax exemption if you reinvest in property - potentially saving lakhs. This guide helps you calculate how the exemption works, with eligibility criteria, and key timelines.

Section 54F of the Income Tax Act offers a legal way to avoid capital gains tax-if you meet certain conditions. This guide explains how to qualify, maximize your tax exemption, and avoid common mistakes.

Sold residential land in 2025. I am buying an under-construction property. Allotment in August 2025. Possession in 2030. Can I avail a capital gains benefit in sec. 54F?

Before addressing the question, we will first examine what Section 54F is.

Introduced in 1983, Section 54F of the Income Tax act, as sourced from the Income Tax website, allows us to save capital gains tax if we sell mutual funds to buy a house.

Insertion of new section 54F. 12. In the Income-tax Act, after section 54E, the following section shall be inserted with effect from the 1st day of April, 1983, namely: -

'54F. Capital gain on transfer of certain. capital assets not to be charged in case of investment in residential house.

The basic premise of this tax exemption is very simple:

you wish to buy a house in India as an individual or HUF

you sell Mutual funds, shares, gold etc, to buy the house

on the date of the MF sale, you do not already own more than one house

you don’t have to pay capital gains taxes (only if it is long term gains) on the MF/shares/gold you sold

There is an upper limit of Rs. 10 crores on the exemption amount under Section 54F as per Budget 2023.

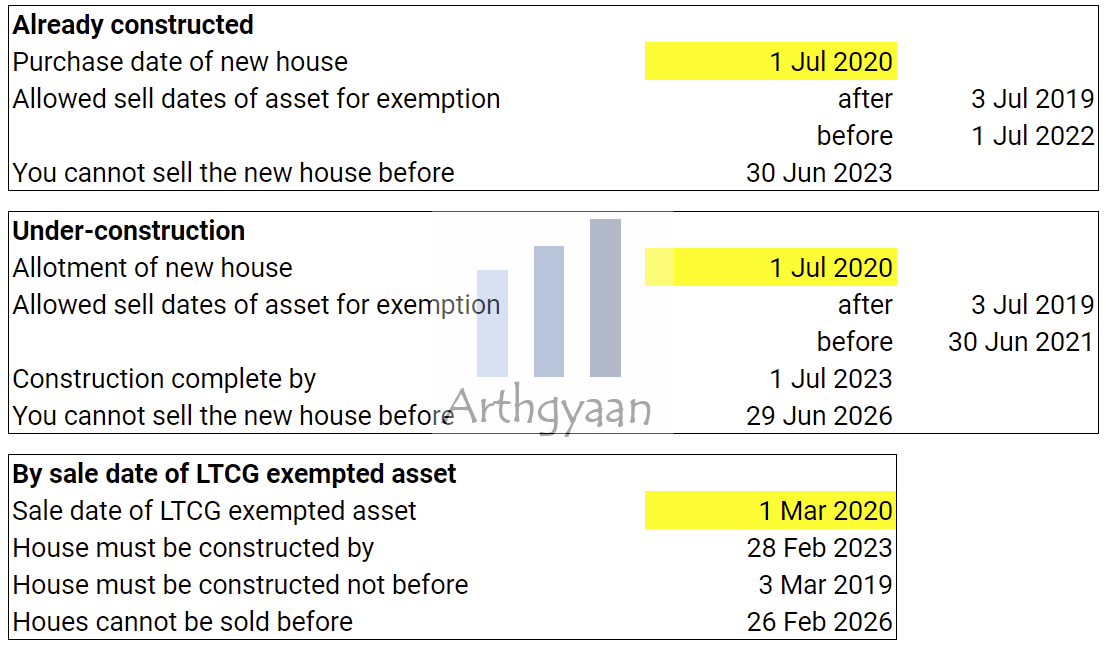

The key rules for applying Section 54F to an under-construction house

Every calculation is based on the agreement date. Depending on the state, this is also called allotment date or builder-buyer-agreement date

Rule 1: your share/MF sale that gets 54F advantage has to happen within one year before and one year after the agreement date

Rule 2: the house has to be constructed within 3 years of the agreement date which is measured by the registration date

Rule 3: you cannot sell the new house before 3 years of the registration date

Rule 4: the new house is your first or second house and not your third, fourth etc

Rule 5: everything like shares, mutual funds, RSUs, gold etc is eligible for selling . Only real-estate is not eligible

Violation of any of the rules above will invalidate Section 54F exemption.

For more nuances, please refer to the FAQ article linked above.

We have an easy-to-use calculator for Section 54F exemption calculation

Section 54F Tax Exemption Calculator

How to use the Section 54F Exemption Calculator?

The calculator requires you to enter three numbers, one choice of house type, the number of houses you own today and one date:

Cost of the New House you are planning to purchase

Sale Proceeds of Original Asset, eligible for long-term capital gains, which can be Mutual Funds, Shares, Gold etc. (anything except another property)

Long-term Capital Gains from this sale

The number of houses you own today since you cannot get Section 54F exemption if you own more than one house already

The type of you house you are purchasing: ready-to-move or under-construction

Now you need to enter one of these dates:

purchase date of house in case you know this date either in the past or future

sale date of LTCG exempted asset if you have already sold or plan to sell

Now click the Calculate Exemption button to get the result.

₹

1.00 Cr

₹

50.00 Lakh

₹

30.00 Lakh

A. By purchase date of house

B. By sale date of LTCG exempted asset

If you want to use a Google Sheets / Excel version, please see below:

We will use Google sheets to create a simple calculator for this calculation. There is a link to download a pre-filled copy of the Google sheet via the button below.

Important: You must be logged into your Google Account on a laptop/desktop (and not on a phone) to access the sheet.

Here are some case studies using the tool (click the image below)

Please refer to the Sec54F tab of the sheet once you open it. You can export this Sheet to Excel using the File > Download Menu option.

How does selling land and then purchasing an under-construction property fit into Section 54F in this case?

Conditions

Match?

Why?

The individual or HUF, and even NRIs, should be buying a house in India

Yes

Under-construction property (assumed in India)

The capital gain should arise from the sale of a long-term capital asset and cannot be a residential house

Maybe

Should be sold at least two years after purchase

The asset sold may also be a plot, land, commercial real estate or a house on rent which is not self-occupied

Yes

Residential Land is sold

The construction of the new house should be completed within three years of the sale

Maybe

Possession date is 2030, i.e. 5 years late (violates the 3-year rule)

The individual should not own more than one residential house on the date of the transfer of the original asset

Maybe

Information not provided

Note Section 54F application is on the sale proceeds of the land and not on capital gains. If you sold land for ₹1 crore, of which LTCG was ₹40 lakhs, then:

₹40 lakhs is tax-free only if the entire ₹1 crore is used for the new house

Only ₹20 lakhs is tax-free only if half of the entire ₹1 crore is used for the new house, and so on proportionately

Does this mean that the Section 54F exemption is valid in this case?

We will now examine a few additional nuances next.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Start Building Wealth with Expertly Curated Mutual Fund Packages

What Additional Conditions Must be True for the Section 54F exemption to be Applicable?

What Happens if Construction is Delayed?

Section 54F applicability is conditional on the construction being completed within three years of the land sale date, i.e. by 2028.

However, the target completion date is 2030 here.

Precedents in the case of construction delays have sided in the favour of the Section 54F claimant if the delay in construction is entirely the builder’s fault.

That being said, documentation must be available that the builder “intends to complete” the construction within the August 2028 deadline. The builder-buyer-agreement (BBA), RERA documentation, etc., must clearly mention 2028. Otherwise, the case becomes weak for the Section 54F application.

Another possible avenue that should also be explored is whether the entire sale proceeds from the land sale must be paid off to the builder within the three-year window. This is where the Capital Gains Accounts Scheme (CGAS) comes in.

What about the Role of CGAS for getting the Section 54F benefit?

The tax rules require you to open a Capital Gains Account Scheme (CGAS) account before July 2026 and deposit any unutilised portion of the land sale proceeds in that. Future payments to the builder must be made from the CGAS. The timelines for CGAS usage are based on the land sale date:

Land Sale date is before 31st Mar 2025: CGAS must be opened before 31 Jul 2025 (return filing deadline of AY 2025-2026), and any amount not paid to the builder must be deposited here.

Land Sale date is between 1st Apr 2025 and 31st Mar 2026: CGAS must be opened before 31 Jul 2026 (return filing deadline of AY 2026-27), and any amount not paid to the builder must be deposited here.

What is the Compliance Timeline to be followed here to get the Section 54F exemption?

We will assume that the land was sold after 31st March 2025. Otherwise, the years below are to be shifted back by one.

Year 2025

Land sale year: ensure that the gain is LTCG (>2 years holding period)

Get allotment letter from builder (August 2025). Sign the BBA showing intent to complete by 2028 (or at least having a payment schedule that utilises the entire land sale proceeds by 2028)

Important documents: Registered Sale Deed**, LTCG computation for land sale, Allotment Letter / BBA, RERA status of project, proof of payments to builder via bank statements

Year 2026

Open CGAS before July 2026 if all payments from the land sale have not already been made to the builder. Deposit any excess in CGAS

Future payments from the builder to come from CGAS first until used up (maintain CGAS-related documentation: passbook, etc.)

File Income Tax return (ITR) for FY 2025-26 before 31st July, showing both the land sale and claiming the Section 54F exemption

Important documents: proof of payments to the builder via bank statements, ITR, and CGAS-related documentation

Year 2027

Keep making payments to the builder as per the payment plan

Ensure that almost all of the land sale proceeds get paid this year as much as possible

Important documents: proof of payments to the builder via bank statements and CGAS-related documentation showing drawdown of the land-sale proceeds balance

Year 2028 (3-year window ends here)

Ensure that all payments from the sale proceeds are completed to the builder before 31st Mar 2028

If construction is incomplete, maintain proof of builder delay (letters, RERA filings, circulars)

Important documents: proof of payments to the builder via bank statements and CGAS-related documentation showing land-sale proceeds are now fully paid to the builder

Year 2029 and beyond

Keep correspondence showing builder delays beyond your control (e.g. construction updates that show the shifting date)

Save RERA extension orders, notices from the builder regarding delays, etc.

Important documents: proof of ongoing payments to the builder via bank statements, builder communication and demand letters, delay notices, RERA extension-related documentation

Note: The onus is on you to prove that the delay is beyond your control.

On Possession in 2030 or beyond

Take the possession letter from the Builder

Execute and register the Sale Deed/Conveyance Deed for the flat

Keep utility bills and property tax records as proof of ownership, along with the registered deed

Important documents: Proof of completion date (possession letter), Sale Deed

If you face income-tax scrutiny on this topic, this documentation will be required to defend the Section 54F claim.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Section 54F Capital Gains Exemption after Land Sale: Claiming on Delayed Under-Construction Property first appeared on 17 Sep 2025 at https://arthgyaan.com