How to invest a lump sum amount for your goals?

This article uses the Arthgyaan Have vs Needs Framework to invest a large lump sum amount in your portfolio per your financial goals.

This article uses the Arthgyaan Have vs Needs Framework to invest a large lump sum amount in your portfolio per your financial goals.

A lump sum is a large chunk of money, relative to the size of your portfolio, that you need to invest.

Typical examples of lump sum amounts come from bonuses, real estate sales or other such transactions. In addition, suppose you are doing a portfolio rebalancing exercise or exiting investments that no longer meets your objectives. In those cases as well, you will also end up with a lump sum cash amount.

We will use the bucket theory of portfolio creation, also called the Arthgyaan Have-vs-need (HvN) framework for investing a lump sum amount.

We extend the concept of the bucket theory of portfolio construction to create a framework to be used in the accumulation, i.e. the pre-retirement stage when the investor has active income and is investing for future goals.

The Arthgyaan Have vs Needs framework (HvN) is a simple tool to tell you how much money you need to invest:

We will now break this down in simple terms. There are two important questions that investors who are investing for their goals ask:

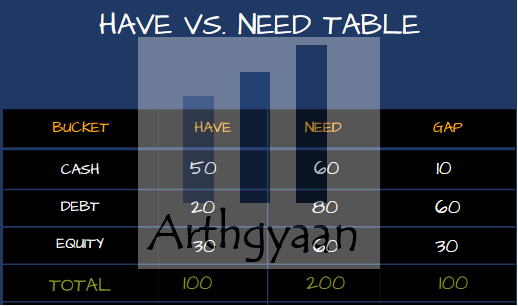

The Arthgyaan HvN framework needs you to make a very 4x4 simple table with three asset class buckets and for each bucket asks you to calculate three numbers: the amount you already have (the HAVE column), the amount you need to reach your goals (the NEED column) and the difference between the two (the GAP column).

The three buckets are:

The columns are:

We also have a TOTALs row to give a high-level view of the portfolio.

We create a set of rules for allocating a lump sum using the HvN framework like this:

We will see Steps 3-6 in action using a worked-out example.

To understand how to create such a plan for yourself:

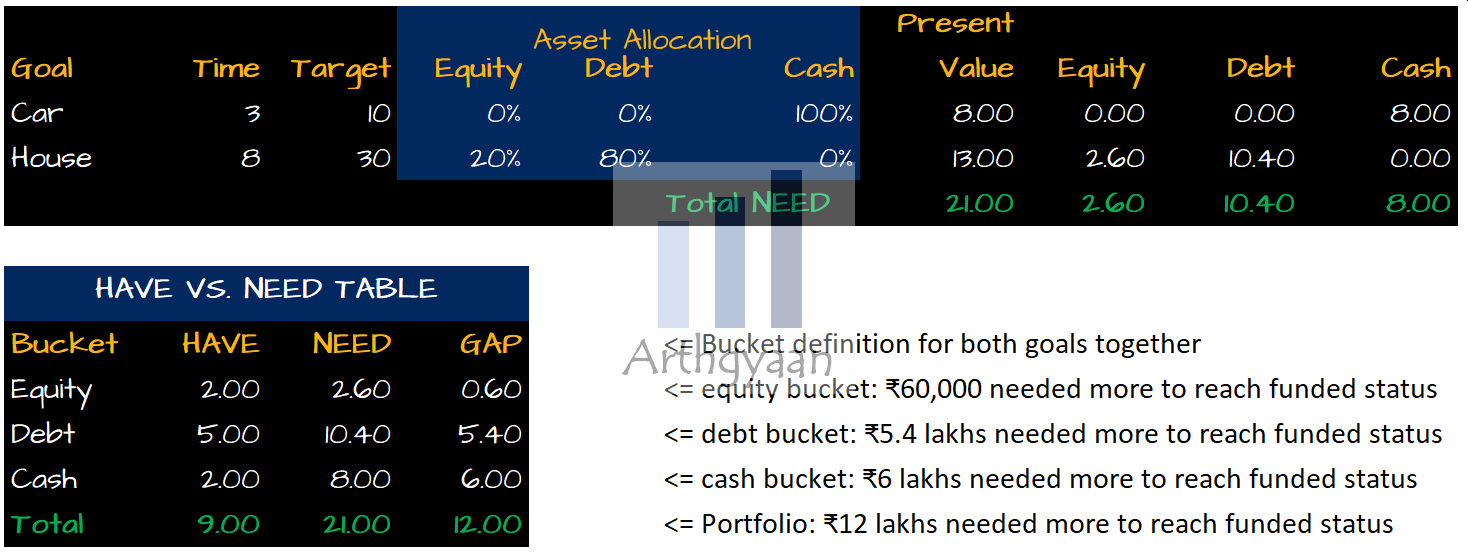

We will use a simple numerical example to calculate this. Let us say that the investor has two goals:

As the table shows, the investor has ₹2 lakhs, ₹5 lakhs and ₹2 lakhs in equity, debt and cash, respectively. The table also shows the total amount needed to reach the funded status of both goals combined. By funded status, we mean that for each goal, there is no need for further investment. This point is essential since the invested amount will grow over the time left to reach the goal value when the goal is due.

We assume that the investor is investing ₹20,000/month, which they will increase by 10% per year due to salary hikes. So the following year, they will be investing ₹22,000/month. Over the next 5 years, the amount invested becomes:

This ₹14.65 lakhs does not include any returns and is simply the total amount to be invested over the next five years.

We assume that the lump sum amount available is ₹5 lakhs from a bonus at work.

There is only one loan outstanding today, a ₹1 lakh education loan, that is paid off. So ₹4 lakhs is now left.

We see that in three years, there would be ₹7.94 lakhs invested from monthly salary. This money will be enough to fund the car goal. Hence we will not allocate any of the ₹4 lakhs to the cash bucket since the need figure (₹6 lakhs) for this bucket is lower than the amount that can be invested from salary.

There is a ₹0.6 lakhs or ₹60,000 gap in the equity bucket. Login to your mutual fund portal and invest this amount as a one-time investment or an equal amount over the next three months into equity funds. If you have investments in direct stocks, you can buy more of those.

Any remaining amount from the amount should now go into debt funds.

So in our example, the final allocation for ₹5 lakhs lump sum will be:

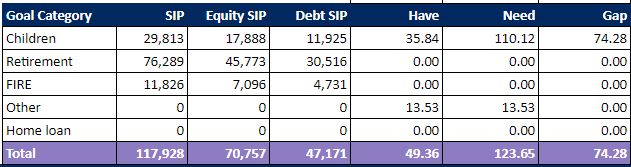

If you are using the Arthgyaan goal-based investing calculator, then it is effortless to calculate the numbers and use this framework for all your goals together as below:

Asset-wise view:

Goal-wise view:

Published: 23 December 2025

6 MIN READ

Published: 18 December 2025

8 MIN READ

1. Email me with any questions.

2. Use our goal-based investing template to prepare a financial plan for yourself.Don't forget to share this article on WhatsApp or Twitter or post this to Facebook.

Discuss this post with us via Facebook or get regular bite-sized updates on Twitter.

More posts...Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled How to invest a lump sum amount for your goals? first appeared on 27 Nov 2022 at https://arthgyaan.com