This article describes how to use the Arthgyaan goal-based investing tool as a calculator to determine if switching to the New Tax Regime makes sense from 1st April 2024.

This article describes how to use the Arthgyaan goal-based investing tool as a calculator to determine if switching to the New Tax Regime makes sense from 1st April 2024.

This article is a part of our detailed article series on Union Budget 2024. Ensure you have read the other parts here:

This article shows you the method for lowering the effect of Tax Collected at Source (TCS) on foreign remittances and travel via RBI’s Liberalised Remittance Scheme (LRS) as per new rules introduced under Union Budget 2024.

This article explains the new of the reversal of the 12.5% without indexation tax rule to allow 20% with indexation for all properties bought before 23rd July 2024.

This article helps you calculate the minimum price above which you must sell your property to pay lower taxes under the taxation rule change as per Budget 2024.

This article shows you how debt, international and gold/silver mutual funds will get taxed as per the new capital gains tax declared in the Union Budget 2024.

What did Union Budget 2024 say about personal income tax?

As per the Union Budget after the 2024 General Elections, the Finance Minister tweaked the New Tax Regime slabs slightly and kept the Old Tax Regime intact. We maintain that the new tax regime, which you can check using our easy-to-use calculator, is the better tax regime for most people.

What is the new tax regime as applicable due to Union Budget 2024?

Budget 2020 introduced the New Tax Regime (NTR) with the premise of lower overall taxes on income as long as tax deductions like 80C, 80D, HRA, etc., are foregone by the investor. In contrast, the Old Tax Regime (OTR) allows all of these deductions but with a higher tax on the post-deduction income. As per Union Budget 2023 (as announced on 23-Jul-2024),

Old tax Regime slabs for post-deduction income are:

0-2.5L - no tax

2.5-5L @ 5%

5-10L @ 20%

10L+ @ 30%

New tax Regime slabs for post-deduction income are:

0-4L - no tax

4-8L @ 5%

8-12L @ 10%

12-16L @ 15%

16-20L @ 20%

20-24L @ 25%

24L+ @ 30%

Note: The new tax regime slabs are as of Union Budget 2025 announced on 1-Feb-2025. Standard deduction is at ₹75,000 (same as Budget 2024) for income from salary and pension. Please keep in mind that offset of capital gains say under Section 111A, 112 etc (stocks and mutual funds) will not be available in the amounts above the threshold 4L no-tax threshold.

This means that income up to ₹12.75L (including the standard deduction) will be tax-free but if you have say ₹3 lakhs of equity long-term capital gains, it will still be taxable at 12.5% above 1.25L. Though taxable income starts after 4 lakhs as per the slabs, there is no tax until ₹12.75lakhs (₹12 lakhs for non-salaried) due to marginal relief.

There is also a concept of marginal relief, under Section 87A, up to ₹71,250 so that some one with ₹12,75,001 income is not hit with ₹71,250 tax just because of being over the threshold by ₹1. In Budget 2025, 87A relief has been raised to ₹60,000 for income up to ₹12 lakhs. 87A rebate is not available for NRIs.

Previous to Union Budget 2025, the new regime slab rates were:

0-3L no tax, 3-7L @ 5%, 7-10L @ 10%, 10-12L @ 15%, 12-15L @ 20%, 15L+ @ 30% with ₹75,000 standard deduction as per Budget 2024 (applicable to FY 2024-25)

0-3L @ 0%, 3-6L @ 5%, 6-9L @ 10%, 9-12L @ 15%, and 15L+ @ 30% with ₹50,000 standard deduction as per Budget 2023 (applicable to FY 2023-24)

In the Union Budget 2024 speech, the new tax regime slabs were tweaked to give an additional ₹17,500 tax reduction. Here is a worked-out example for an income of ₹20 lakhs demonstrating the ₹17,500 benefit.

Tax Rate

Before Budget 2024

Tax

After Budget 2024

Tax

Benefit

0%

0-3L

0

0-3L

0

0

5%

3-6L

15,000

3-7L

20,000

-5,000

10%

6-9L

30,000

7-10L

30,000

0

15%

9-12L

45,000

10-12L

30,000

15,000

20%

12-15L

60,000

12-15L

60,000

0

30%

Above 15L

1,50,000

Above 15L

1,50,000

0

0%

Std. deduction 50k

-15,000

Std. deduction 75k

-25,000

7,500

Benefit

-

-

-

-

17,500

Given how these slabs are structured, there is a break-even point based on the total amount of deductions you usually take so that one of the tax regimes leads to lower taxes. Now that NTR is the default option, it is essential to choose the tax regime correctly, as many companies will open up the choice in April.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Switching regimes and default options

An individual salaried taxpayer can switch between the old and new tax regimes once a year without restrictions. If you have yet to specify the regime to your employer, then the new tax regime will be used by default. You must also file your ITR on time if you wish to use the old tax regime.

Taxpayers can also declare one tax regime (old or new) to their employer and then switch to the other one when filing.

This article helps you decide, based on your tax planning and the deductions you wish to take, which regime will be beneficial for you for financial year FY2024-25, which starts on 1st April 2024. However, you should remember that if you declare the wrong tax regime and later add/remove deductions, more tax will get deducted. Therefore, you will have to ask for a refund when filing.

Which tax regime is better if you want to invest in NPS as per Union Budget 2024?

Union Budget 2024 added a new incentive for taxpayers to switch to the New Tax Regime by increasing the deduction available under non-government employer contributions to the NPS. It raised the eligibility amount from 10% to 14% of basic pay plus dearness allowance (DA).

Taxpayers without income from business or profession

As per Budget 2023/interim Budget 2024 and of course Union Budget 2024, the new tax regime is the default unless the taxpayer chooses the old regime.

You can switch between old and new and back anytime during tax-filing by 31st July. If you miss the 31st July deadline, you cannot switch regimes and have to choose the new regime.

Taxpayers with income from business or profession

These tax filers who must use ITR 4, have to fill Form 10-IEA to choose the old tax regime before 31st July. Otherwise, the new regime will apply.

If you have income from business or profession, you cannot switch regimes every year.

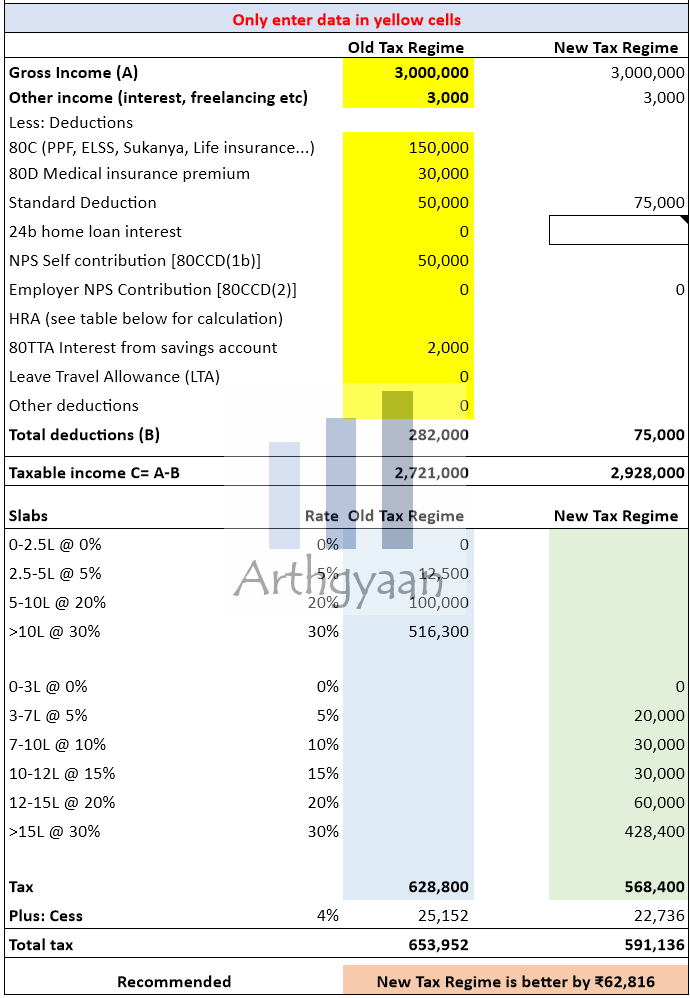

Using the calculator

We will use Google sheets to create a simple calculator for this calculation. There is a link to download a pre-filled copy of the Google sheet via the button below.

Important: You must be logged into your Google Account on a laptop/desktop (and not on a phone) to access the sheet.

Here are some case studies using the tool (click the image below)

We show a few cases below.

Start Building Wealth with Expertly Curated Mutual Fund Packages

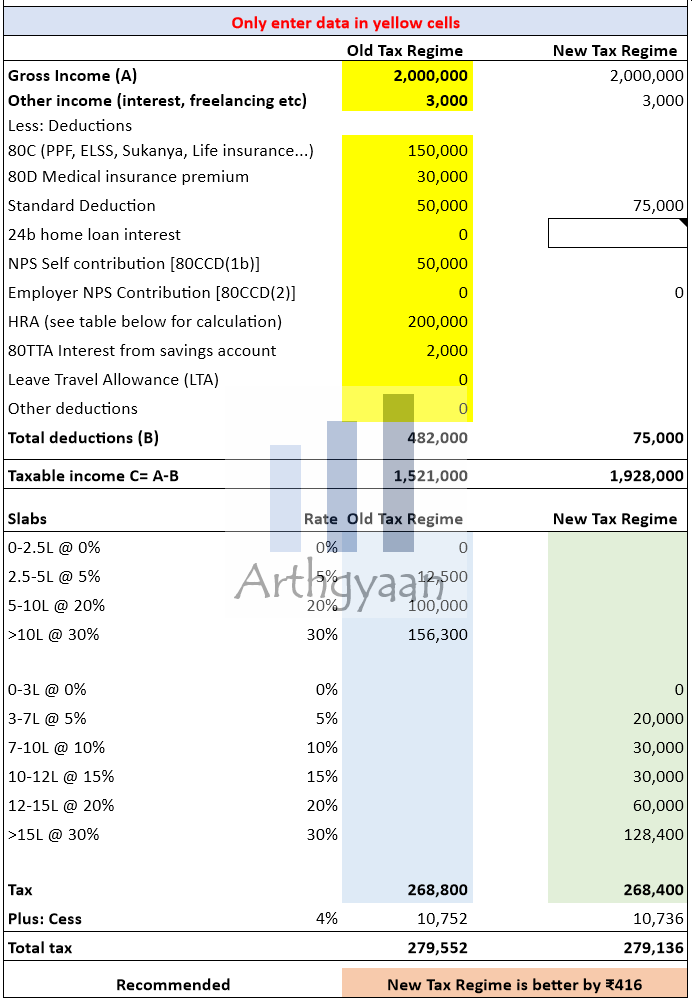

Case 2: Income 20 lakhs, usual deductions but no HRA

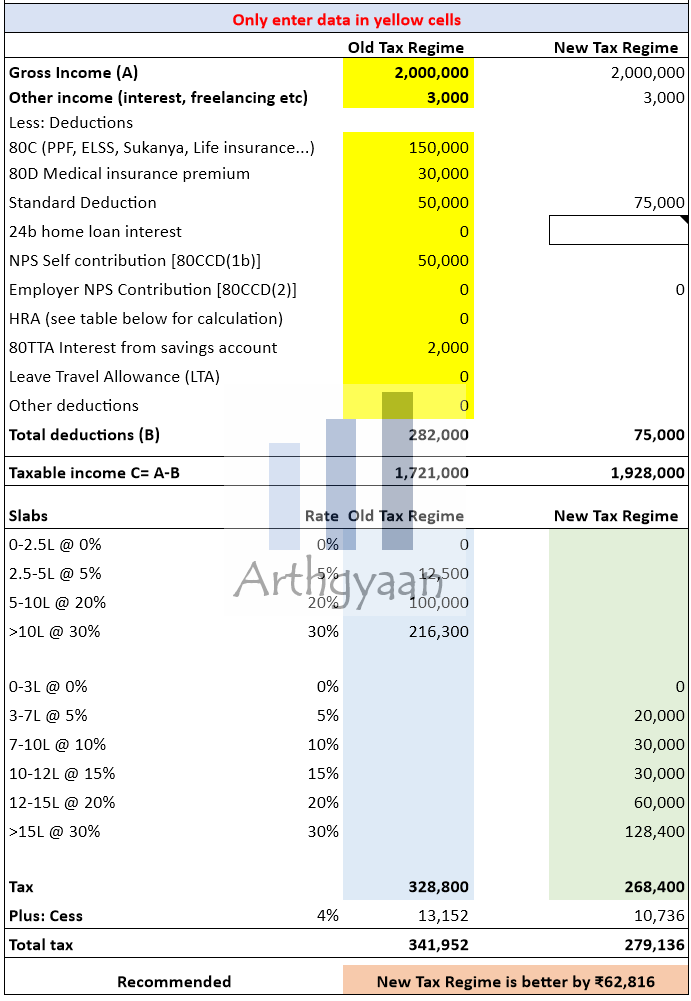

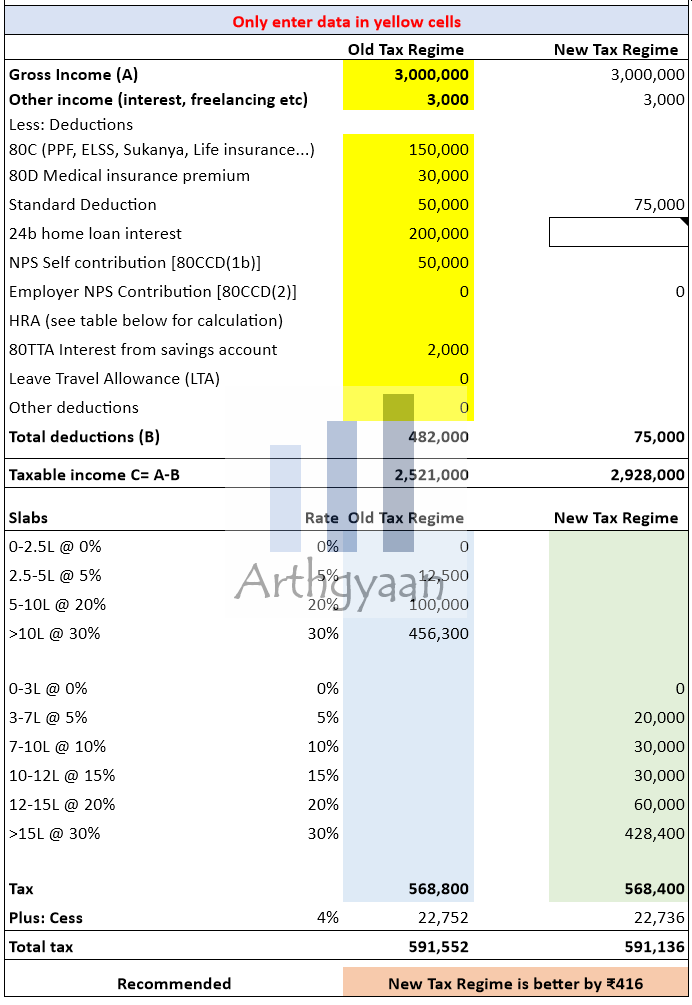

Case 3: Income 30 lakhs, usual deductions, home loan

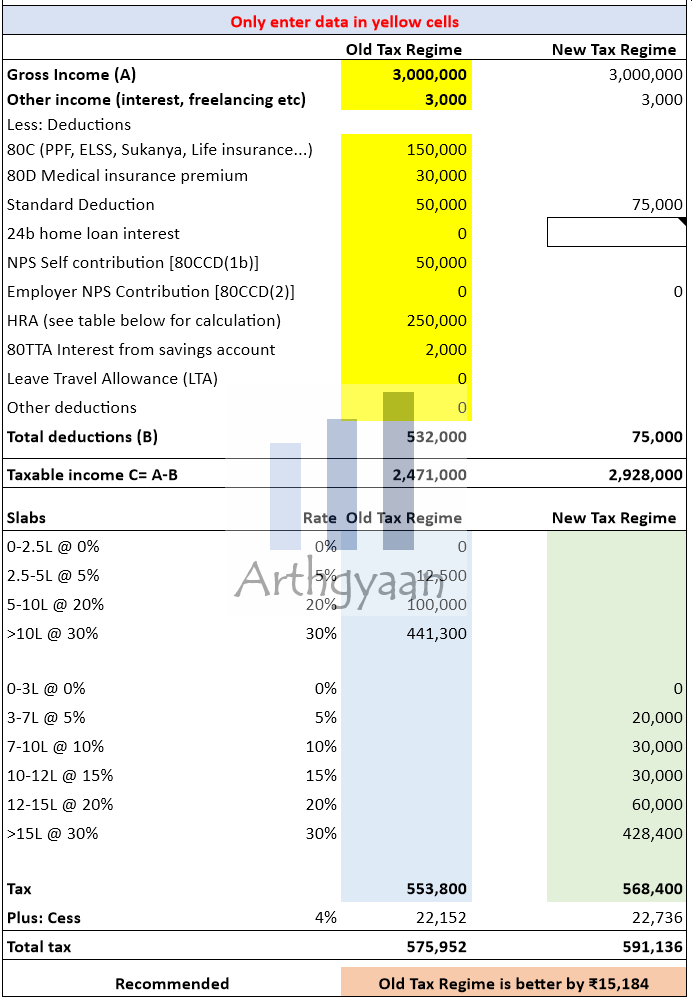

Case 4: Income 30 lakhs, usual deductions, HRA

Case 5: Income 30 lakhs, usual deductions, no HRA, no home loan

Summing up

As in all the cases above, the differentiating factor is the quantum of deductions. As long as the amount of deductions from 80C, 80D, home loan, HRA, etc., exceeds ₹3.75 lakhs, the old tax regime is better. Two key differences between the regimes are now the higher (75,000 instead of 50,000) standard deduction and the difference in how corporate NPS is handled.

The old tax regime, therefore, makes sense only if you have substantial valid investments via 80C, pay a good amount of medical insurance premium under 80D and have either a home loan or receive HRA.

The new tax regime makes sense

if you have a high enough income so that 80C is taken care of by default by EPF but do not have a home loan or no HRA since this could be very close or less to 10% of your basic pay

if you stay in your own home without a home loan and do not have to pay rent or EMI

if you have planned your investments as per goal-based investing and do not have an excess allocation to debt investments like PPF or insurance plans

If you are still determining your deductions, you can play around with your options in the calculator to see what works best for you.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Union Budget 2024: which is the best tax regime to choose from 1st April 2024? (July 2024 update) first appeared on 23 Jul 2024 at https://arthgyaan.com