If you’re worried about job security - whether at Amazon or elsewhere - now is the time to prepare. This guide helps you safeguard your finances, manage loans, and build a backup plan.

If you’re worried about job security - whether at Amazon or elsewhere - now is the time to prepare. This guide helps you safeguard your finances, manage loans, and build a backup plan.

Amazon is reportedly considering cutting up to 14,000 managerial positions in early 2025. While the rationale of such a cut (“cost savings” and “efficiency improvements”) is debatable, it is good to be prepared if you suddenly find yourself in such a situation.

This article covers the situation where you are concerned that your role, whether at Amazon or not, is currently under threat and are looking for options.

Focus on upskilling and networking to improve your human capital

It is better to stop something bad from happening than it is to deal with it after it has happened.

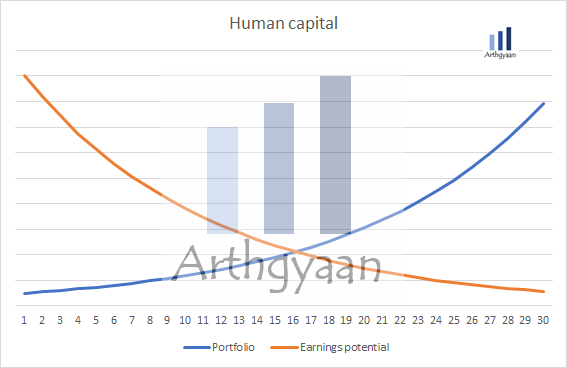

We have deliberately kept this point at the beginning since we believe that the impact of continuous improvements to your human capital is the largest both in growing your income and finding another job quickly.

Human capital is an estimate of the future earning potential of an investor, either from salary, profession or business. As age increases, human capital will reduce; however, the investments made by the investor create a portfolio i.e. financial capital that meets all financial goals. In the case of looming job losses, having the right connections will get a foot in the door (i.e. an interview call) while new and improved skills will help you sail through the interview. Of course, newer skills will help you create additional dependencies in your current role as well and help you stay on longer.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

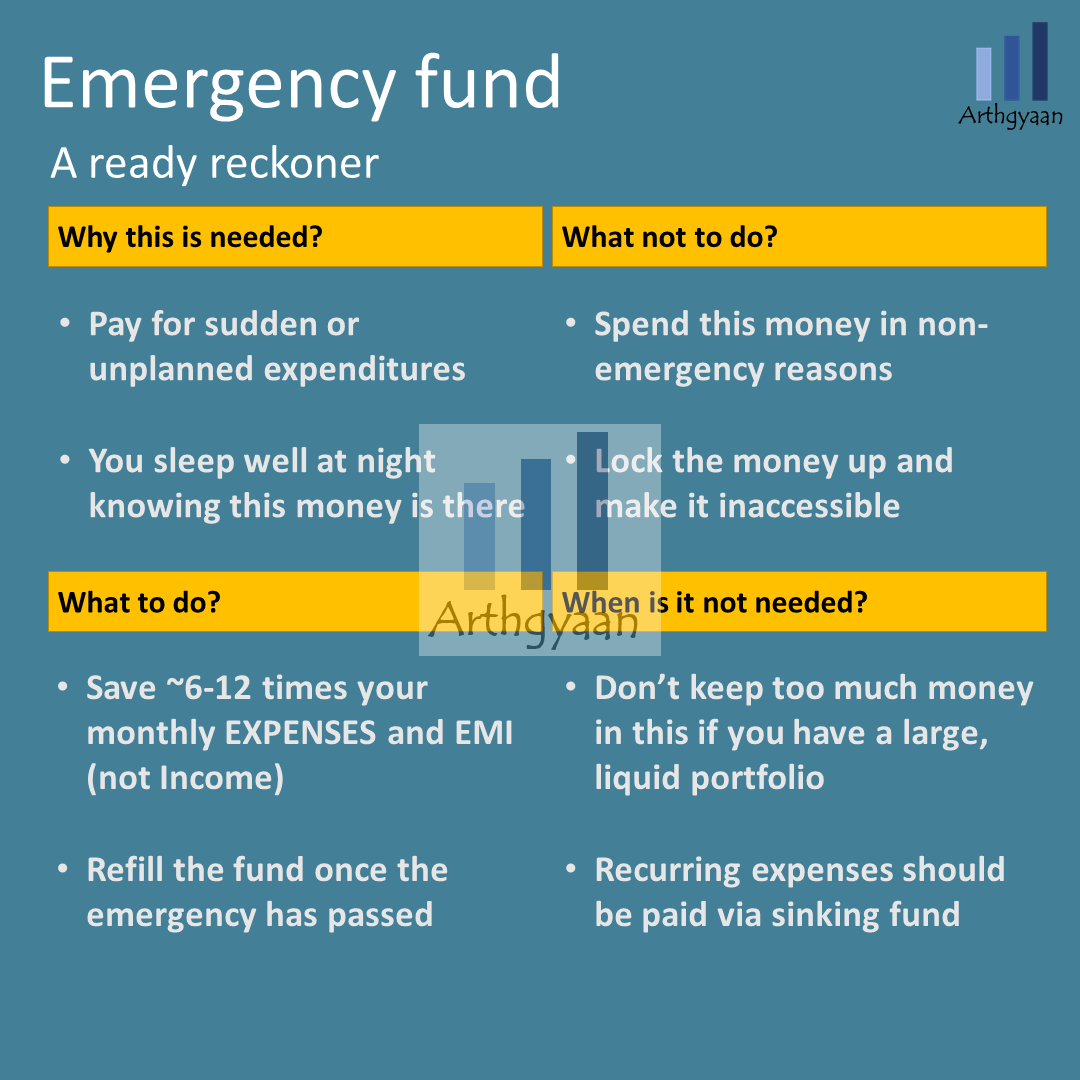

The role of the emergency fund in a job-loss scenario

Saving 6-12x monthly expenses as an emergency fund helps you sleep well at night.

An emergency fund is a stack of money kept aside for a sudden or unplanned expenditure or contingency. This money is needed to be available for immediate use in emergencies. Without this safety net in place, you will have to run around for money, depend on a loan or use a credit card at high interest rates.

In this case, the purpose of your emergency fund is to keep your mandatory expenses (rent/EMI, groceries, school fees etc) running along smoothly while you search for your new job.

Remember: Known recurring items like insurance premiums, building maintenance etc. are to be saved via a sinking fund: see this detailed post on sinking funds for details

Dealing with a home loan

A home loan is one of the biggest sources of fear that many of us have whenever we read about job losses. When you have a home loan, your risk-taking ability changes immediately. Two sources of risk affect you:

external factors: job loss, interest rates, inflation, capital market returns, appreciation in the housing market

internal factors: health, human capital, other goals like retirement

There are multiple strategies to deal with a home loan:

Pay lump sum amounts when bonuses come

Increase the EMI every year

Start with a higher EMI at the beginning

Each of these options has its pros and cons and if you are concerned about an impending job loss, you need to balance a wish to pay off the loan quickly vs. holding on to that capital for emergencies.

Start Building Wealth with Expertly Curated Mutual Fund Packages

Other loans like credit cards and BNPL or Low/No-cost EMIs

High-interest loans like credit cards and personal loans are always the first target for elimination if your job is stable or not. If you have a credit card loan, pay it off today from any liquid assets like shares, mutual funds or even by taking a personal loan: What are the best ways to pay off a large credit card balance quickly?

Personal loans and car loans (including car leases) are less onerous compared to credit cards just like a wolf’s bite is less deadly than a crocodile’s jaws - both can hurt, but one drags you into deeper trouble much faster. If you have either and a job loss is imminent, sell assets or borrow from family (or even a top-up home loan) to pay those off.

Being able to pay EMI doesn’t mean you can afford it.

BNPL or low/no-cost EMIs exemplify this statement. If you have such loans going on, explore paying them off for peace of mind.

Children’s goals like college admission

If you have a mandatory expense due in the next few years, like a college fee payment, or are already in the middle of a series of college-related expenses, then the potential of a job loss can be disruptive.

If you are already paying college fees, then those should be handled via the emergency fund. If the goal is due in a few years, one way to be sure that the goal is not disrupted is by using Arthgyaan packages targeting college admission. The pre-packaged mutual fund bundles adapt to both the market and the investor’s situation to minimise the impact on the target goal amount.

Choose the year closest to your desired college admission year to get started:

The direct impact on retirement

The impact on retirement due to a job loss is the biggest. A few months’ break in investing in case it takes longer to find a job is not consequential in the bigger scheme of things. The impact will be even less in dual-income families.

However, a permanent reduction in income due to not getting an equivalent profile, either due to the impact of AI, age-ism, recession or a similar factor will be the main problem here.

Retirement is the only goal that you will not get a loan for

There are a few ways to mitigate this risk ranging from reprioritising goals. For example, college education expenses can be funded by an educational loan or a large house can be sold to pay off the home loan and shift to a cheaper house.

You can use the Arthgyaan goal-based investing calculator to check the impact on your retirement goals by changing the SIP amounts and target retirement corpus values.

You can look at Arthgyaan Packages for making your retirement planning simpler. Each Arthgyaan Package is a structured investment plan for retirement, ensuring financial security in later years through systematic wealth accumulation tagged to a particular retirement year. A package encapsulates the portfolio creation assumptions (equity / debt / cash asset returns, inflation, longevity and rebalancing plan) and creates a mutual fund (and EPF, PPF and NPS if applicable) portfolio.

Choose the year closest to your desired retirement year to get started:

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Amazon Layoffs 2025: How to Prepare and Protect Your Financial Plan first appeared on 19 Mar 2025 at https://arthgyaan.com