What should you do when your home loan interest rates go up?

This post discusses managing when interest rates go up increasing your home loan EMI.

This post discusses managing when interest rates go up increasing your home loan EMI.

This article is a part of our detailed article series on the concept of home loans. Ensure you have read the other parts here:

This article breaks down the benefits of prepaying your home loan and how it impacts both your interest payments and tax savings.

This article shows how quickly you can pay off your home loan, and even save a lot of interest, by increasing your EMI steadily year-on-year.

This article tells you why it is a good idea to buy a home jointly as a couple and it is not only the tax benefits you get.

This article shows you an easy way to calculate how big a house you can buy based on your family’s combined monthly salary.

Home loan rate hike? You can prepay to keep EMI and tenor same. This post shows how.

This article shows how paying a small fee to your bank to reduce your home loan rate can save you lakhs in interest over the life of your loan.

This article shows you the benefits due to interest saving when you make a part-payment to your home loan. Your loan duration also reduces due to the pre-payment.

This article shows a handy ready reckoner for home loan EMI amounts for all tenures and interest rates along with the amount of principal and interest to be paid.

This article helps you decide when to prepay your home loan - at the beginning, middle or end of the total loan period.

This articles describes overdraft home loans like SBI Maxgain and BOB Home Loan Advantage.

Home buyers should keep in mind that most home loan rates are floating i.e. the rate of interest will fluctuate over time. An increase in interest rates will increase the EMI and may cause a strain on the household budget or other investments for other goals.

This is an important consideration since currently, interest rates worldwide are going up due to higher inflation. In India, the marginal cost of funds-based lending rate (MCLR) is being raised, and loans (home/personal/car etc.) linked to MCLR are already going up. In addition, new home loans that are connected to the RBI repo rate (RLLR) are also at risk since RBI has been increasing the repo rate.

Chart: Arthgyaan • Source: RBI • Get the data

RBI, after hiking the Repo rate from 4.00% to 6.50% in quick succession, has finally started cutting the repo rate:

The hike from 2022 was a part of inflation-taming measures put in place by global central banks.

As inflation had been rising as the economy recovered, the repo rate rise was inevitable. As inflation is now cooling and Budget 2025 has seen tax rates to reduce, the repo rate has been cut for the first time since May 2020.

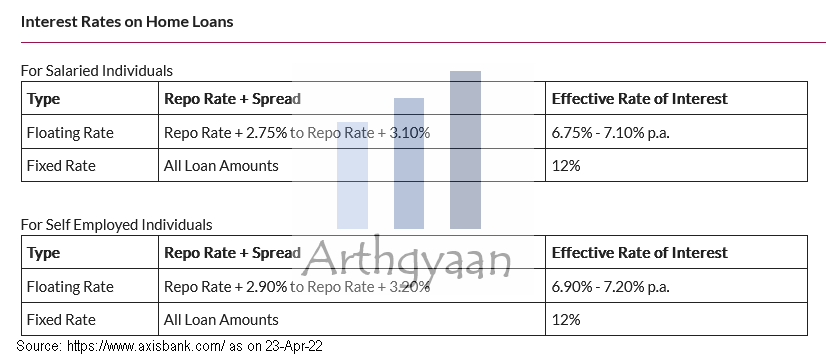

The interest rate on your home loan will typically be a floating rate that will fluctuate with overall interest rates in the economy. Usually, the RBI repo rate movements indicate the direction of interest rates in the economy. At the same time, home loans are tied to the Repo Linked Loan Rate (RLLR) or Marginal Cost of Funds-based Lending Rate (MCLR) as per RBI. As inflation increases, the central bank is expected to increase this year.

As interest rates fluctuate, so will your EMI over time. If rates increase, one of two things happen:

Any increase in the EMI will correspondingly cause an impact on your household budget, as we show below.

We break down the home loan rate into its major components to see where the fluctuations come from.

Repo linked home loan rate = Repo Rate + Spread + Premium

Repo rate: This rate is decided by the RBI. Home loan rates will move up and down as soon as the RBI revises the repo rate.

The latest repo rate is 5.25%. This rate was last reviewed by the RBI on 05 Dec 2025.

Spread: This is an additional rate on top of the repo rate that essentially captures the profit the bank can make off this loan relative to the deposits it offers to customers. This rate is generally revised every three years but will vary from bank to bank.

Premium: An extra value for some specific customers. For example, SBI adds another 15 bps for non-salaried customers or it will depend on the CIBIL score of the borrower. This value is also revised periodically, like every three years.

We will assume a home loan with a current rate of 9% and an outstanding balance of ₹50 lakhs. You can determine the impact on your loan by applying the unitary method. For example, if your due balance is one crore, you need to double the numbers in the table. The table shows the annual change in EMI due to both decreasing and increasing rates. The base case of no change in EMI is in the centre column of the table.

To explain the data, if the interest rate rises by 1% and 10 years is left for your ₹50 lakhs loan balance, then your annual EMI amount will increase by ₹29,125.

Please use the sliders below:

Fixed rate loans seem to be a good solution to this problem. If the rates never rise (or fall), then you no longer have to worry about this problem. The EMI will always be the same. Except when they are not:

If you are thinking to take a fixed rate loan, you will be better off with a floating rate loan and keep the difference in a EMI buffer fund as explained below.

You should perform an immediate portfolio review, including emergency fund review, as soon as the interest rate changes. To be on the safe side, use a slightly higher interest rate, say by extra 1%, when calculating the impact on goals and emergency fund amount when you are buying a house with a loan.

You can offset a part of the increase by reducing the principal via pre-payment. This plan assumes that your current asset allocation for goals allows this to be done. If you have excess equity allocation, then only you can rebalance from equity into the home loan prepayment.

Pre-payment amount that keeps the EMI constant can be calculated as:

Pre-pay = Outstanding_Balance * (1 - OldEMI/NewEMI)

A numeric example to explain this formula:

Read more on the topic of prepayment to ensure that it is the right thing to do in your case: Should you use your stock market profits to prepay a home loan?.

All lenders are not equally prompt in changing the rates as per the MCLR or repo rate changes, especially when rates are going down. However, when rates rise, they will probably be passed on to the borrower reasonably quickly since it is in the bank’s interest to do so.

If you find that other lenders are offering lower rates, consider transferring with the caveat that those rates may also rise soon. On the other hand, if you are getting a better rate elsewhere, consider switching costs and customer service of the new lender.

If you follow our goal-based investing plan for paying the home loan, you can adjust your home loan related goal for a higher interest rate. In addition, this plan will pull in an additional amount from other purposes to pay the loan. If your actual loan rate is lower than what you assumed it to be, invest the difference of the EMI in a debt mutual fund to be used when rates rise.

For example, for a 50L loan for 15 years,

You can invest the difference of ₹2,842 in a debt fund via SIP to be used when the rate rises. Please use the table in the “Change in EMI for increasing home loan rates” section above to check how much to save in the EMI buffer fund. The table shows yearly figures so divided that by 12 to get the monthly SIP amount.

If you cannot manage the EMI increase post the rate rise, please speak to the lender to increase the loan term.

Published: 23 December 2025

6 MIN READ

Published: 18 December 2025

8 MIN READ

1. Email me with any questions.

2. Use our goal-based investing template to prepare a financial plan for yourself.Don't forget to share this article on WhatsApp or Twitter or post this to Facebook.

Discuss this post with us via Facebook or get regular bite-sized updates on Twitter.

More posts...Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled What should you do when your home loan interest rates go up? first appeared on 24 Apr 2022 at https://arthgyaan.com

Copyright © 2021-2025 Arthgyaan.com. All rights reserved.