What benefit do you get if you make a one-time prepayment to your home loan?

This article shows you the benefits due to interest saving when you make a part-payment to your home loan. Your loan duration also reduces due to the pre-payment.

This article shows you the benefits due to interest saving when you make a part-payment to your home loan. Your loan duration also reduces due to the pre-payment.

This article is a part of our detailed article series on the concept of home loans. Ensure you have read the other parts here:

This article breaks down the benefits of prepaying your home loan and how it impacts both your interest payments and tax savings.

This article shows how quickly you can pay off your home loan, and even save a lot of interest, by increasing your EMI steadily year-on-year.

This article tells you why it is a good idea to buy a home jointly as a couple and it is not only the tax benefits you get.

This article shows you an easy way to calculate how big a house you can buy based on your family’s combined monthly salary.

Home loan rate hike? You can prepay to keep EMI and tenor same. This post shows how.

This article shows how paying a small fee to your bank to reduce your home loan rate can save you lakhs in interest over the life of your loan.

This article shows a handy ready reckoner for home loan EMI amounts for all tenures and interest rates along with the amount of principal and interest to be paid.

This article helps you decide when to prepay your home loan - at the beginning, middle or end of the total loan period.

This articles describes overdraft home loans like SBI Maxgain and BOB Home Loan Advantage.

This post discusses managing when interest rates go up increasing your home loan EMI.

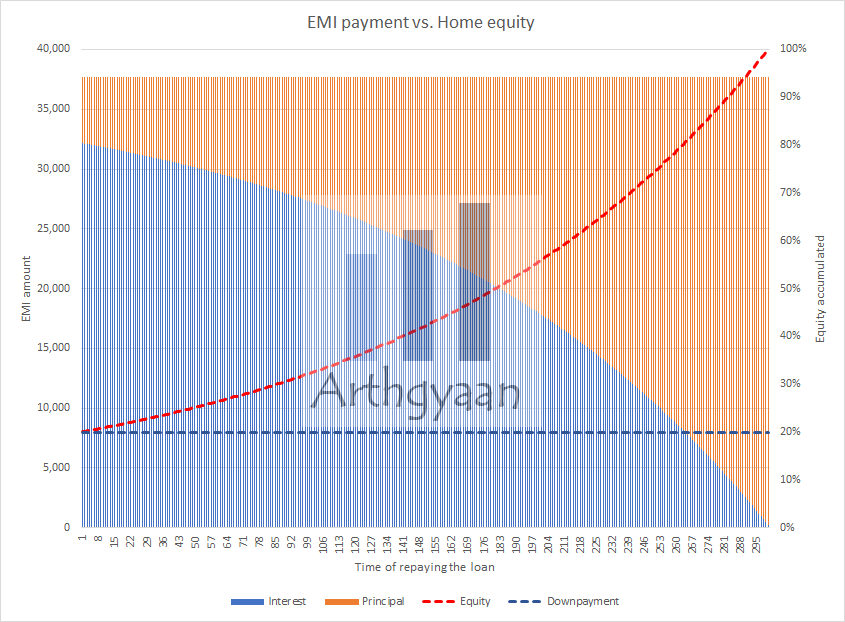

The bank gives a home loan to own the property while you use it until you pay back the loan via EMIs. An Equated Monthly Instalment plan (EMI) is a standard way to pay off a loan by making a fixed payment monthly that includes both interest and principal in the same amount.

EMI = Principal + Interest

In each EMI, the split of the interest and principal changes since the interest is based on the outstanding loan balance at that point and the rest of the EMI is principal. As the chart shows, the interest part drops off with time, and the rest is the principal. The actual numbers in the chart relate to a ₹50 lakhs home loan taken at 8% for 25 years. The EMI is ₹38,591. The down payment amount is ₹12.5 lakhs.

You can test the numbers using this calculator:

As you pay back the loan, your ownership share in the house will increase in the same way. At the point of taking the loan, you own 20% of the house (12.5 out of 62.5, of which 50 is the loan). The bank owns 80%. As the loan is repaid, you own more and more of the house as the principal is paid off. This is the concept of building equity in an asset. Equity is the part of the asset you own after subtracting the part that the bank owns.

Home equity value = Current home value - Outstanding loan balance

Once you build equity in your home, that has additional benefits:

We break down the home loan rate into its major components to see where the fluctuations come from.

Repo linked home loan rate = Repo Rate + Spread + Premium

Repo rate: This rate is decided by the RBI. Home loan rates will move up and down as soon as the RBI revises the repo rate.

The latest repo rate is 5.25%. This rate was last reviewed by the RBI on 05 Dec 2025.

Spread: This is an additional rate on top of the repo rate that essentially captures the profit the bank can make off this loan relative to the deposits it offers to customers. This rate is generally revised every three years but will vary from bank to bank.

Premium: An extra value for some specific customers. For example, SBI adds another 15 bps for non-salaried customers or it will depend on the CIBIL score of the borrower. This value is also revised periodically, like every three years.

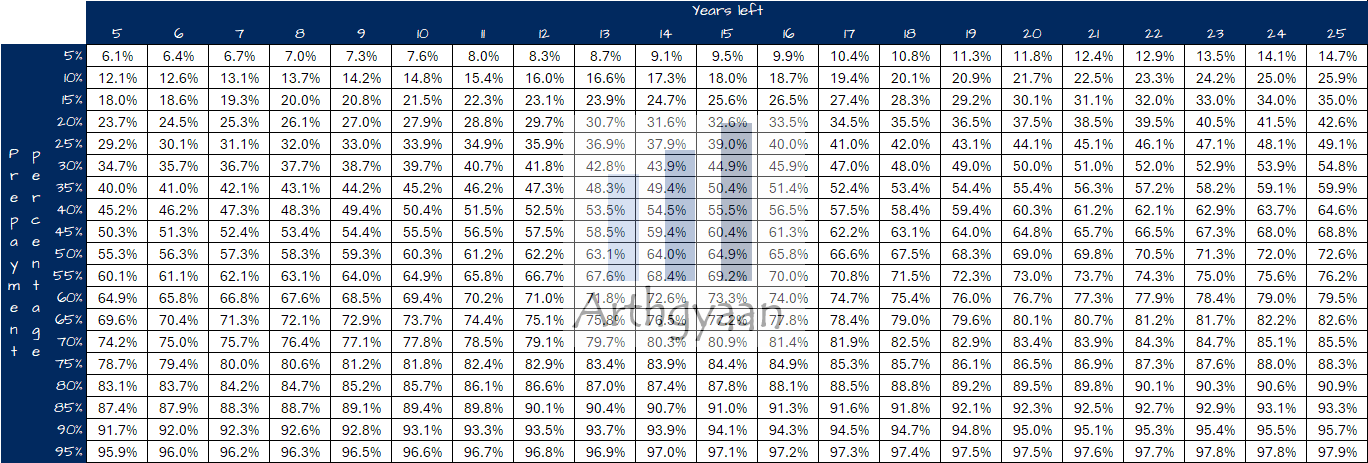

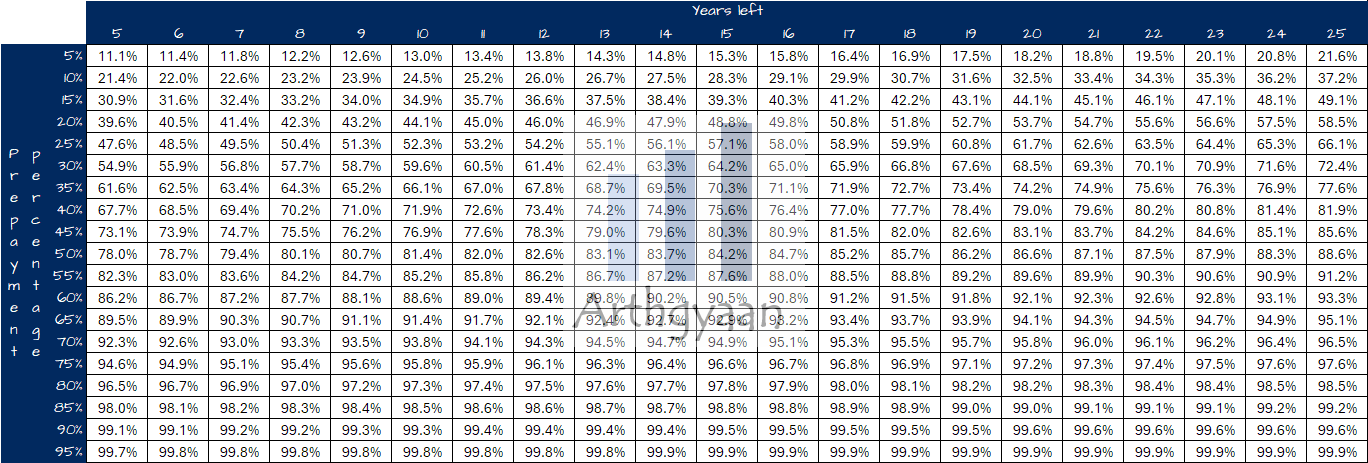

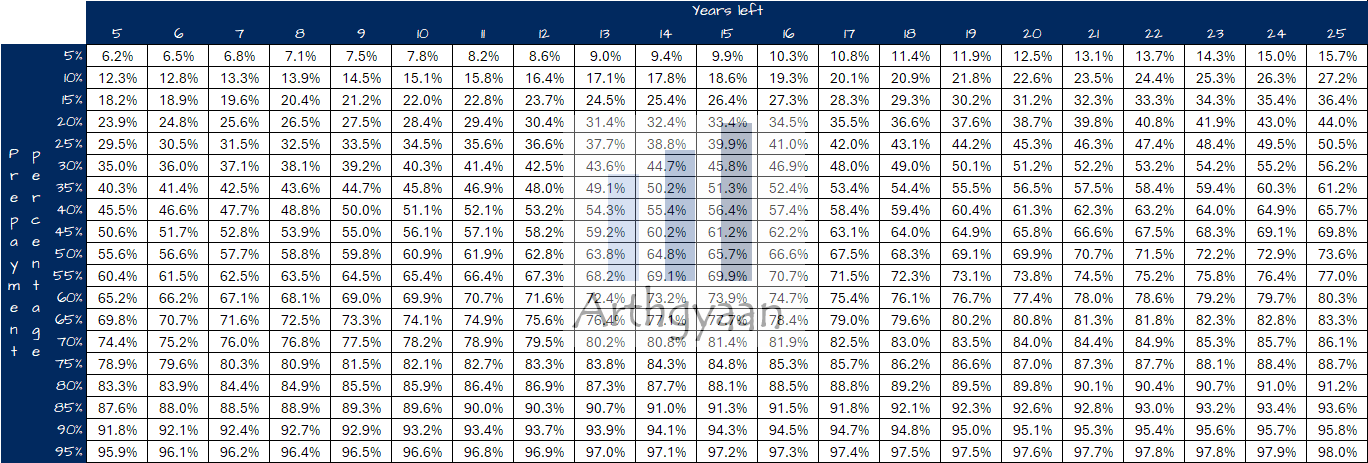

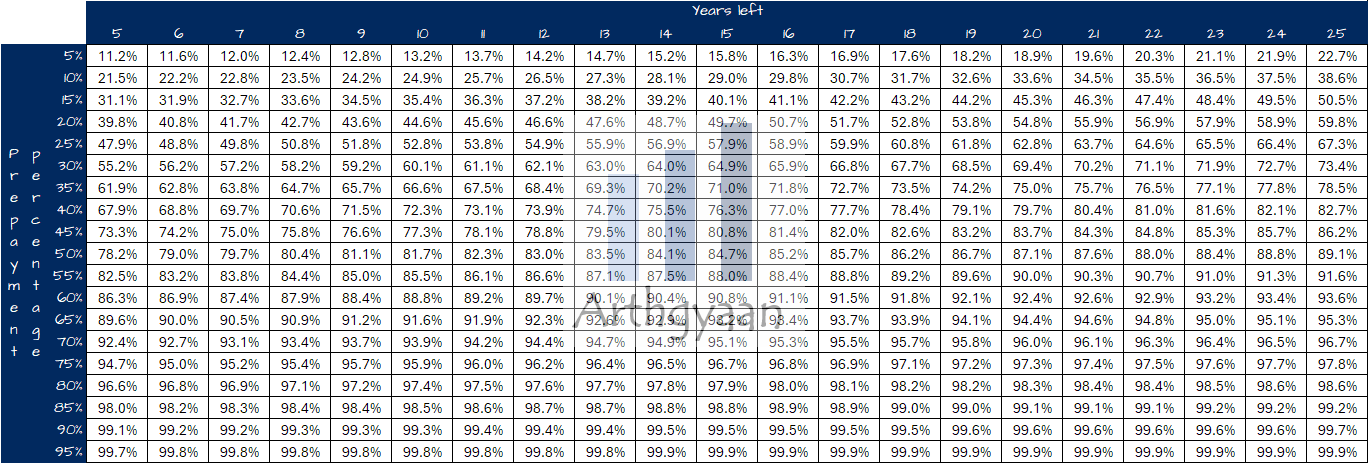

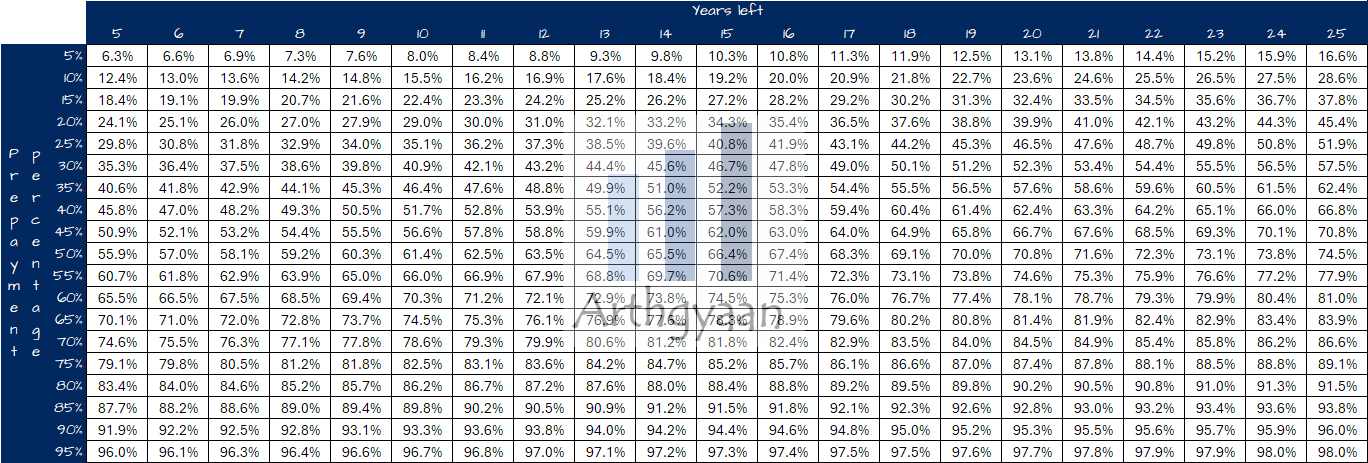

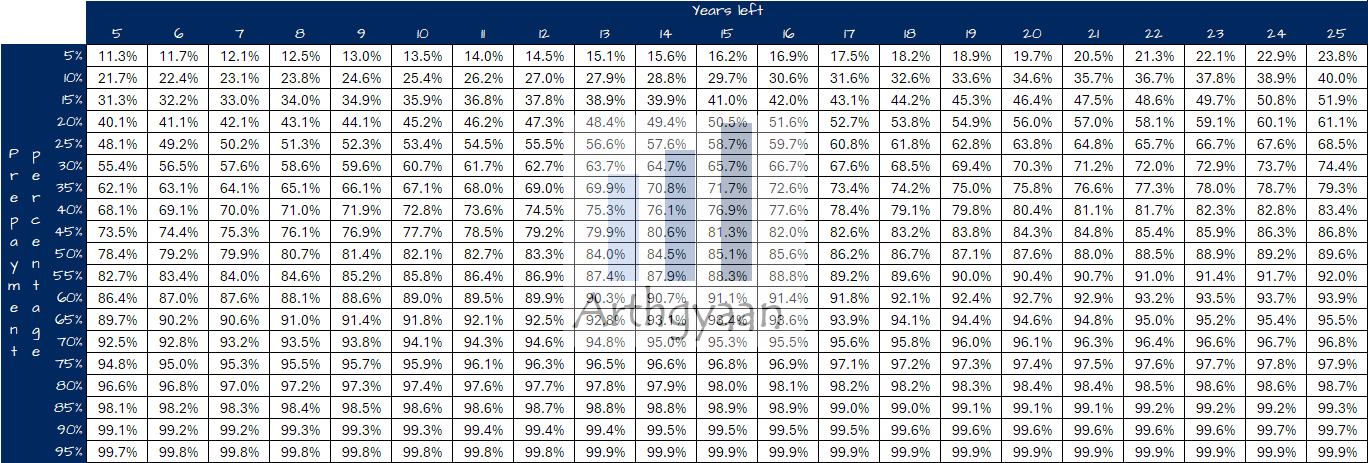

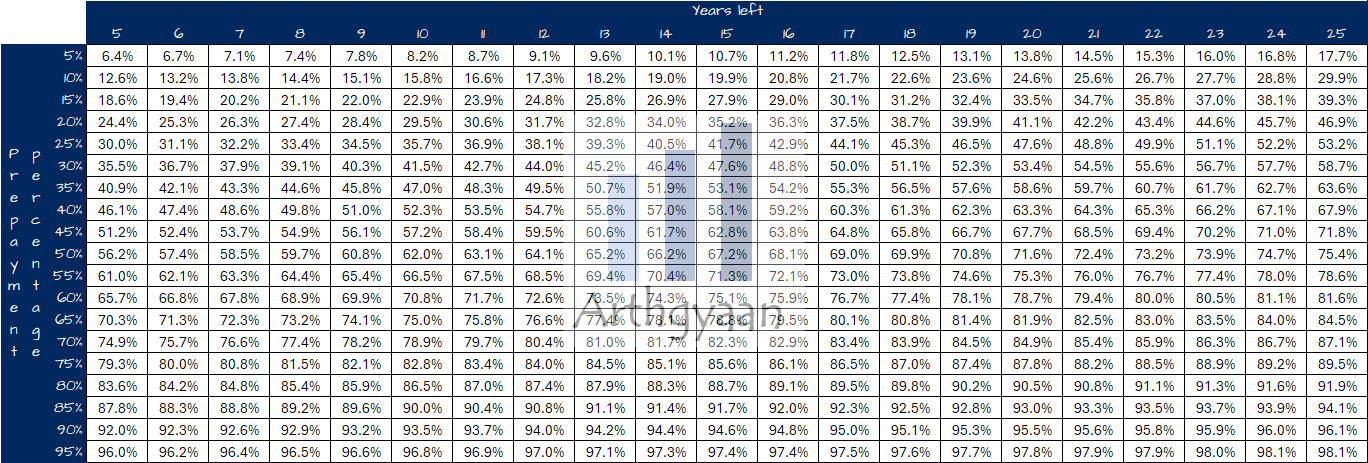

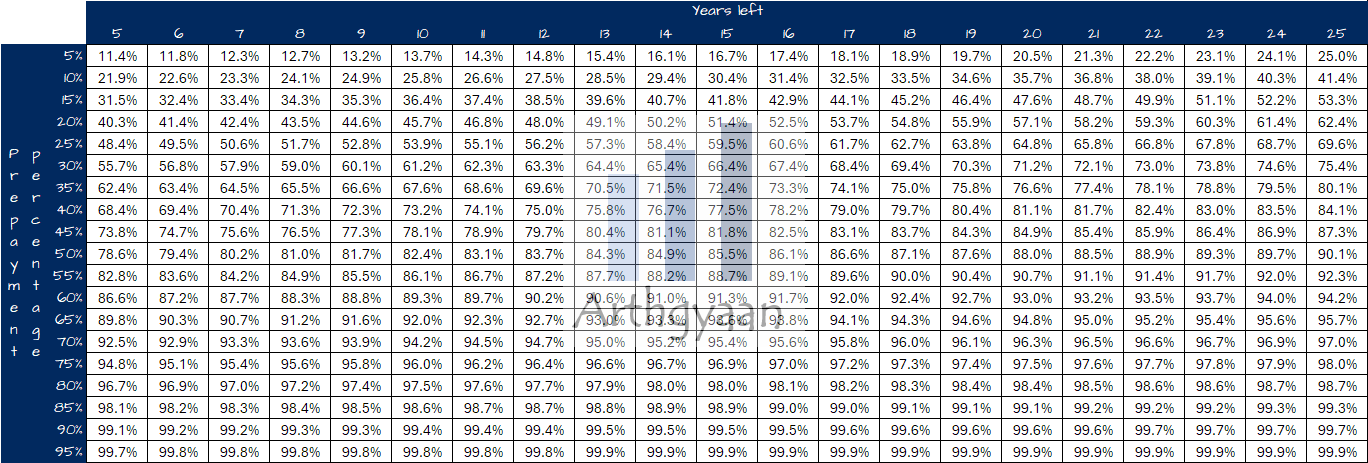

We will now look at the effect of a single prepayment. The logic here is that the prepayment immediately impacts the principal and effectively makes the loan smaller.

Warning: Depending on how the bank (or NBFC) treats home loans, the prepaid amount may not hit the principal immediately. Also some lenders reduce the EMI and others reduce the loan tenure. It is up to you to check with the lender that the principal is reduced immediately and the duration is reduced. Reduction of duration saves the interest you need to pay over time.

Should you prepay your home loan? We have discussed this in detail here: Should you use your stock market profits to prepay a home loan?.

We will now use a sample home loan to see what happens when you prepay. If you are using Excel to calculate your home loan EMI, the formula to use is:

EMI = PMT(rate/12,time * 12,-principal,0,0)) where time = years left to pay the loan

Interest paid = EMI * Number_of_EMIs - Principal left

| Metric | Value |

|---|---|

| Loan balance (₹ lakhs) | 50 |

| Rate of interest | 10.00% |

| Years left | 15 |

| EMI | ₹53,730 |

| Total interest to be paid | ₹46,71,446 |

| Prepayment % | 30% |

| Prepayment amount (lakhs) | ₹15 |

| New loan period (months) | 94 |

| Interest saved | ₹15,67,630 |

| Time savings | 48% |

| Interest savings | 66% |

We will now look at various savings values for interest and time if you make a one time prepayment.

You should approach your lender to reduce it. This article shows the benefits of reduction: How paying a small fee to your bank can save you lakhs in home-loan interest?.

1.Email mewith any questions.

2. Use our goal-based investing template to prepare a financial plan for yourself.

![]()

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This page titled What benefit do you get if you make a one-time prepayment to your home loan? first appeared on 04 Oct 2023 at https://arthgyaan.com

Made by Arthgyaan with ❤ in 🇮🇳