This guide breaks down what term insurance is, why it’s crucial for financial planning, and how much coverage you actually need for financial goals like your child’s education, home loans, and retirement planning.

This guide breaks down what term insurance is, why it’s crucial for financial planning, and how much coverage you actually need for financial goals like your child’s education, home loans, and retirement planning.

Term insurance is a type of life insurance that pays a benefit to the named beneficiaries in the event of the insured person’s death, as long as the policy is active. The purpose of term insurance is to provide financial protection for the policyholder’s loved ones in the event of their unexpected death, helping to cover daily expenses, future goals such as children’s education, and loans like home loans.

It is a straightforward insurance product, similar to car insurance, in that it only pays out in the event of a specific occurrence (death) and does not have a savings component like other types of life insurance. Term insurance offers high coverage at a low cost and is the cheapest insurance plan that you can purchase to protect your family’s lifestyle and financial goals in case you die.

Insurance spreads financial risk across a large pool of policyholders, reducing individual financial burden. Since many people buy insurance, only some are expected to die within the policy’s coverage time. However, it should be present at least for all earning members of the family before retirement age.

Why do you need term insurance for your investment goals?

Term insurance protects against loss of income. One of the uses of that income is investing for goals like children’s college education, retirement, house purchase etc.

If you die prematurely, your family no longer has your income to cover these goals.

Objection: We are a dual income household and don't need a lot of insurance

Response: This assertion is true only if the financial goals can be scaled down as per the remaining spouse's income.

While it can be argued that a dual-income household will be able to adjust retirement expenses, it won’t be easy to assume that future expenses like children’s college and fixed expenses like housing costs (maintenance, household help, electricity etc.) will be adjusted to be funded from a single income source. This becomes all the more important if the spouses have a large difference in incomes.

Objection: I have investments, so I don't need term insurance.

Response: Investments can fluctuate in value, while term insurance provides a guaranteed payout to your family in case of your absence. Once your investment goals are funded, you can discontinue the policy.

Therefore, it is important to calculate the impact of your financial goals to be sure that your insurance coverage is sufficient.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Start Building Wealth with Expertly Curated Mutual Fund Packages

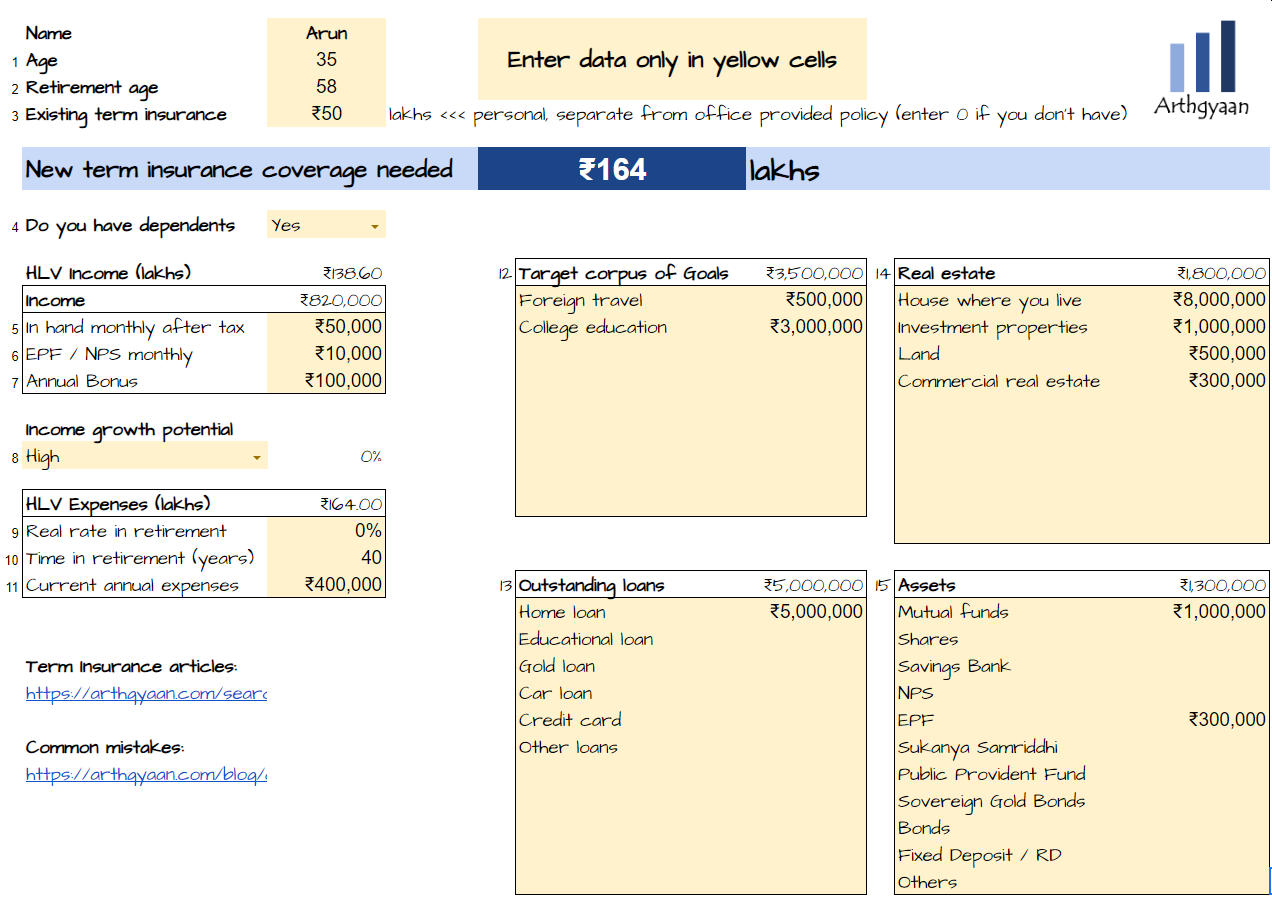

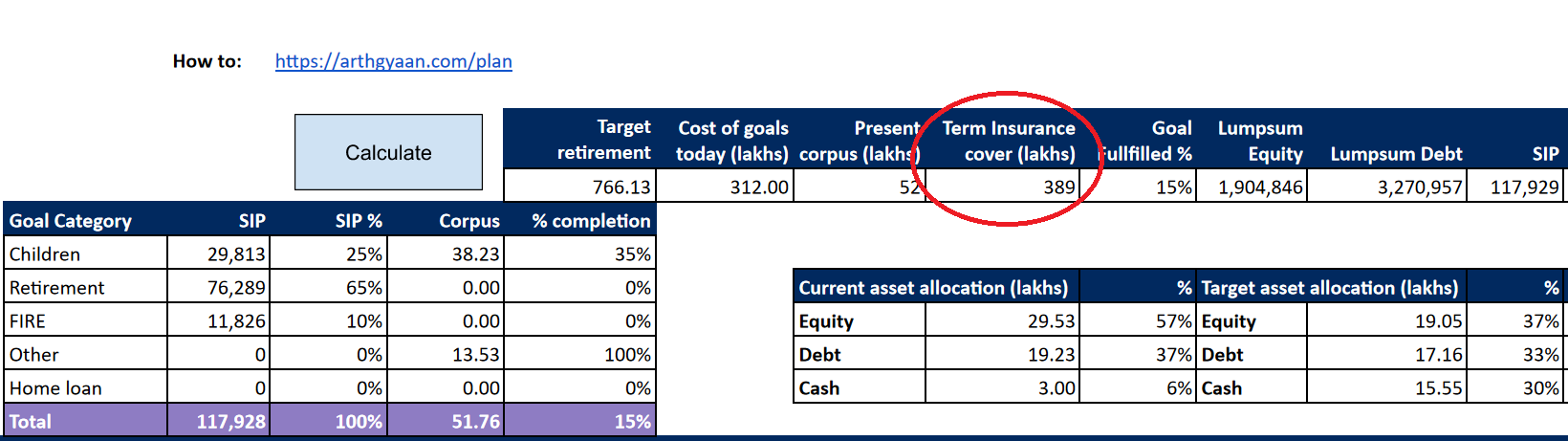

the shortfall of current goals. If income stops, this amount, if invested, will fund current goals

the amount needed to sustain a retirement-level lifestyle, including inflation adjustment, for the period income was expected to be there.

This figure is the minimum since you need to add any ongoing outstanding secured loans (like home or car loans) or loans where family members may be co-borrowers to this coverage amount. This means that if you have 30 lakhs in an outstanding home/car loan or an educational loan of 10 lakhs with parents as co-borrowers, add those amounts to the term insurance coverage.

Objection: What about the HLV income or expense models of calculating term insurance coverage?

Response: Both are valid models for calculating how much insurance you need. Our calculator ensures that you do not miss out on any extra amount that you might need for your goals.

There is another calculator that you can use if you want a quick and free solution:

We will use Google sheets to create a simple calculator for this calculation. There is a link to download a pre-filled copy of the Google sheet via the button below.

Important: You must be logged into your Google Account on a laptop/desktop (and not on a phone) to access the sheet.

Here are some case studies using the tool (click the image below)

Please refer to the term-insurance tab of the sheet once you open it.

Is term insurance only for investment goals?

If you have a home loan or similar large amounts due say via a car or educational loan, then it is important to cover those as well. Specifically, a home loan carries several risks starting from the moment you borrow money:

What happens if you lose your job or become too ill to work?

What if your house is destroyed by fire or damaged in an earthquake?

What if you die and there isn’t enough money to cover the home loan?

What if interest rates rise and you can’t afford the monthly payments?

What if having a monthly home loan payment stops you from taking career risks like changing jobs or joining a startup?

To mitigate some of these risks, there are insurance policies:

Property Insurance: Covers damage to your house from events like fire or earthquakes.

Loan Insurance: Covers your loan payments if you die and term insurance is the cheapest insurance product to cover your loan.

The Arthgyaan calculator allows you to add outstanding loans to understand your term insurance coverage amount.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Term Insurance Explained: Why You Need It & How Much to Get For Your Financial Goals first appeared on 04 Mar 2025 at https://arthgyaan.com

]

]