This article explains why chasing performance is a flawed strategy and what investors should do instead. After all, you should not invest in the same way you buy a plane ticket - by looking at the cheapest flights first.

This article explains why chasing performance is a flawed strategy and what investors should do instead. After all, you should not invest in the same way you buy a plane ticket - by looking at the cheapest flights first.

We visit our favourite ticketing site, such as Cleartrip, and enter our travel dates. Once the results are displayed, we sort them by price in ascending order, with the cheapest flights listed first.

The site nudges you by showing the cheapest flights at the top. The screenshot above (highlighted by the maroon ovals) shows a dark pattern (a behavioural trick websites use to steer customers towards a particular activity).

There is nothing wrong with buying the cheapest plane tickets. However, if you apply the same approach to selecting and investing in the best-performing mutual funds, you might run into problems.

If you visit any mutual fund website, for example this one, the default view (highlighted by the maroon oval indicating the dark pattern) displays the highest-returning funds at the top of the list.

Since most people invest in mutual funds for high returns, it’s natural to select from the top 3 or 5 funds and invest. This article will show how this logic can lead to wealth destruction when applied to mutual fund investments.

By calculating annual returns from AMFI NAV data, we have prepared two exhibits to demonstrate what happens when you chase performance by investing in the best funds based on past performance.

What returns do you get from the best-performing funds?

We selected the top 10 best performers from the previous three years and invested equally, say ₹10,000 per fund, at the beginning of the year. After one year, we compare the average return of this portfolio with the average return of the actual top 10 funds of that same year.

Year

Top 10

Top 10 Next Year

2017

53.52%

58.03%

2018

-15.04%

-0.72%

2019

17.20%

25.98%

2020

11.58%

59.33%

2021

37.90%

65.83%

2022

-11.64%

10.82%

2023

33.53%

49.25%

Average

15.70%

36.07%

For example, using the 2017 illustration:

On 1st January 2017, you invest ₹10,000 in each of the ten highest-return funds from January 2014 to December 2016.

On 31st December 2017, you sell the entire investment for a return of 53.52%, and compare it against the average return of the best ten funds of 2017, which gave 58.03%.

The average return is 15.70% pre-tax, whereas the top 10 funds of the same year gave a higher average return of 36.07%.

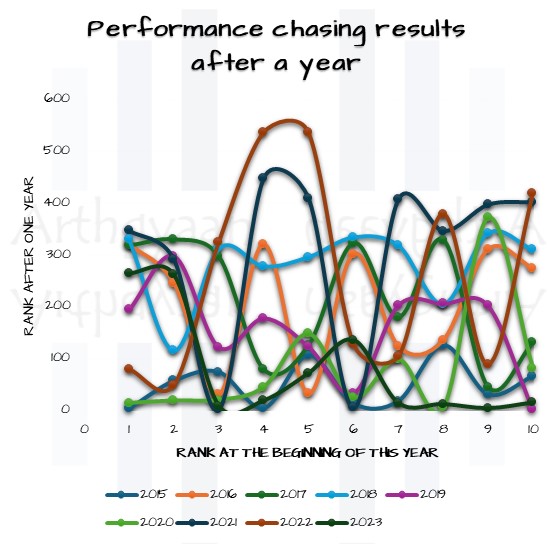

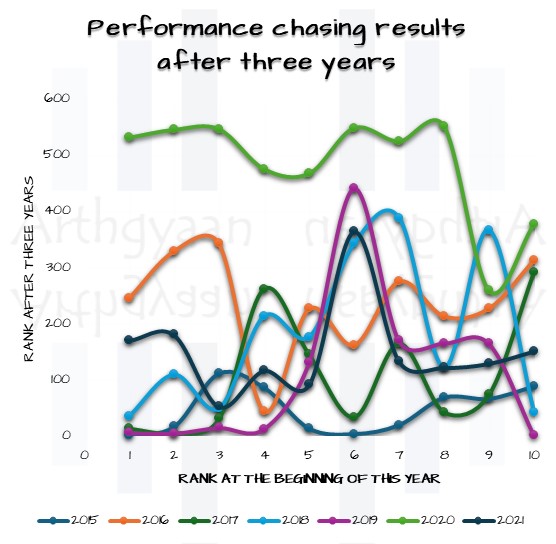

Now, we will examine what happens to the ranking of these funds once they make it to the top 10.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Start Building Wealth with Expertly Curated Mutual Fund Packages

What happens to the ranking of the best-performing funds?

We have two charts depicting the change in the relative ranking of the year’s top 10 funds over time.

The first chart shows the ranking of the top 10 funds after one year:

The second chart shows the ranking of the top 10 funds after three years:

As shown, selecting funds based solely on recent returns is a sure way to achieve poor results.

Investors should not forget that leaving a poor-performing fund to enter a new one in the hope of getting better performance has three negatives for the investor:

suffering from underperformance while you can see that other funds are doing better

paying capital gains tax on selling the old fund

being potentially unlucky that the new fund also underperforms next year

What should investors do instead of choosing the best-performing funds?

“Prediction is very difficult, especially if it’s about the future.” - Niels Bohr

There are two ways to avoid this problem, both requiring a degree of maturity that comes from investing across market cycles.

Invest only in index funds

There are multiple benefits to investing in broad market index funds that track indices such as the Nifty 50, SENSEX, or the Nifty 500. Adding other indices, like mid-cap or small-cap indices, may or may not provide additional benefits unless the investor has a strategy for market timing based on the relative movements of these indices.

Investing in index funds eliminates much of the decision-making:

Should you invest in a new fund today?

Should you exit an existing fund today?

What should you do if Fund X performs better than Fund Y?

Which new fund should you invest in when your income increases?

These decisions can be entirely avoided by investing in index funds. Active index funds, such as factor funds (momentum, quality, low-volatility, etc.), are not passive and are comparable to investing in active funds.

Invest based on conviction in the fund

Active fund investors need solid conviction in either the investment strategy of the fund or the skills of the fund manager and their investment team.

This conviction comes from analysing the consistency of the fund’s past returns relative to its peers and then hoping or trusting that the outperformance will continue. However, it can be mathematically proven that, apart from pure luck, the same fund cannot consistently be the best performer year after year.

This problem is exacerbated by the fact that investing is a multi-decade journey, and equity is a permanent asset class that should never be sold. Therefore, when inevitable underperformance begins, the second aspect of conviction comes into play: having faith that the fund manager will turn things around.

The process of an active fund falling behind its peers and then climbing back up the performance tables can take years and often leads to a permanent loss in terms of opportunity cost for the investor.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Why Chasing Mutual Fund Returns is a Proven Way to Destroy Wealth? first appeared on 15 Sep 2024 at https://arthgyaan.com