This article gives you the mathematical support regarding the financial and life-stage reasons to consider accelerating loan repayment, from income stability concerns to freeing up funds for retirement or children’s education.

This article gives you the mathematical support regarding the financial and life-stage reasons to consider accelerating loan repayment, from income stability concerns to freeing up funds for retirement or children’s education.

Who should you consider paying extra to your home loan monthly to pay off the loan quickly?

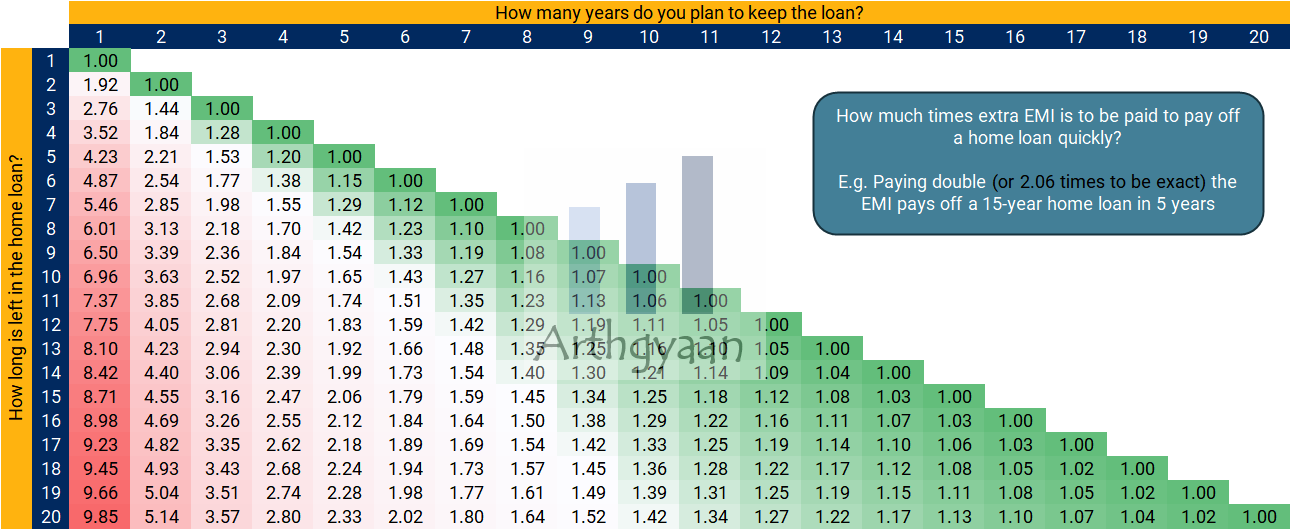

Paying double (or 2.06 times to be exact) the EMI pays off a 15-year home loan in 5 years

Should you do that? Pay off your home loan early?

There are many reasons for paying off a home loan early with reducing income stability being an important one for many in their 40s or even 50s. We have written on this topic before: How to manage a home loan if you are worried about job loss?.

In this article, we explore the options of paying off a home loan quickly, due to reasons like:

lower income due to increasing age or other workplace issues

major expenses, like children’s college education, coming up

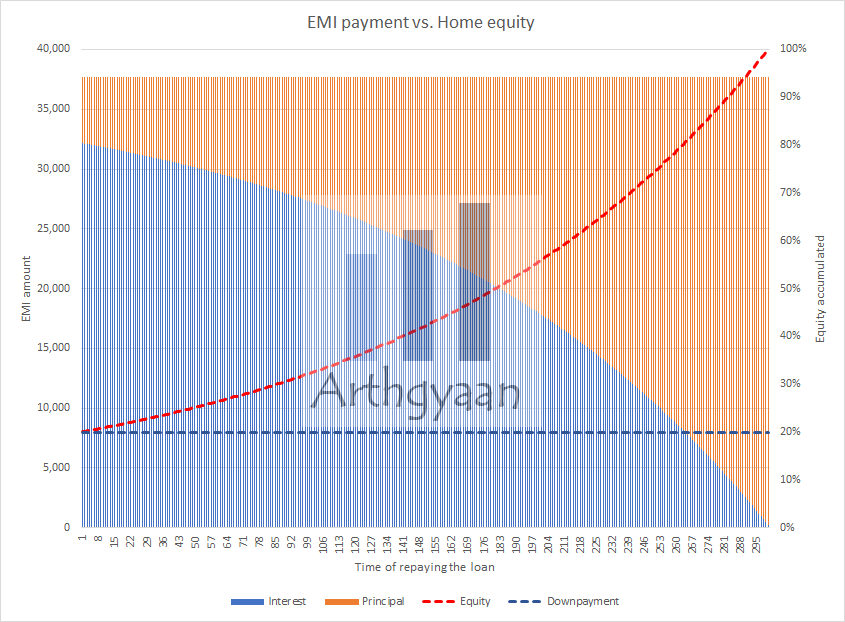

The bank gives a home loan to own the property while you use it until you pay back the loan via EMIs. An Equated Monthly Instalment plan (EMI) is a standard way to pay off a loan by making a fixed payment monthly that includes both interest and principal in the same amount.

EMI = Principal + Interest

In each EMI, the split of the interest and principal changes since the interest is based on the outstanding loan balance at that point and the rest of the EMI is principal. As the chart shows, the interest part drops off with time, and the rest is the principal. The actual numbers in the chart relate to a ₹50 lakhs home loan taken at 8% for 25 years. The EMI is ₹38,591. The down payment amount is ₹12.5 lakhs.

You can test the numbers using this calculator:

As you pay back the loan, your ownership share in the house will increase in the same way. At the point of taking the loan, you own 20% of the house (12.5 out of 62.5, of which 50 is the loan). The bank owns 80%. As the loan is repaid, you own more and more of the house as the principal is paid off. This is the concept of building equity in an asset. Equity is the part of the asset you own after subtracting the part that the bank owns.

Home equity value = Current home value - Outstanding loan balance

Once you build equity in your home, that has additional benefits:

You can take a top-up loan in case you need money for some other purpose like home improvement or any other reason.

The more you will get to keep if you sell the house.

We break down the home loan rate into its major components to see where the fluctuations come from.

Repo rate: This rate is decided by the RBI. Home loan rates will move up and down as soon as the RBI revises the repo rate.

The latest repo rate is 5.25%. This rate was last reviewed by the RBI on 05 Dec 2025.

Spread: This is an additional rate on top of the repo rate that essentially captures the profit the bank can make off this loan relative to the deposits it offers to customers. This rate is generally revised every three years but will vary from bank to bank.

Premium: An extra value for some specific customers. For example, SBI adds another 15 bps for non-salaried customers or it will depend on the CIBIL score of the borrower. This value is also revised periodically, like every three years.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Start Building Wealth with Expertly Curated Mutual Fund Packages

How much times extra EMI is to be paid to pay off a home loan quickly?

Here we have assumed that the loan interest rate is 8.8% which is applicable for loans above ₹1 crore. Lowering the interest rate to say 8.5% does not materially impact the numbers in the table below.

Read the above table as :

to pay off a 15-year loan in 5 years, pay double the EMI (exact = 2.06 times the EMI)

to pay off a 20-year loan in 10 years, pay 1.42 times the EMI

etc using the equation

Increased EMI = x times ActualEMI where x > 1

where table gives the values of x for various combinations of home loan tenure left and desired time to pay off the loan.

To understand if you should increase your EMI for your home loan:

Our home loan prepayment vs investment decision calculator uses the concept of NPV to help you decide which option is better:

Home Loan Prepayment Decision Calculator (India)

Loan & Investment Details

Tax & Borrower Details

Scenario Comparison

Click "Calculate & Compare" to see the results.

Loan Amortization

Year

Loan Left

Principal Repaid

Interest Paid

Tax Savings

MF Corpus

To choose best mutual funds for prepayment of loan:

Net Present Value (NPV) Comparison

NPV is calculated over the full original term of the loan, using the Expected MF Return as the discount rate. A higher (less negative) NPV is better.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Pay Off Your Home Loan Faster: How Extra EMI Payments Save Time and Money first appeared on 01 Dec 2024 at https://arthgyaan.com