This article reviews the re-entry of Franklin Templeton AMC into the segment of Ultra Short Duration funds after a similar fund got shut during the COVID pandemic.

This article reviews the re-entry of Franklin Templeton AMC into the segment of Ultra Short Duration funds after a similar fund got shut during the COVID pandemic.

What is the Franklin India Ultra Short Duration Fund?

Franklin India Ultra Short Duration Fund is an Ultra Short Duration Fund re-launched by Franklin Templeton AMC, available for investment since 30th August 2024.

This fund, whose New Fund Offering (NFO) concluded on 28th August 2024, marks the re-entry of Franklin Templeton into certain segments of debt mutual funds where it had been absent since April 2020.

What is the story of Franklin Templeton regarding debt mutual funds?

On 23rd April 2020, at the height of the COVID-19 pandemic, Franklin Templeton announced the winding up of six debt mutual funds, including the Ultra Short Bond Fund, citing market conditions due to the pandemic. Later investigations revealed that these Franklin funds had taken extra risks in investing, which initially provided good returns under normal market conditions. However, due to COVID-19, the debt market no longer allowed Franklin fund managers to trade the bonds in their portfolios, leading to the shuttering of these funds.

The official reason, as per Franklin Templeton website, is this:

There has been a dramatic and sustained fall in liquidity in certain segments of the corporate bonds market on account of the Covid-19 crisis and the resultant lock-down of the Indian economy which was necessary to address the same. At the same time, mutual funds, especially in the fixed income segment, are facing continuous and heightened redemptions.

It took more than three years and the intervention of the Karnataka High Court to wind up the portfolios of these six funds and return the entire amount-more than ₹27,000 crores-to the unit-holders. Until the entire amount was returned, which happened in multiple tranches as the bonds were sold, investors had no choice but to wait, hoping they would at least get their principal back.

Since the money was returned over three years, the investors lost the return over this period (the so-called opportunity cost) along with any plans they had, for example to fund medical expenses in the middle of the worst pandemic in a century, for their hard-earned money.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

What does the Franklin Templeton story regarding debt mutual funds teach us about risk?

Liquidity risk is a financial risk that, for a certain period of time, a given financial asset, security, or commodity cannot be traded quickly enough in the market without impacting the market price. (Wikipedia)

This incident, the first of its kind in India, is a perfect example of how both fund managers and investors chase returns at the cost of risks that can materialise in unknown or unexpected ways.

Just like higher returns come with higher risk, just taking higher risk does not always mean that the return will always be high.

In the pre-pandemic period, the fund managers of Franklin Templeton invested in bonds that no longer had any takers in the bond market when the pandemic hit. Since nobody wanted to buy these bonds, except at a severe discount to the expected price, Franklin Templeton had no choice but to close these funds. This is how liquidity risk, brought on by the pandemic, led to the closure of the funds.

Many investors, who had previously invested in these funds due to their higher-than-category returns, were suddenly cut off from their money. Open-ended mutual funds, which are typically the type of funds most people invest in, are always expected to allow investors to enter (i.e., buy) or exit (i.e., sell) at the NAV of the fund. Franklin Templeton decided to change the rules of the game by closing the funds without unit-holder consent, citing liquidity issues.

However, the Franklin Templeton fund managers made a conscious choice to invest in such bonds, going against the spirit of their mandate. We will explain this with an example.

Ultra Short Duration Funds invest in Debt & Money Market instruments with a Macaulay duration of the portfolio between 3 months and 6 months.

The above excerpt from the SEBI definition of Ultra Short Duration Funds hints at how the system can be gamed.

The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. (Investopedia)

The Macaulay duration (MD) of the portfolio can be imagined as the average of the MD of the individual bonds in the portfolio. The problem with an average, as a statistical measure, is that it is affected by extreme values.

For example, it would generally be unwise to take admission to an MBA college where most students (say 8 out of 10) are placed at a salary of ₹10,000/month, and the rest (2 out of 10) receive a salary of ₹100,000/month.

The average salary of ₹28,000/month is extremely misleading for prospective candidates who, perhaps because they have not yet studied for an MBA, might misunderstand how to interpret the average salary statistic. Similarly, holding a few long-dated bonds with higher yields (higher since the bonds will mature much later) along with a few extremely short-dated ones will keep the average maturity of the portfolio within prescribed “ultra-short” limits but provide higher-than-average returns due to the presence of the long-dated bonds.

Note: We are loosely conflating Macaulay duration with portfolio duration, though they are not the same. This does not change the conclusion of how averages can be misused to hide risks.

Start Building Wealth with Expertly Curated Mutual Fund Packages

What should investors do regarding Franklin India Ultra Short Duration Fund?

It all comes down to trust at this point. Is there an expectation that Franklin Templeton will do the right thing this time and stick to both the letter and spirit of the SEBI rules regarding the portfolio of the new fund?

Yes, investors will have that expectation. The AMC has taken a few steps in the right direction on this.

For example, one of the fund managers is MD/CIO Fixed Income Rahul Goswami, who joined the AMC in 2023, thereby bringing in fresh ideas (hopefully!) and perhaps better insights on risk management. This may create some expectation that the other fund manager of this fund, Pallab Roy, a veteran at Franklin Templeton since 2001, will not repeat the steps that led to the situation in April 2020.

Investors wary of Franklin Templeton’s return to this debt fund segment should remember that there are already 24 funds in this segment. There is no compelling reason, except in a few cases where a Franklin Templeton debt fund might be used to SWP into one of their equity funds, to rush to invest in Franklin India Ultra Short Duration Fund.

As per SEBI guidelines, each AMC publishes a portfolio of their debt funds every fortnight. Once the fund publishes a few of these portfolios and builds sufficient history of adhering to the definition of the Ultra Short Category without taking any so-called unnecessary risks, investors can revisit this fund.

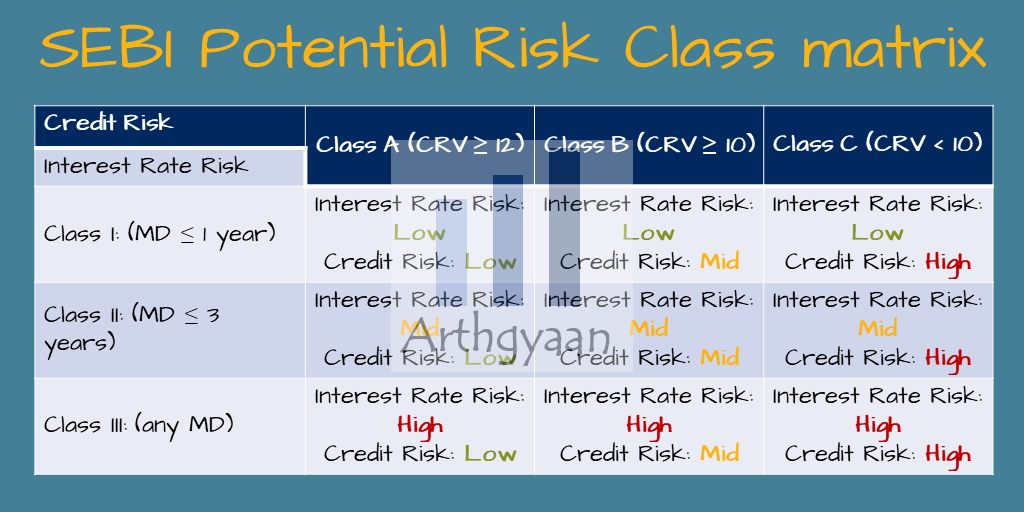

What other risks are there in the Franklin India Ultra Short Duration Fund?

It is important to note that the SEBI definition of the Ultra-Short Duration category does not address the credit risk of the bonds in the portfolio. It is very easy to take risks in that aspect of the portfolio as well, in order to improve returns.

Again, it is important to correlate the fund portfolio, once there is portfolio disclosure data of sufficiently long duration, for an investor to determine whether this fund suits their requirements for both return and risk.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled FRANKLIN INDIA ULTRA SHORT DURATION FUND relaunch: Should investors again trust Franklin Templeton for this debt fund? first appeared on 02 Sep 2024 at https://arthgyaan.com