This article breaks down the misconceptions about stock investing and provides actionable advice on why you should avoid individual stocks and invest for the long term.

This article breaks down the misconceptions about stock investing and provides actionable advice on why you should avoid individual stocks and invest for the long term.

When does an investor lose money in the stock market?

There are many ways of losing money in the stock market:

a permanent loss of capital when a stock price falls and does not recover.

returns over time, including dividends, do not beat inflation

sequence of returns is such that average returns are good, but the investor ends up with too less returns for their goals

However, even in these situations where money is lost in the stock market, there are two rules that, based on historical data, show that you will very unlikely lose money in the stock market.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Rule 1 to never lose money in the stock market: never buy individual stocks

The Academic Research that Supports Never Buy Individual Stocks

A 2017 study “Do Stocks Outperform Treasury Bills?” by Hendrik Bessembinder, published in the Journal of Financial Economics, analysed the lifetime returns of U.S. common stocks from 1926 onwards.

There are two takeaways from this study:

Concentration of Wealth Creation: The study found that the top-performing 4% of listed companies accounted for the entire net gain in the U.S. stock market since 1926. The remaining stocks collectively performed no better than one-month Treasury bills.

Positive Skewness: The distribution of individual stock returns is highly skewed, with a small number of stocks generating substantial returns while the majority underperform

These two results, which effectively say that:

To make money from the stock market, you need to be invested only in the top-performing stocks consistently

You need to identify these top-performing stocks in advance

You need to stop investing in under-performing stocks sooner rather than later

The Psychology of the Single Stock Investor

Every long-term investor in individual stocks sincerely believes in three things:

that their research in their stock portfolio is sufficient to create wealth

they will be able to identify good stocks in advance

they will be able to hold on to good performers and not sell them prematurely

On the flip side, they also believe, implicitly in some cases:

they will be able to avoid investing in poor-performing stocks in advance

they will be able to exit from such positions before they lose too much money

As we have argued before, when investing in individual stocks, you are running a single-person mutual fund. This implies three things:

your day job, family commitments and other interests allow you sufficient time to analyse the entry and exit points of individual stocks

you know which stocks will perform better out of the potential 5000+ stocks in the market today and similarly which stocks will perform badly in advance

you know how to do this activity better than professional fund managers who have formal training and access to research teams, databases and other resources to justify managing thousands of crores of other people’s money

The Solution that Solves this Problem of Avoiding Losing Money in Individual Stocks

Buy the stock market index via passive index mutual funds

A lot of stock investors will scoff at this point. This article is not for them.

Instead, this article argues that:

an index which passively tracks the market (whether 50, 100 or 500 stocks) will never be the best but will never be the worst as well

a stock market index systematically buys stocks when they are priced low and sells them when they are priced high

a stock market index has never (barring extreme situations like Russia in 1917 due to the Bolshevik Revolution and privatisation in China in 1949) gone to zero unlike individual stocks

depending on how the index is constructed, the best-performing stocks are automatically added to the index while the poor-performers are methodically removed

There is already enough evidence that active mutual funds, including the one-person funds run by individual investors, do not beat the market index.

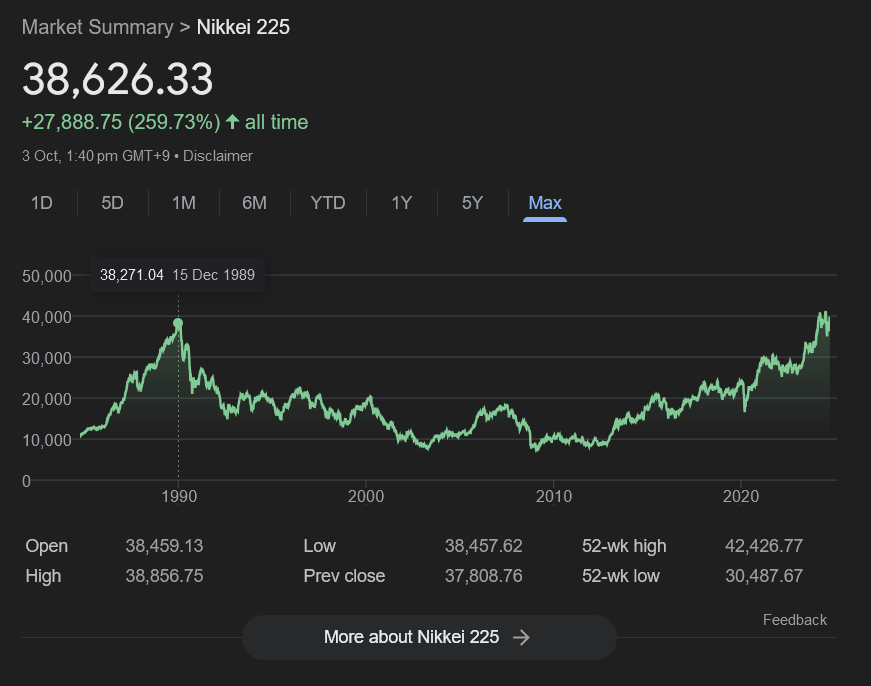

Note: It is important to mention that one common example that is given every time index performances over long periods are mentioned is the performance of the Japanese Nikkei 225 index after the Black Monday crash of 1987 where the index value in 1989 was only recently reached in 2024 as the chart below shows.

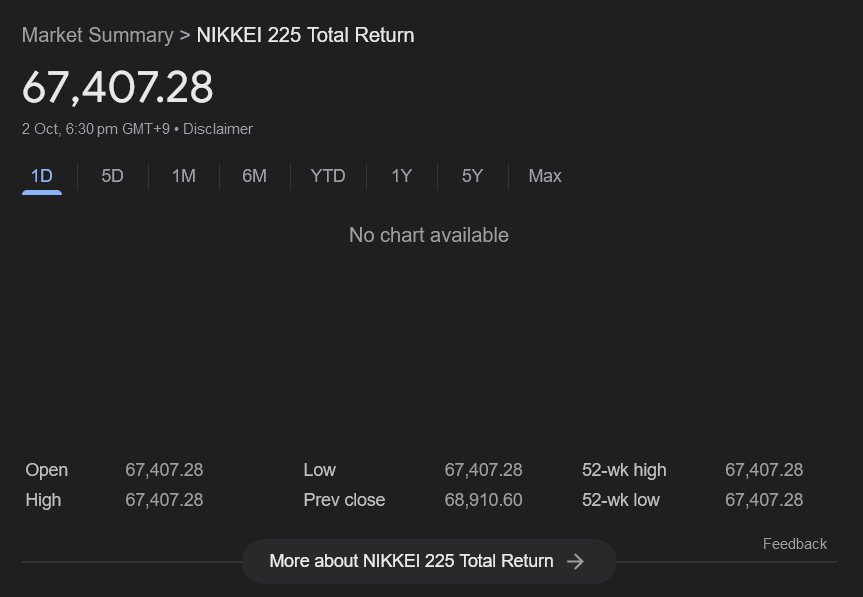

However, it is important to note that the Nikkei 225 Total Returns Index, which includes reinvested dividends has given a modest 1.56% extra returns, per year, over the price index for the last 35 years.

Given Japanese inflation values of either negative or less than 1%, this is not as bad as a total return as a cursory view of the index returns will show.

Start Building Wealth with Expertly Curated Mutual Fund Packages

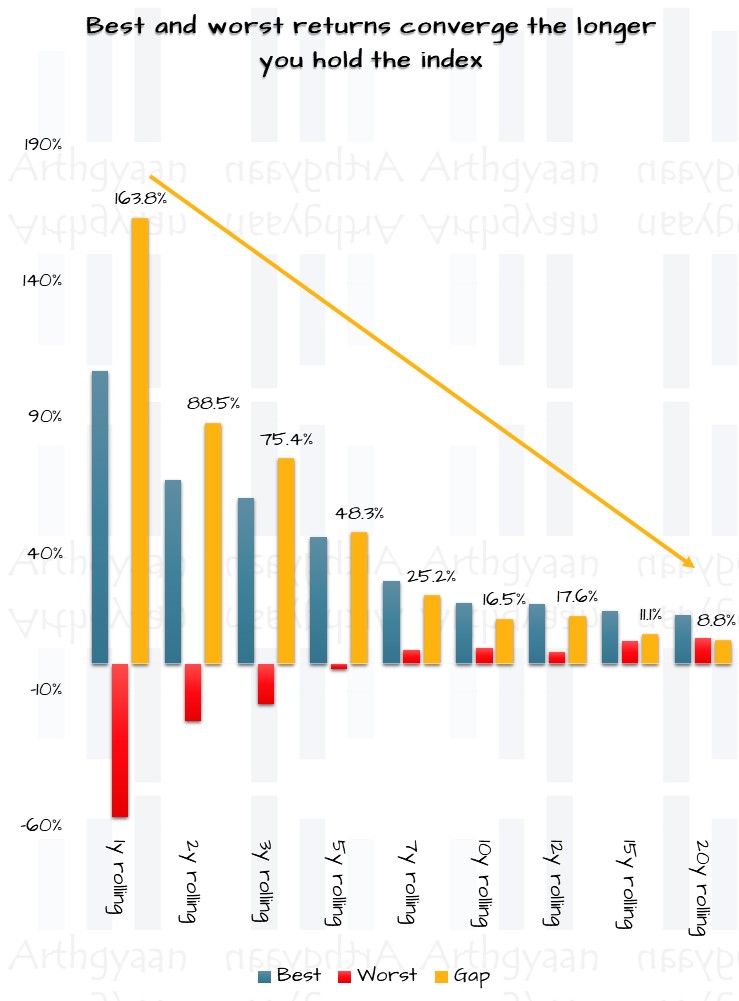

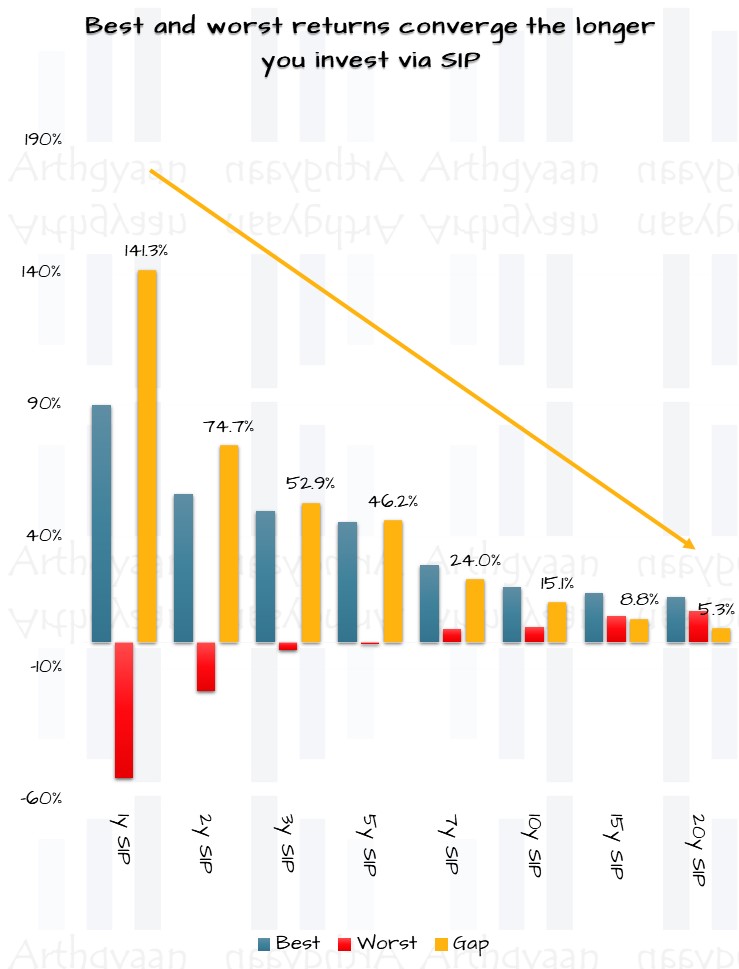

Rule 2 to never lose money in the stock market: only invest for the long term

Stock market returns converge towards the average as time passes for both positive and negative values.

We have used data for the Nifty 50 index data and included dividends i.e. the Nifty 50 Total Returns Index from 1996 onwards. We have used this data to calculate returns over 1Y, 2Y, 3Y, 5Y (for the short-term) and 7Y onwards for the long-term and calculated both lump sum and (monthly) SIP returns.

Lump sum return convergence for long-term investments

SIP return convergence for long-term investments

How to use these two rules to minimise your chances of losing money in the stock market?

The rules explained in the article are:

We need a way to ensure that we never invest in underperforming stocks. The easiest way to do this is to invest in a broad-market index fund: Which index funds to invest in and why?

We need to figure out that we never invest in the stock market for the short term while investing adequately for our goals in the long term. We show how to do this easily below:

We need a method to divide your entire portfolio into these 12 categories (3 buckets: equity/debt/cash and 4 time-based groups) and allocate the correct amount of mutual funds to each.

We will use Google sheets to create a simple calculator for this calculation. There is a link to download a pre-filled copy of the Google sheet via the button below.

Important: You must be logged into your Google Account on a laptop/desktop (and not on a phone) to access the sheet.

Here are some case studies using the tool (click the image below)

This table is in the “goals” tab on the right.

This way you can use the learnings from both histories, i.e. Hendrik Bessembinder’s paper, and the simple observations that over the long-term, the stock market index has made more money than it has lost.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled How to Avoid Losing Money in Indian Stocks: 2 Proven Strategies for Long-Term Success first appeared on 06 Oct 2024 at https://arthgyaan.com