This article debunks common myths about SIPs and SWPs, showing how unpredictable returns impact wealth creation and retirement planning since you will never get fixed steady or average returns.

This article debunks common myths about SIPs and SWPs, showing how unpredictable returns impact wealth creation and retirement planning since you will never get fixed steady or average returns.

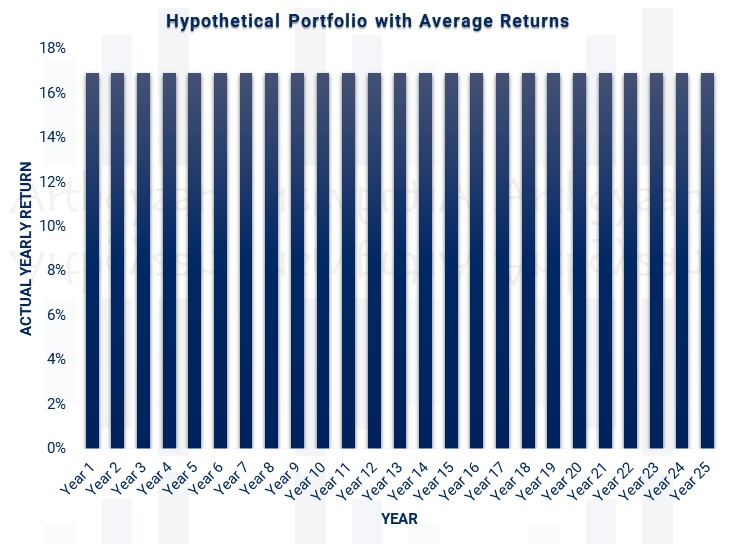

Have you ever seen a SIP investment chart that looks like this?

You must have since they are everywhere.

Question: What is wrong with the image above?

Answer: It assumes that the stock market grows like an FD, a bit like this:

with an average return quoted as 12-18%, depending on how aggressive the mutual fund sales pitch is currently being.

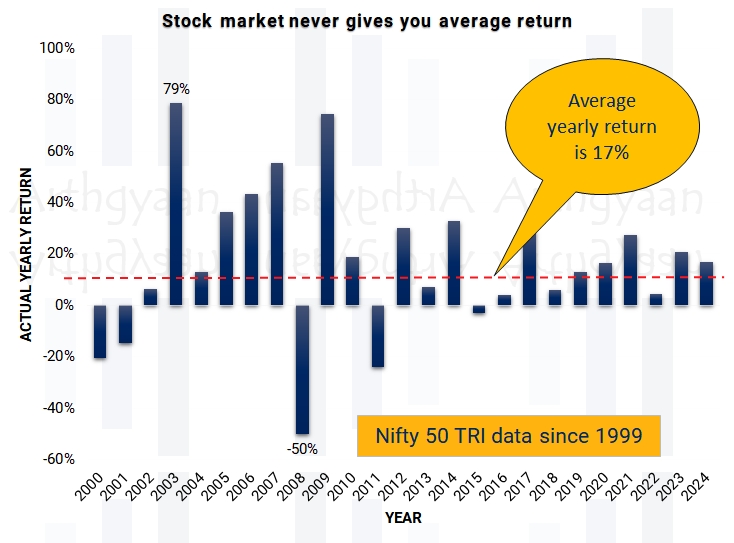

In real life, stock markets do not behave as simply as implied by the “Start SIP today” mantra. The average return that is assumed is something you will never get since the actual stock market returns look like this:

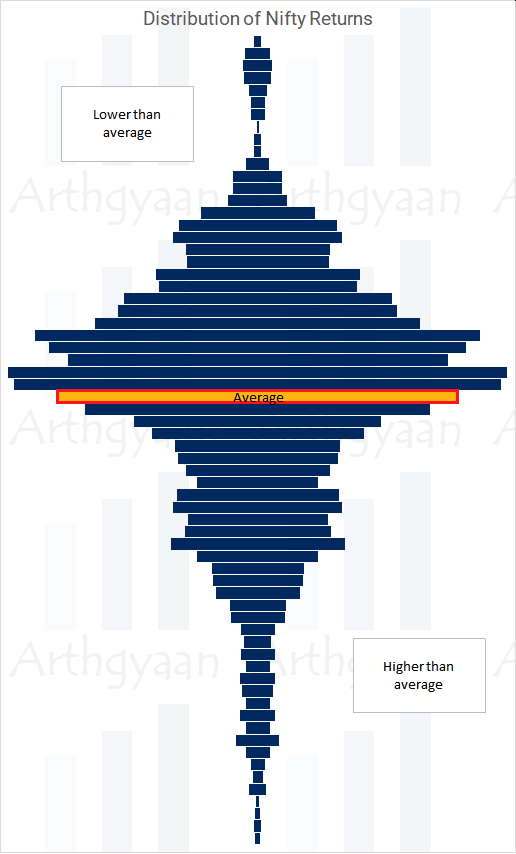

We have taken data since 1999 for our analysis of checking how many times we actually get average returns. Here the average return is 17% of the Nifty 50 index with dividends reinvested, but never in this period was the return that average value. If we use rolling returns (1st Jan this year to 1st Jan next year, 2nd Jan this year to 2nd Jan next year etc.), then the true picture emerges like this:

This picture clearly shows that amongst all the actual one-year returns, only around 10-12% of returns are around the average. The rest of the returns are lower or higher and that is as expected from a risky asset like equity.

What does this mean in real life? We will give two examples.

Another popular use case is withdrawing via SWP in retirement. If the SWP amount (as a percentage of the corpus is high, then you can suddenly run out of money like this:

(click to open in a new tab)

This is the case where in the beginning of retirement, the market returns were poor. If you withdraw too much when the markets are down, especially at the beginning of retirement when the portfolio is small, then you will likely never recover. This is the concept of Sequence of Return Risk (SRR).

This example is described in detail here: The lie of enjoying financial freedom via SWP from mutual funds

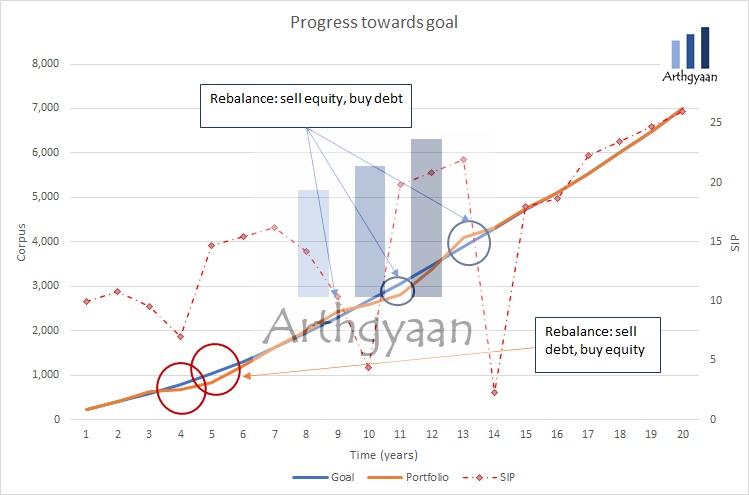

What should the investor do then if average returns cannot be assumed?

The right process is an annual review combined with rebalancing which is used for risk management to achieve one goal: over time, the risk of the portfolio needs to reduce as the goal comes closer. This is done via stepwise reduction of the equity exposure of the goal. Rebalancing:

allows systematically buying low, selling high

should be done at the portfolio level (all goals together to minimize trades and taxes)

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Stock Markets do not give Fixed Return like FD: What to do instead? first appeared on 25 Dec 2024 at https://arthgyaan.com