This article shows that if your PPF account is maturing, you need not by default invest it back into PPF since you have the option of getting higher returns in mutual funds.

This article shows that if your PPF account is maturing, you need not by default invest it back into PPF since you have the option of getting higher returns in mutual funds.

PPF accounts mature in 15 years but need not be closed immediately. A matured account will keep earning interest if there is any balance.

Your PPF will mature on 1st Apr 2025 only if you have opened the account between 1st April 2009 and 31st March 2010.

The following rules govern PPF extension:

Option 1 is to Withdraw: You can withdraw the entire amount and close the account. To invest further in PPF in the future, you need to create a new PPF account that restarts the 15-year clock. So, even if you need the money, you should not close the account immediately. If you do not want to withdraw, you can extend the account, and unlimited extensions are allowed for blocks of 5 years.

Option 2 is to Extend PPF without fresh investments: if you did not put in an extension request on time, i.e. within a year of the maturity date, then this option gets activated automatically. Partial withdrawals, up to the full balance of the account, are allowed once a financial year (Apr to Mar), but you cannot invest any new money. Investors should explicitly provide instructions to the bank or post office to avoid this situation

Option 3 is to Extend with fresh investments: if you wish, you can invest up to ₹1.5 lakh per year. 80C tax deduction is allowed on this investment. You can withdraw up to 60% of the corpus when you decide to extend for each five-year extension with fresh investments once every block of five years.

Should you reinvest the PPF account back into PPF?

We should remember that a PPF account can be kept active with just ₹500/year of investment. Hence, the problem essentially simplifies to:

Step 1: Extend the PPF account for five years since this is the most flexible case. As situations change, you can invest more in the account and retain the tax exemption and guaranteed return benefits

Step 2: Decide whether to withdraw wholly or partially as per the need

Many investors choose to roll the PPF account for a further block of 5 years to get tax-free guaranteed interest.

The latest PPF rate is 7.10%

However, given that all choices have consequences, this article shows what you are missing out on returns if you keep your PPF without withdrawal account for five more years.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

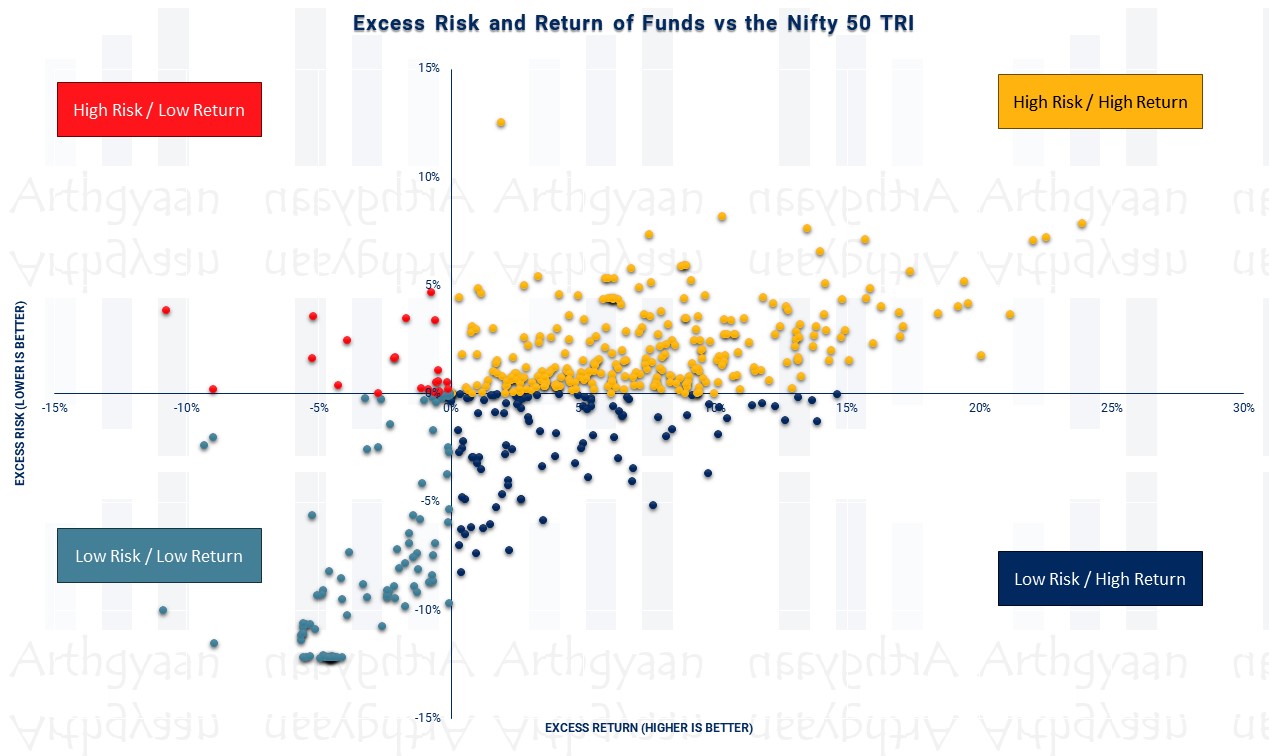

Which mutual funds are suitable for a 5-year investment where the returns are good without too much risk?

If we split the list of all mutual funds then we will end up with four categories:

funds that give better returns than the Nifty 50 index fund but with lower risk which are ideal for any investor

funds that give better returns than the Nifty 50 index fund but with higher risk which are great for investors with high risk tolerance

funds that give lower returns than the Nifty 50 index fund but with lower risk which are good for debt funds

funds that give lower returns than the Nifty 50 index fund but with higher risk which is a terrible place to be for an equity fund

Aggressive hybrid funds fall in the first category i.e. better returns at lower risk due to the inherent rebalancing that every fund performs between equity and debt due to market movement.

Exploring Aggressive Hybrid Mutual Funds as a PPF Reinvestment Opportunity

An Aggressive Hybrid Fund, as per the SEBI classification rules, must have 65% to 80% investment in equity & equity-related instruments; and 20% to 35% in Debt instruments.

We use data from AMFI to show the return performance of these funds. These are rolling returns.

You should pay close attention to the figure of lump sum returns over any 5 year period. We will now explore what happens when instead of rolling over your PPF, you withdraw and invest in Aggressive Hybrid funds.

Objection: PPF offers guaranteed returns, but mutual funds are risky.

Response: While PPF is safe, long-term data shows Aggressive Hybrid Funds often outperform PPF returns, even after adjusting for risk and taxation.

Hybrid Funds

Tax Treatment for FY2025-26

Bought Anytime

Taxed at 20% before 1 year (STCG); Taxed at 12.5% after 1 year (LTCG) for CG above 1.25L/year

These funds are taxed as equity funds. The current taxation rule is as above.

Start Building Wealth with Expertly Curated Mutual Fund Packages

In the tables below we are showing the worst, median and best 5-year lump sum returns of these funds vs. PPF. We show the worst first to tackle the argument of mutual funds are risky.

Investment in

Worst

Median

Best

Mahindra Manulife Aggressive Hybrid Fund

18.78%

21.59%

24.20%

Groww Aggressive Hybrid Fund

13.06%

15.07%

17.44%

Quant Absolute Fund

12.40%

20.47%

28.84%

Axis Aggressive Hybrid Fund

11.19%

13.45%

16.21%

Mirae Asset Aggressive Hybrid Fund

10.79%

15.00%

18.82%

Navi Aggressive Hybrid Fund

10.48%

13.87%

17.32%

Invesco India Aggressive Hybrid Fund

10.09%

15.23%

19.51%

Bank Of India Mid Small Cap Equity Debt Fund

9.52%

17.61%

30.28%

Canara Robeco Equity Hybrid Fund

8.56%

15.40%

20.34%

Bandhan Aggressive Hybrid Fund

8.01%

12.27%

19.68%

PPF

7.97%

7.97%

7.97%

SBI Equity Hybrid Fund

7.68%

14.01%

19.63%

DSP Aggressive Hybrid Fund

7.55%

14.83%

20.17%

PGIM India Hybrid Equity Fund

6.84%

11.52%

15.78%

ICICI Prudential Equity Debt Fund

6.79%

16.06%

24.97%

Shriram Aggressive Hybrid Fund

6.68%

11.20%

16.38%

Kotak Equity Hybrid

5.94%

14.47%

22.47%

Franklin India Equity Hybrid Fund

5.55%

13.06%

20.48%

Edelweiss Aggressive Hybrid Fund

5.03%

13.33%

21.86%

LIC MF Aggressive Hybrid Fund

4.10%

9.98%

15.21%

Tata Hybrid Equity Fund

4.08%

11.78%

19.53%

Aditya Birla Sun Life Equity Hybrid95 Fund

3.47%

11.60%

19.77%

UTI Aggressive Hybrid Fund

3.42%

12.10%

20.64%

HDFC Hybrid Equity Fund

3.00%

12.92%

20.06%

Nippon India Equity Hybrid Fund

0.18%

9.18%

19.96%

JM Aggressive Hybrid Fund

-1.24%

11.50%

25.73%

As expected, the list does show that in the worst case, the 5-year lump sum returns are indeed higher than PPF in some of the cases only. This is expected since equity markets are risky.

What about the cases where Aggressive Hybrid funds did not give the worst returns?

Median = Middle value of a dataset when arranged in ascending or descending order

The median is the middle value of a dataset. It is used to understand the central tendency without being affected by outliers. In investing, it can show the typical return in a way that is not skewed by extreme values. The median is best suited in data sets where the average is unsuitable.

The above table has the median values. We will now show the same data but this time we will sort it descending on median portfolio values for a ₹10 lakh investment for 5 years in PPF and aggressive hybrid funds.

Investment in

Worst

Median

Best

Mahindra Manulife Aggressive Hybrid Fund

21.94

24.51

27.11

Quant Absolute Fund

16.95

23.46

32.31

Bank Of India Mid Small Cap Equity Debt Fund

15.04

20.94

34.09

ICICI Prudential Equity Debt Fund

13.40

19.67

27.92

Canara Robeco Equity Hybrid Fund

14.44

19.16

23.33

Invesco India Aggressive Hybrid Fund

15.40

19.02

22.58

Groww Aggressive Hybrid Fund

17.41

18.90

20.79

Mirae Asset Aggressive Hybrid Fund

15.86

18.85

21.98

DSP Aggressive Hybrid Fund

13.84

18.72

23.18

Kotak Equity Hybrid

12.92

18.45

25.35

SBI Equity Hybrid Fund

13.92

18.11

22.69

Navi Aggressive Hybrid Fund

15.65

18.00

20.70

Axis Aggressive Hybrid Fund

16.12

17.69

19.79

Edelweiss Aggressive Hybrid Fund

12.43

17.61

24.76

Franklin India Equity Hybrid Fund

12.71

17.41

23.46

HDFC Hybrid Equity Fund

11.39

17.31

23.08

Bandhan Aggressive Hybrid Fund

14.11

16.86

22.73

UTI Aggressive Hybrid Fund

11.60

16.74

23.61

Tata Hybrid Equity Fund

11.94

16.52

22.60

Aditya Birla Sun Life Equity Hybrid95 Fund

11.63

16.40

22.82

PGIM India Hybrid Equity Fund

13.43

16.34

19.45

JM Aggressive Hybrid Fund

9.47

16.33

28.74

Shriram Aggressive Hybrid Fund

13.34

16.13

19.93

LIC MF Aggressive Hybrid Fund

11.95

15.33

19.01

Nippon India Equity Hybrid Fund

10.08

14.82

22.99

PPF

14.09

14.09

14.09

Average Aggressive Hybrid Fund

13.88

18.13

23.80

The next table shows the numerical difference between PPF and Aggressive Hybrid fund returns for the same ₹10 lakh investment.

Investment in

Worst

Median

Best

Mahindra Manulife Aggressive Hybrid Fund

7.85

10.42

13.02

Quant Absolute Fund

2.85

9.37

18.22

Bank Of India Mid Small Cap Equity Debt Fund

0.95

6.85

20.00

ICICI Prudential Equity Debt Fund

-0.69

5.58

13.83

Canara Robeco Equity Hybrid Fund

0.35

5.07

9.24

Invesco India Aggressive Hybrid Fund

1.31

4.93

8.49

Groww Aggressive Hybrid Fund

3.32

4.81

6.70

Mirae Asset Aggressive Hybrid Fund

1.77

4.76

7.88

DSP Aggressive Hybrid Fund

-0.25

4.63

9.08

Kotak Equity Hybrid

-1.17

4.36

11.26

SBI Equity Hybrid Fund

-0.17

4.02

8.60

Navi Aggressive Hybrid Fund

1.56

3.91

6.61

Axis Aggressive Hybrid Fund

2.03

3.60

5.70

Edelweiss Aggressive Hybrid Fund

-1.66

3.52

10.67

Franklin India Equity Hybrid Fund

-1.38

3.32

9.37

HDFC Hybrid Equity Fund

-2.70

3.22

8.99

Bandhan Aggressive Hybrid Fund

0.02

2.77

8.64

UTI Aggressive Hybrid Fund

-2.49

2.65

9.52

Tata Hybrid Equity Fund

-2.16

2.43

8.51

Aditya Birla Sun Life Equity Hybrid95 Fund

-2.46

2.31

8.73

PGIM India Hybrid Equity Fund

-0.66

2.25

5.36

JM Aggressive Hybrid Fund

-4.62

2.24

14.65

Shriram Aggressive Hybrid Fund

-0.75

2.04

5.84

LIC MF Aggressive Hybrid Fund

-2.15

1.24

4.92

Nippon India Equity Hybrid Fund

-4.01

0.73

8.89

PPF

0.00

0.00

0.00

Average Aggressive Hybrid Fund difference with PPF

-0.21

4.04

9.71

What about investing ₹1.5 lakhs in PPF between 1st and 5th April?

Investing ₹1.5 lakhs into PPF before 5th April gives the full interest on that amount for the rest of the year.

We have already shown that the alternative i.e. making a ₹12,500/month investment in PPF does not materially change the PPF corpus in 15 years which means that you can invest the rest of the amount as per your long-term goals at potentially higher returns: How to get the most interest when investing in PPF?

That being said, we have shown that for continuing PPF investments, whether ₹1.5 lakhs in April or ₹12,500/month, you are deliberately suppressing your portfolio returns if your asset allocation is already debt-heavy: SENSEX vs PPF report card: should you invest 1.5 lakhs in PPF in April?.

What is the conclusion of this analysis of moving PPF into Mutual Funds?

Investing is about trade-offs and it is important to understand the opportunity costs of each investing decision made.

Trade off

PPF

Mutual fund

Return

Low

High

Tax

None

12.50%

Market Risk

No

Yes

Withdrawal

Up to 60%

Any amount Any number of times

If you are choosing to roll your PPF maturity amount again into PPF for 5 years, then

You are consciously giving up the 4.04 lakhs median extra amount just to avoid the 0.21 lakhs loss « this is the trade-off of guaranteed returns

You are of course giving up on the 9.71 lakhs extra in the average best-case

You are absolutely certain that you will need the exact PPF maturity amount on 1st April 2030. It cannot be needed a day earlier and the exact 14.09 lakhs (for a 10 lakhs investment is needed)

You are keeping the money locked up based on post-extension PPF withdrawal rules « trade-off of lack of liquidity

Objection: I need a fixed sum in five years.

Response: If your financial goal is time-sensitive, keeping your PPF intact may be better. However, if you have flexibility, hybrid funds could offer higher returns.

If you have an iota of doubt in any of the above scenarios or :

You don’t need an exact sum immediately on 1st April 2030 and can wait for the market to recover if it has fallen at that time

If your PPF corpus is large, higher returns could significantly impact your portfolio

You are a seasoned mutual fund investor and are looking for options beyond fixed returns

You don’t have a concrete plan for your PPF corpus and are looking for what to do next

Note: If you change your mind and want to withdraw from PPF after extending it, you can do so only up to 60% of the balance at the point of extension of the account either at one go or in parts over the 5-year extension window.

Our choice of Aggressive Hybrid funds for this analysis is just an example. Many different mutual fund categories can find a place in your portfolio based on what you need.

To understand which mutual funds can be an alternative for PPF:

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled PPF Account Maturity in 2025: How Much Higher Returns Can You Get if You Withdraw and Invest in Mutual Funds? first appeared on 31 Mar 2025 at https://arthgyaan.com