This article guides retirees and FIRE aspirants on using the Arthgyaan goal-based investing tool to incorporate diverse income sources like rent, pension, royalties, and commissions into your portfolio.

This article guides retirees and FIRE aspirants on using the Arthgyaan goal-based investing tool to incorporate diverse income sources like rent, pension, royalties, and commissions into your portfolio.

How can you add multiple income streams to your portfolio for retirement?

Having multiple income streams, once standard only with professionals (doctors, lawyers, CA etc), authors and commission-based agents, is now common and necessary for most individuals retiring at their normal retirement age or earlier.

In this article, we will understand how to use the Arthgyaan goal-based investing tool to add incomes from rent, interest, pension, royalty, commission, or any other source, with or without an inflation adjustment, to your portfolio.

Why having multiple sources of income is good for your portfolio?

Having multiple income sources in retirement will reduce the amount of retirement corpus you need.

FIRE = Financial Independence Retire Early

In fact, the definition of Financial Independence (FI or FIRE) means that income from your assets can meet your current expenses. You can then optionally Retire Early (RE in FIRE) if this income grows with inflation for the rest of your life.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Which income sources should you capture via this tool?

This tool will help you enter the income from sources which you already know today. For example, if you have a book from which you get ₹1 lakh royalty per year, you can include that. The same should be true for real estate (rental income) that you already own should be captured here.

However, if you wish to invest in real estate for rental income after you retire, then do not enter that here. The same logic applies to the income from your cash bucket in retirement which will be filled by income from the debt bucket.

The only exception to this rule is if you are planning to start a low-stress job or consulting gig post-retirement and you can enter the projected income from that here. Professionals like doctors, lawyers and CAs should also do the same.

Here’s a list of income sources that you can enter in the sheet:

FD interest for FDs you already have

Dividend income from stocks you already own

A part-time job that you are planning to take post-retirement (BaristaFIRE cases)

Royalties from books that you have already written (if you are a professional author, you can include royalties from future books as well)

Pension income from annuities that you have already taken

Insurance payouts from whole life or endowment plans whose future payouts are known

Rent from property you already own

Interest from bonds, government or corporate or gold (SGB), from bonds you already have

Consultancy roles you plan to take up in the future

Professional income (for doctors, lawyers, CA etc)

Commissions for insurance agents, mutual fund distributors etc.

The tool also lets you enter the tax rate, at an aggregate level, on this entire income.

Start Building Wealth with Expertly Curated Mutual Fund Packages

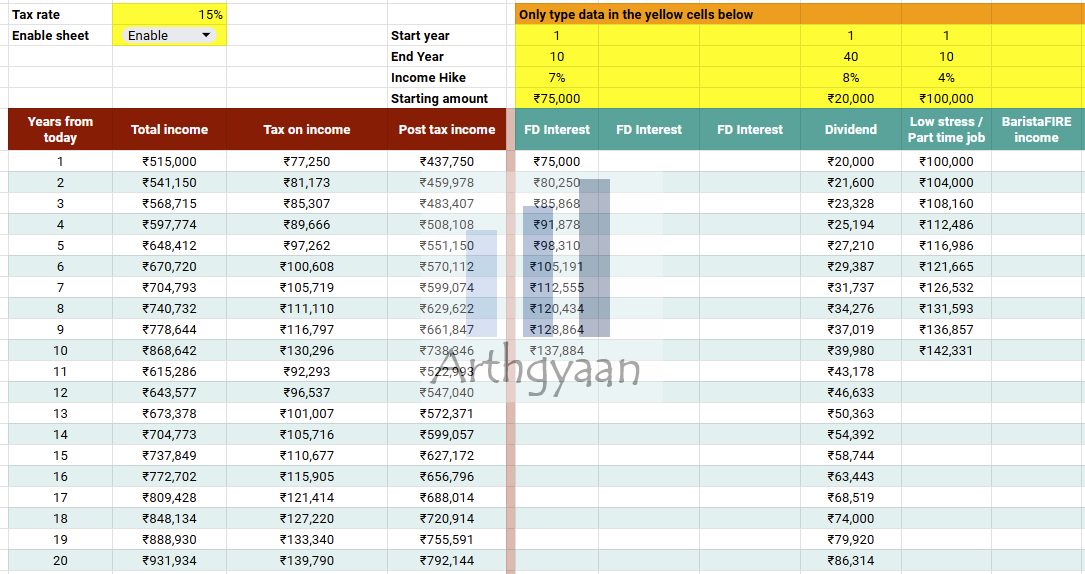

How to use the tool to enter multiple income sources?

The sheet allows you to enter each income stream in columns. For each, you need to enter four numbers:

Start year: This is the year from which this income starts. If the start year = 1, the income starts a year from now and so forth

End Year: This is the year when this income ends

Income Hike: This is the annual increase in income.

Starting amount: This is the income expected in the first year

To add more income streams beyond the 20+ examples already in the sheet, you need to add more columns between and fill in the formulas from left to right.

Note: It does not matter what the income stream is called since each income stream is entered in the same way with the same set of four numbers as described above.

How to access the tool to enter multiple income sources?

By default, the sheet is disabled which means that the income numbers are not enabled. You need to set the “Enable sheet” toggle to “Enable” to enable the numbers. A few income numbers have been entered for your convenience. To remove the sample values, you can set the “Starting amount” values to zero.

We will use Google sheets to create a simple calculator for this calculation. There is a link to download a pre-filled copy of the Google sheet via the button below.

Important: You must be logged into your Google Account on a laptop/desktop (and not on a phone) to access the sheet.

Here are some case studies using the tool (click the image below)

What to do once you enter your multiple income sources?

Multiple income sources will help you

require a smaller retirement corpus once you retire

take up a low-stress job when you become financially independent so that you can have money for personal interests and optional goals (Barista FIRE cases)

To see these income sources in action, please review these worked-out case studies.

Ready-made goal-linked mutual fund packages related to this article

If you are planning your FIRE journey, then Arthgyaan packages can help you create and manage your FIRE portfolio effortlessly. Choose the year closest to your desired FIRE year to get started:

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled How can you add multiple income streams to your portfolio for retirement? first appeared on 30 Oct 2024 at https://arthgyaan.com