This article analyzes the historical impact of rate cuts on bond markets and mutual funds and explores why a similar rate cut by the RBI could provide higher returns for investors.

This article analyzes the historical impact of rate cuts on bond markets and mutual funds and explores why a similar rate cut by the RBI could provide higher returns for investors.

What is the significance of the US Fed Rate cut by 50 bps?

The federal funds rate is the target interest rate set by the Fed at which commercial banks borrow and lend their extra reserves to one another overnight. - Investopedia

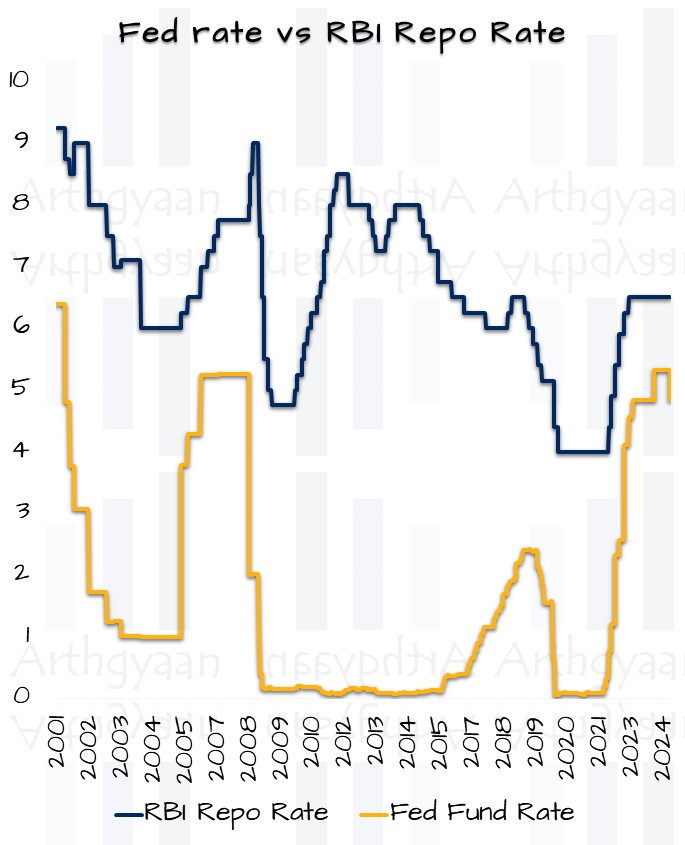

On 18 September 2024, the US Federal Open Market Committee (FOMC) cut the Fed fund rate by 0.5% or 50 basis points to 4.75-5.00%, their first rate cut since March 2020.

As a result,

it will be cheaper to borrow money and invest in new businesses or purchase houses, cars, etc

stimulate the economy since it is now cheaper to borrow and spend

the RBI is now incentivised to lower the repo rate in India as well

Lowering interest rates by the central bank, like the Fed and the RBI, affects both the stock and bond markets. In this article, we will understand if there are any opportunities, based on historical data, to get higher returns in long-duration debt mutual funds after a rate cut like this.

Why does a rate cut lead to higher returns in long-duration debt funds?

The one-sentence answer to this question is called interest rate risk. Bonds with higher interest rates, issued when the fed rate/repo rate was higher become more desirable when the central bank (here the Fed or the RBI) cuts rates and new bonds with lower interest rates are issued. This is why gilt funds, typically long-duration funds with no risk of default, fluctuate a lot in the opposite direction of interest rate movements.

This fluctuation with interest rates, typically in the short term due to a rate cut (in September 2024) or a rate hike (after March 2020) represents a trading opportunity.

Did you know that we have a private Facebook group which you can join for free and ask your own questions? Please click the button below to join.

Start Building Wealth with Expertly Curated Mutual Fund Packages

Does a Fed rate cut lead to higher short-term returns in long-duration debt funds?

We have taken mutual fund NAV data from the AMFI website for the “Long Duration debt fund” category since January 2013.

As per SEBI, Long Duration Debt Mutual funds are classified as

Investment in Debt & Money Market Instruments with Macaulay duration of the portfolio greater than 7 years

We expect that these funds, which hold long-maturity bonds (either government or corporate) will move up due to rate cuts and similarly fall due to rate hikes. We see the one-year average return of the category vs. any changes in the Fed rate or Repo Rate.

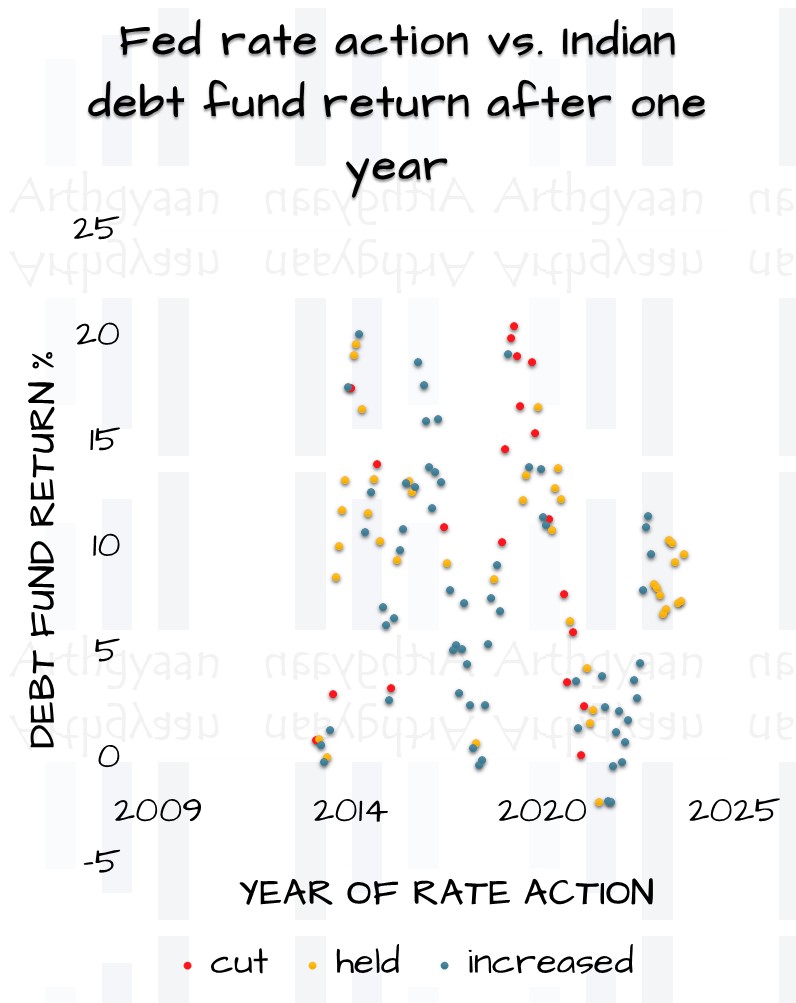

The chart of the one-year forward return of Indian long-duration debt funds vs. the Fed fund rate is shown below:

Unfortunately, there is no clear impact of a Fed rate cut (or rise) on Indian domestic long-duration bonds. We examine the same now vs. the RBI repo rate.

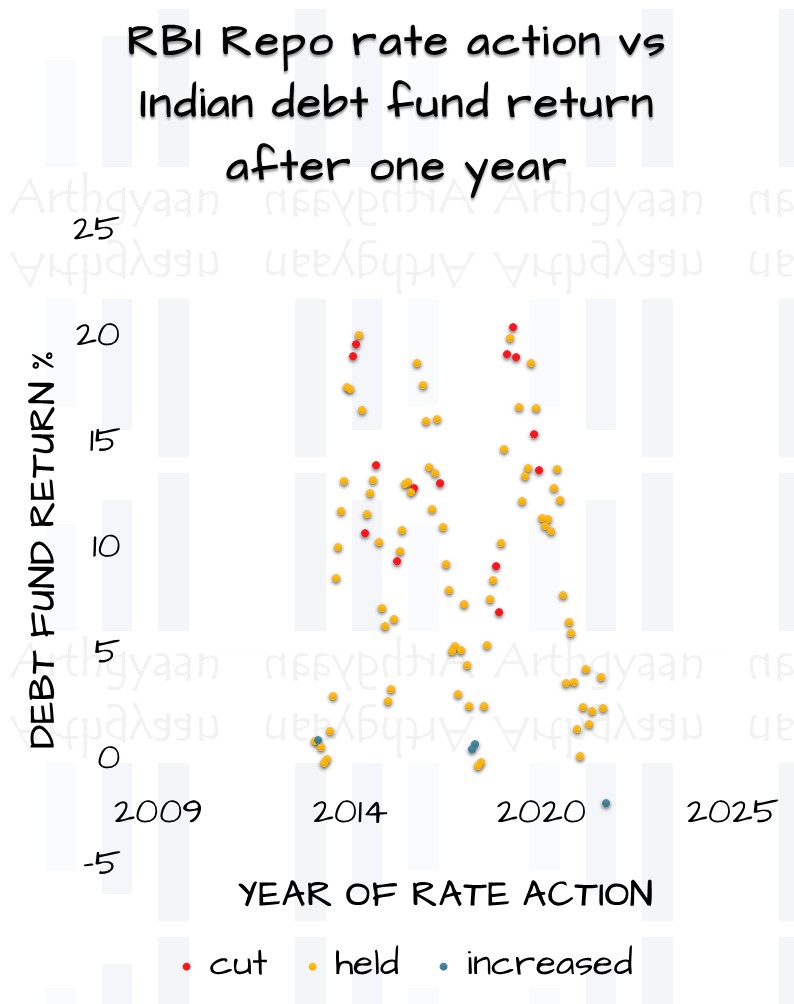

Here the result is clearer:

There is a marked uptick in one-year long-duration fund returns after a repo rate cut

Similarly, for a repo rate rise, there have been severely poor returns as expected

Therefore, unlike the Fed Rate cut, the RBI repo rate cut is a stronger indicator of long-duration fund returns in the short term.

What should investors do after the fed rate cut in anticipation of an RBI repo rate cut?

For the time being, no RBI rate has been announced. However, given how global markets are increasingly moving in tandem, a repo rate cut in December 2024 of 25bps or 0.25% is expected as per a Reuters poll.

Remember that if you are reading this news now, the bond market has already adjusted to the anticipated RBI rate cut. There is no window of opportunity right now. This is normal in both stock and bond markets and has a name for it:

Buy the rumour, sell the news

Instead, a better plan will be to understand how your current financial plan is allocated to safe (cash), low-risk (debt) and high-risk (equity) buckets for goals due in 0-5, 5-10, 10-15 years etc.

We need a method to divide your entire portfolio into these 12 categories (3 buckets: equity/debt/cash and 4 time-based groups) and allocate the correct amount of mutual funds to each.

We will use Google sheets to create a simple calculator for this calculation. There is a link to download a pre-filled copy of the Google sheet via the button below.

Important: You must be logged into your Google Account on a laptop/desktop (and not on a phone) to access the sheet.

Here are some case studies using the tool (click the image below)

This table is in the “goals” tab on the right.

Once you have the allocation planned for your portfolio based on where you are in the existing portfolio, vs. where you need to be in terms of both future goals and macroeconomic changes like the RBI repo rate cut, you can take steps accordingly to rebalance the portfolio. Do not take tactical steps based on news of rate cuts without understanding how that changes the risk-reward profile of your portfolio.

What's next? You can join the Arthgyaan WhatsApp community

You can stay updated on our latest content and learn about our webinars.

Our community is fully private so that no one, other than the admin, can see your name or number. Also, we will not spam you.

Disclaimer: Content on this site is for educational purpose only and is not financial advice. Nothing on this site should be construed as an offer or recommendation to buy/sell any financial product or service. Please consult a registered investment advisor before making any investments.

This post titled Does the 2024 Fed Rate Cut Signal Entering Long-Duration Debt Funds for Higher Returns? first appeared on 29 Sep 2024 at https://arthgyaan.com